![[Wonkish] A tale about the Great Nigerian Bond Market Bull Run of 2017 by @Walesmit](https://nairametrics.com/wp-content/uploads/2017/12/Black-Bull.png)

- The Bond Market Bull Run of 2017: Drivers and Outlook

- Note: This article is Wonkish

In a dramatic turn of events, interest rates across all segments of Nigeria’s fixed income markets collapsed last week following the announcement by the Debt Management Office (DMO) that it would repay N198 billion in maturing Nigerian Treasury Bill (NTB) obligations.

In the aftermath of the DMO notice, short-dated interest rates plummeted by 365 basis points to 11.8-17.7% while longer dated bond yields crashed to between 13-14% from 14-15%. The steep decline in rates reflected increased demand by banks and asset managers for securities to park the sudden influx of liquidity at time of diminished securities supply.

The build-up in system Naira liquidity pushed overnight borrowing and Open-Buy Back rates to 3-4% at the end of the week from elevated double-digit levels they averaged over the most part of 2017.

As stated earlier, the trigger for the sudden yield compression was the DMO announcement which effectively implied that in a departure from the fortnightly norm, there would be no NTB auction for the rest of 2017. To further complicate matters, the Central Bank of Nigeria (CBN), which had ceased daily issuance of its Open Market Operation (OMO) bills at the end of November 2017, also released a Q1 2018 NTB calendar which showed that the government borrowings would be market neutral.

The most telling evidence of the seismic shift in the fixed income market was a drop in average marginal rates at the monthly bond auction to 13.2% from 14.8% in November and the 15-16% trend for the most part of 2017. Interestingly, despite a sell-off over the first half of 2017, the yield declines implied that the S&P Nigeria bond market index is up 26% YTD.

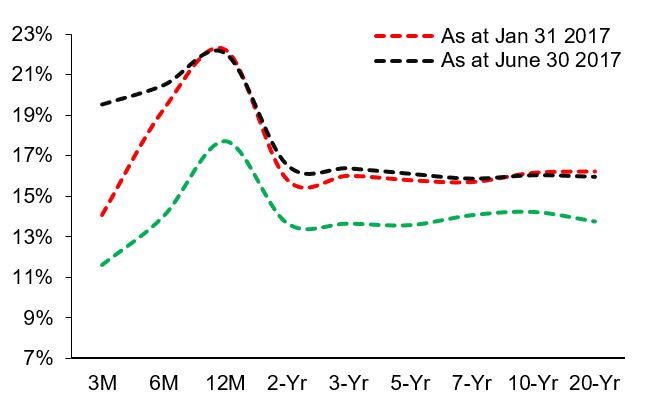

Figure 1: Naira Yield Curve

Source: FMDQ-OTC

The not so Monetary Policy

For a significant part of 2017, indeed since July 2016, interest rates have raced upwards to record levels, in line with the CBN’s hike in the key policy rate to a record 14%. To keen observers of Nigeria’s fixed income markets, the MPR is merely a meaningless totem with little predictive power in understanding where CBN wants interest rates along the yield curve.

This is not a trivial point. For example, while CBN hiked MPR to 14%, which implied that it would lend money to banks at 16%, given the 200bps spread charged on its standing lending facility to banks, it then went about issuing OMO bills at effective yields of between 18-22%. This scenario created an obvious arbitrage on the MPR, as a clever bank could in theory borrow from the CBN at 16% and wait to lend that money back to the CBN at its OMO auctions at 18-22% completely risk free.

Given the short term duration of OMO bills, with maximum 1-year tenor, debt market participants interpreted their yields as where the CBN wanted interest rates. To ensure everyone was on the same page, the apex bank commenced Naira liquidity sequestration via daily OMO issuance and when the market was unwilling to play ball, the CBN simply took the money with forced debits of bank balances under an arcane tool called stabilisation securities.

Crude Tactic

While one could theoretically explain the ramp-up in monetary policy tightening in the second half of 2016 as a bid to fight off roaring inflation, what was the justification for the sustained liquidity extraction in 2017 when headline inflation decelerated? The answer is not too far-fetched and indeed reveals the real policy anchor of the CBN: the exchange rate. Of course, thanks to the collapse in oil prices which drove a deterioration in Nigeria’s external balance into a deficit picture, CBN’s ability to ensure adequate supply across all segments of the FX market had waned.

Having weakened the Naira from N155/$ to N305/$ and unwilling to stomach any further depreciation, the CBN latched onto a crude tactic: curb Naira liquidity and USD demand will disappear. The adoption of this view resulted in a dramatic rise in outstanding CBN bills to over N8 trillion at some point. While government borrowings rose, on a net basis with over N600 billion in maturities, these were small in comparison. The CBN sucked up so much liquidity that money supply aggregates actually contracted on an annualised basis over the most part of 2017 in a developing country.

A natural consequence of the lop-sided paper supply by the CBN relative to the FG was that the yield curve inverted with short term interest rates being more elevated than longer dated yields. A naïve conclusion would be that the CBN wanted to offer real returns for investors at the short end of the yield curve. In economic theory, monetary policy should seek to influence short term interest rates as long term interest rates are a function of inflationary expectations over the medium to long term and the implication of that trajectory on future short term interest rates.

Market frenzy

The subsequent rise in yields favoured increased investments in fixed income instruments of a short-term duration with SEC data showing 139% jump in net asset value (NAV) of fixed income funds by registered asset managers to N301billion (89% of which went into money market funds). Despite having an implied liability of long-term structure, pension funds also jumped on the short-term yield chase with PFA holdings of NTBs jumping to N1.4trillion from (N779billion at the end of 2016).

This is understated, when one considers that holdings of local money market securities (bank placements and commercial papers) rose from N395billion to N545billion. In all, Nigerian pension funds, with a long-term focus, were holding over a quarter of their assets in short-term securities. For context, the FGN intends to spend roughly N2trillion on capital expenditure in 2017 which is just about the amount parked in treasury bills. Keen observers would have noted that banking stocks have rallied close to 80% on average relative to 49% YTD rally in the broader NSE reflecting an improved earnings outlook. The high yield environment favoured even banks who have reported 62% rise in profits over 2017 driven by strong interest income largely buoyed by income from treasury bills.

Policy U-Turn

So what changed in December that caused the CBN to end the high interest rate bonanza? Here, look no further than the improvement in oil prices and stability in oil production which pushed the external account back into surplus starting in Q4 2016. The steady improvement in FX reserves allowed the CBN, who had abandoned its brief flirtation with a floating exchange rate with re-imposition of a ‘peg’ in September 2016, to become more open to allowing some flexible trading in the market. Enter the Investors & Exporters (I&E) window in April 2017, which is a brain-child of CBN’s associate company, the FMDQ-OTC.

Given improved perceptions of Nigeria’s current account, the CBN rightly bet that limited flexibility would be rewarded by increased FPI inflows to Nigeria. To allow proper formation of expectations, the apex bank moved to wipe out the parallel market premium by re-connecting the BDC operators to its USD supply pipeline. Perhaps, unsurprisingly, the Naira appreciated from over 500/$ to the 360/$ spot rate of CBN interventions to private/retail demand.

Curious observers may have noticed that while the oil prices have strengthened, the Naira is yet to appreciate further than the N360/$ which is reflective of the new peg. Thus, there is little doubt that were the CBN to lower the rate of these interventions, the parallel market rate would appreciate to that level which would swing the interbank and I&E rate even lower. There is an implicit advice to the CBN in that point.

But the key takeaway is that the CBN now has the firepower to underwrite the Naira exchange rate in all segments of the FX market and with its subsisting current account curbs on the notorious 41 items, it retains control over troublesome import demands. Added to this is the FG’s newfound love for USD borrowings with the recent issuance helping to push reserves to over $38.2billion (Okay throw in a few FX swap inflows). Under these settings the CBN can afford to take its feet off the pedal and allow the market set rates. Cue the un-parallel downward shift in the yield curve at the end of last week.

So what will happen going forward?

Fundamentally, interest rates should reflect market expectations of inflation over the next one year. The CBN governor has painted a benign inflation outlook where it falls to single digits by the end of June 2018 even as he has dropped hints in media chats and conference speeches about a return to 12% MPR. Forward guidance appears to point to a monetary policy normalisation which would likely result in the entire yield curve at 11-13% levels. However, the CBN also faces a mounting liquidity challenge with over N6.7trillion in maturing OMO bills in 2018.

Left unchallenged, alongside an improved outlook for FAAC inflows given the improved oil revenue outlook, short-dated interest rates could collapse deep into single digits dragging bond yields along with it. Thus, it is highly unlikely that the CBN would allow things go untested without a return to OMO issuance though at a lower frequency than the daily pattern observed in 2017. That said, given likely pressures on CBN profitability, in the absence of any Naira devaluation, OMO issuance is likely to remain restrained. Some have argued that CBN is likely to raise CRR next year to grapple with the impending liquidity challenge to interest rates.

However, with CBN’s adoption of an asymmetric approach to CRR computation, which has resulted in effective CRR for banks being closer to 40% than the statutory 22.5%, one is unsure as to the likely success of that approach. In any case, it would be inconsistent with the body language of easing. A more likely approach would be to raise the rate on the Standing Deposit Facility to 10%, by returning to a symmetric corridor around the MPR, and importantly removing the N7.5billion cap for remuneration on daily outstanding balances.

This would allow the CBN to absorb cash from maturing OMO bills at a lower rate and importantly, this will set a floor on short-term interest rates. This was the original role of the SDF before the removal of the floor and reinstating its effectiveness would help normalise monetary policy.

Unlikely headwinds?

No doubt the improvement in the external account will translate to a more stable exchange rate which will help anchor inflationary expectations over 2018. With no planned adjustments in electricity tariffs until July 2019, the only plausible threat to inflation is from an adjustment to PMS prices from N145/litre by 10-20% given the recent rise in crude oil prices.

Politically, this would be a difficult pill given the proximity to the February 2019 general elections. Delaying adjustments to key prices is not new in Nigeria, the previous Jonathan government postponed electricity tariff adjustments for shaky reasons and only adjusted fuel prices lower even though it could not afford the implied subsidy bill. In all, the era of elevated naira interest rates is ending and another is starting. In the coming days, bond traders who have booked profits will predictably look to talk-up that Nigeria is not ready for low rates and that lower yields do not mean higher bank landing.

Similarly, local and foreign bond investors (i.e. those who adopt a yield perspective) will moan about negative real returns. These points will be moot in the absence of fresh inflationary pressures, lack of OMO issuance and restrained fiscal borrowings. Nigeria’s debt markets are merely for a demand and supply function if you really understand the market. Effectively their cries will be that the Nigerian government should borrow more and that the CBN should come out and mop-up more liquidity even though money supply has contracted.

If paper suppliers (read CBN and FG) limit securities issuance, those on the demand side, faced with limited investment outlets need to take what the going rate is. Most are unused to low fixed income returns and as a result will stay short duration and depress short term interest rates which will drive a flattening first then gradual normalisation of the yield curve over the next six months.

Figure 1: NTB Yields and Standing Deposit Facility

Source: CBN

{kind=link}