Follow Us on Google Discover

Follow Us on Google Discover

Cardinal Stone: Late Thursday (oct 26th), Morgan Stanley Capital International (MSCI) announced that Nigeria stocks will remain part of its frontier index and are no longer under review for a possible demotion to a standalone status. The decision was hinged on improved FX liquidity in the Nigeria market, likely related to improved FX transactions at the “Investors and Exporters” (IE) window.

For context, MSCI had previously announced in June 2016 that it was considering Nigeria for a possible downgrade to stand-alone status, highlighting deteriorating FX liquidity as well as FX restrictions as key concerns. This development led to a massive outflow of capital from the Nigeria equities market – Market capitalization declined by 17.14%. Until now, the decision whether or not to retain Nigeria in its Frontier Market Index has been a recurring theme in the Nigerian equity market space among both local and foreign institutional investors.

The Central Bank of Nigeria (CBN) in April, 2017 established the IE window that allowed for FX transactions at market determined rates in a bid to ease the concerns of foreign investors. Consequently, the MSCI decision on whether to retain Nigeria in its Frontier market indexes in June, 2017, was postponed to ascertain the effectiveness of the IE window. Unequivocally, the MSCI’s decision to retain Nigeria in the Frontier index reflects the success and effectiveness of the IE window.

Possible Impact of Decision

Also Read

Sequel to the implementation of the window, foreign sentiments improved significantly towards Nigerian equities. Despite the uptick in foreign interest, a handful of foreign fund managers waited on the side-lines in anticipation of the final MSCI announcement. We believe this potential demand from these foreign investors as well as tactical local market participants will spur positive sentiments in the short term.

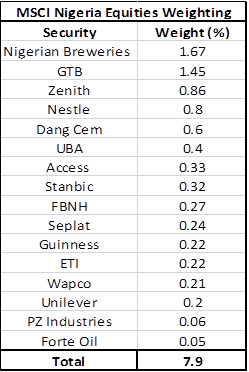

With the reassurance that investors can complete their transactions at a market determined exchange rate, we expect to see further influx of capital into the equities market. Currently, foreign portfolio managers tracking the MSCI Frontier Market index allocates weights varying from 3.98% to 4.99% compared to the 7.96% benchmark weight of the MSCI frontier index.

This implies that these fund managers are still significantly underweight. Thus, we expect underweighted fund managers to rebalance their portfolios in favour of the Nigeria market. This will consequently improve sentiments and demand for Nigerian equities.