Hotel development activity in Africa is still rising in the face of the continent’s economic problems, showing a 13 per cent increase in 2017, according to the annual survey by W Hospitality Group, generally acknowledged as the most authoritative source on the sector’s growth.

The ninth edition of its Hotel Chain Development Pipelines in Africa has 36 international and regional contributors reporting almost 73,000 rooms in 417 hotels. The figures have grown each year, more than doubling since 2009.

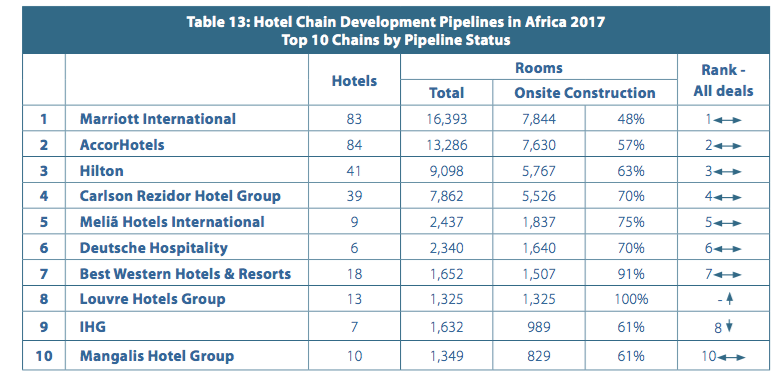

This year, bragging rights are shared; Marriott International, boosted by its merger with Starwood, comes top of the table in terms of number of rooms planned. But AccorHotels continues to lead – just – by the number of hotels in its pipeline. By country, Egypt is in first place with the highest number of hotel rooms in the on-site construction phase.

The report, along with all the challenges of developing new hotels in Africa will be discussed by industry leaders and government officials at the seventh Africa Hotel Investment Forum (AHIF) in Kigali, in October. AHIF is the highest-level gathering of hotel investors and developers in Africa.

Many African countries faced a challenging 2016, with lower prices for oil and other commodities, devalued currencies and other negative factors. That may have affected confidence in the short-term, as the number of deals signed was 86, down from 121 in 2015.

Despite the slowdown, some countries benefited from cheaper oil imports and there was increased activity in southern and east Africa. In addition, more hotel chains established development offices on the continent, to address the fact that Africa is still massively under-provided with rooms.

Growth is expected to be more muted in 2017, and financing and bureaucratic hurdles remain, but an increasing number of deals are coming to fruition on time: from only 26 per cent opening their doors on schedule in 2014, to 47 per cent in 2016.

SOME KEY FINDINGS:

The results show that investor confidence is returning to North Africa after several years of turmoil and uncertainty in countries such as Egypt and Tunisia.

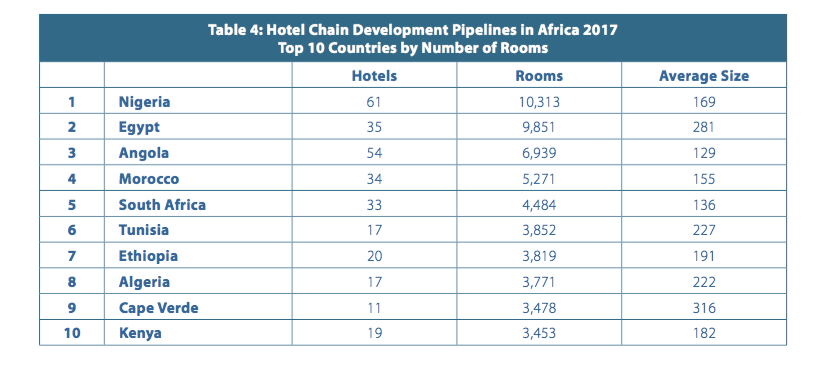

The top ten contains four of the five North African countries, with several deals signed in 2016, including 12 in Egypt.

The top ten contains four of the five North African countries, with several deals signed in 2016, including 12 in Egypt.

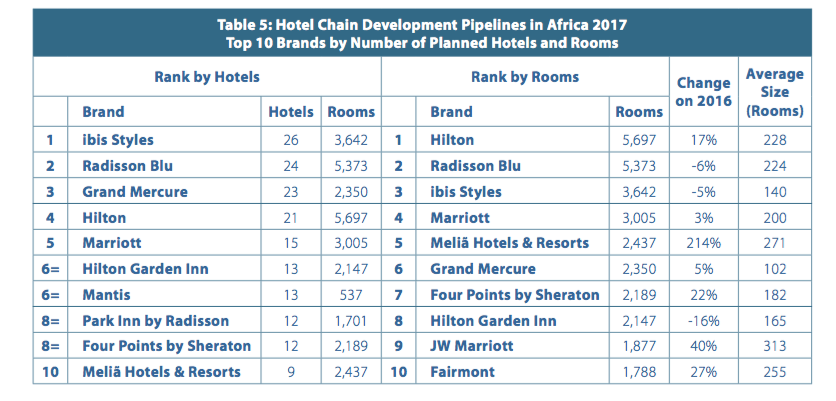

In the ranking by number of hotels, AccorHotels has two brands in the top five positions – Ibis Styles and Grand Mercure, both pipelines primarily in Angola.

When ranked by the number of rooms, the Hilton brand displaces Radisson Blu from last year’s top slot.

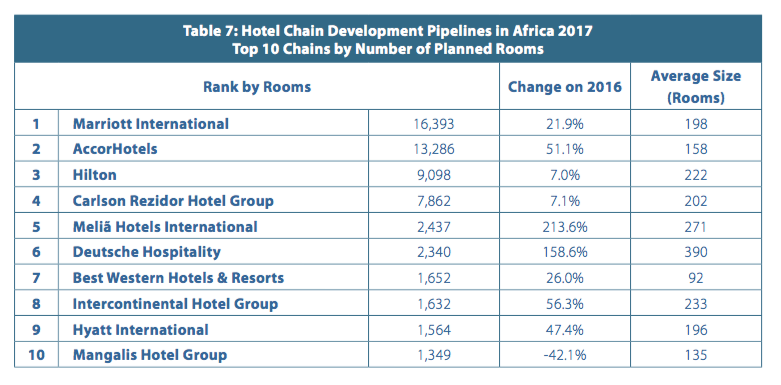

AccorHotels continues to lead the ranking of the chains – as opposed to individual brands – by number of planned hotels, 84 vs 83.

But Marriott International leads in terms of rooms, 16,393 vs 13,286.

But Marriott International leads in terms of rooms, 16,393 vs 13,286.

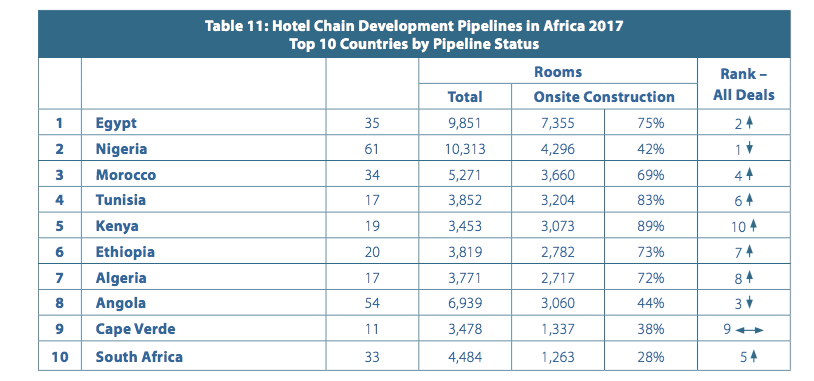

Nigeria has the most hotels and rooms in the development pipeline, but Egypt has the most rooms actually under construction, almost 75% of the total.

Marriott, AccorHotels, Hilton and Carlson Rezidor Group retain their position as the top four hotel chains by pipeline status.

Based on the hotel deals signed by the chains at the time of the survey, their anticipated opening years are shown in the table below. A hundred new hotels are expected to open their doors this year and 117 next year, although expectations are often over-optimistic, as noted above!

W Hospitality Group managing director, Trevor Ward, said: “Several countries in Africa have suffered severe economic problems in the past couple of years.

“But there are encouraging signs that we are turning a corner in 2017, and whilst growth is more muted, there is definitely an acceptance of the “new normal”, with a desire to move forward again in a climate of lower-valued currencies, less government spending and lower GDP growth.

“The world in 2017 is a very different place to when we started this survey in 2009. But Africa is still rising, at least as far as the development activities of the hotel chains is concerned. Whilst the chains do not, generally, build or invest in the hotels they brand, at the other side of every deal there is an investor eager to do so.”

Matthew Weihs, managing director of Bench Events, concluded: “With many more rooms in the pipeline and a much higher proportion being built on time, one has to recognise that hotel development in Africa is becoming an increasingly serious business.”

Ends

About W Hospitality Group

The W Hospitality Group, a member of Hotel Partners Africa, specialises in the provision of advisory services to the hotel, tourism and leisure industries, providing a full range of services to clients who have investments in the sector, or who are looking to enter them through development, acquisition or other means. In sub-Saharan Africa the W Hospitality Group is regarded as the market leader due to the market and financial expertise of its staff, its worldwide knowledge, and its commitment to its clients. In Africa, W Hospitality Group has to date worked in 39 countries on the continent, from its Lagos and Addis Ababa offices.

About the Africa Hotel Investment Forum (AHIF)

AHIF is the premier hotel investment conference in Africa, attracting many prominent international hotel owners, investors, financiers, management companies and their advisers. It is organised by Bench Events (www.benchevents.com), which is known for producing, alongside Questex Travel + Hospitality and MEED Events, several other top-level hotel conferences around the world including Berlin (IHIF), Dubai (AHIC), Istanbul (CATHIC) and Moscow (RHIC).

Sponsors of AHIF Rwanda are: Host Sponsors: Rwanda Development Board; Platinum Sponsors: AccorHotels, Hilton Worldwide, Marriott International and The Rezidor Hotel Group; Gold Sponsors: Best Western; Colliers International, Grant Thornton; Horwath HTL, Hotel Partners Africa, JLL, Kempinski, Minor Hotels, Mövenpick; STR, Swiss Education Group and Wyndham Worldwide

About Bench Events

Global event organiser Bench Events has a long track record of delivering multiple premium hotel investment conferences and forums across Europe, the Middle East, Africa, Asia and Latin America.

Market leading annual conferences include the Arabian Hotel Investment Conference (AHIC) in Dubai, now in its 13th year, the Africa Hotel Investment Forum (AHIF) the new Asia Hotel and Tourism Investment Conference (AHTIC), The Summit in London and the Latin American Hotel & Tourism Investment Conferences (SAHIC).

Bench Events’ extensive portfolio also includes the Global Restaurant Investment Forum (GRIF) in Dubai and AviaDev, designed to promote the future air connectivity in Africa.

Bench Events’ mission is enabling prosperity by facilitating growth, networking, and thought leadership in the hospitality industry worldwide.

www.benchevents.com

Further Information

For further information and high resolution images, please visit https://www.africa-conference.com or contact:

- Sophie Luis, Tarsh Consulting, Email: Luis@Tarsh.com Tel: +44 (0) 20 7112 8556, Cel: +44 (0) 7961 145 787.

- David Tarsh, Tarsh Consulting, Email: David@Tarsh.com, Tel: +44 (0) 20 7602 5262, Cel: +44 (0) 7770 816 070.

{kind=link}