Ecobank Transnational Incorporated Plc. (3 months ended March 2015)

- Ecobank Transnational Incorporated Bank Plc (ETI) released Q1 2015 unaudited results wherein gross earnings rose 23% YoY to N134.6 billion, while PBT and PAT rose 58% and 65% YoY to N30.5 billion and N24.7 billion respectively. Nonetheless, on the heels of USD appreciation against ETI’s main currencies[1], underlying growth, in dollar terms, was more modest across all three items: Gross earnings (+4% YoY), PBT (+33% YoY) and PAT (+38% YoY).

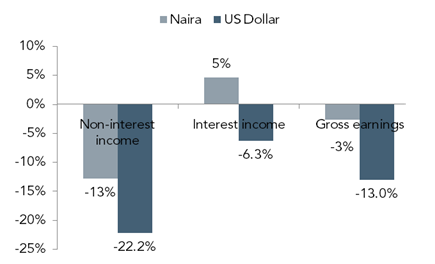

Pull back in NIR weighs on gross earnings

- Relative to prior quarter, gross earnings are weaker (-3% QoQ) as non-interest revenue retreated from Q4 14 highs (-13% QoQ to N50.5 billion) which offset 5% QoQ expansion in interest income to N84.1 billion. Adducing drivers, amid flat movement in naira interest earnings assets to N4.01trillion vs. a 9% cut back on dollar terms, we see currency translation as the underpin for the discrepancy between dollar and naira interest income movements. On NIR, which contracted in both naira and dollar terms, we believe the implementation of the order based two way quote system in Nigeria which reduced USDNGN volatility tempered FX trading gains. (Nigeria accounted for ~42% of NIR in FY 14).

- Figure 1: QoQ trends

Source: ETI financials, ARM Research

Tight lid on cost and provisioning offsets funding pressures

- Interest expense tracked faster than interest income, rising 7% QoQ to N29.8 billion, but maintained the same dynamic as the latter shrinking 4% in dollar terms. Parsing through funding base items, pressures stemmed from higher interbank takings (+27% QoQ) and borrowings (+17% QoQ) as deposits shrank (-4% QoQ). Thus, annualized WACF rose 30bps higher than Q4 14.

- Conversely, after jumping in Q4 14 (+15% QoQ) when ETI consolidated IT costs, opex growth resumed its prior subdued trend, shrinking 5% QoQ to N65.7 billion ($: -15% QoQ) leaving CIR flat at 63% from Q4 14.

- Impairments recorded a similar step down from Q4 14 (+127% QoQ) when heightening macro risks drove ETI to adopt a cautious stance towards loans to public sector entities and oil and gas in Nigeria. In the current quarter, impairments declined 59% QoQ to N8.6 billion) resulting in annualized cost of risk contracting to 1.3% (FY 14: 1.9%).

- Overall, the benign movements in opex and impairments neutered feed-through from weak top-line trends resulting in PBT and PAT jumping 48% and 77% QoQ. Correspondingly, both PBT and PAT are 8pps higher QoQ (5pps YoY) at 23% and 18% respectively.

Headwinds to SSA economies and Nigeria’s capital raise lie ahead

- Over the rest of 2015, the more tempered growth outlook for Sub-Saharan Africa which has seen the IMF lower regional GDP growth by 40bps to 4.5% in April and weak currency picture drives more cautious loan growth outlook for ETI. The subdued risk asset creation theme is more central in ETI’s Nigerian subsidiary which underpinned growth in loans in 2014, first on the more modest growth picture in Nigeria (IMF forecast: 4.8% vs. 2014 actual GDP growth of 6.2%) and secondly as Ecobank Nigeria’s CAR at the end of 2014 stood exactly at the 16% threshold for SIBs. ETI’s management guides to conclusion of a capital raising process in Q3 15 via a dilution of group’s 100% interest in Ecobank Nigeria.

- Whilst ETI’s geographical platform positions the bank to experience NIR expansion on FX volatility across its various African subsidiaries, we think NIR growth should become subdued on account of changes to the FX trading landscape in Nigeria which induced shrinkage in naira volatility.

- On asset quality, the weak economic landscape facing certain public sector entities and downstream oil and gas in Nigeria speaks to some deterioration in asset quality over 2015 which should drive higher cost of risk and net weakness in earnings.

- Overall, we see scope for moderation to our last published FVE (N24.5) which, given recent upward price movement (+28% in last three months) and premium on multiples (ETI trades at a current P/E of 5.9x and P/B of 0.95x relative to peers at 5x and 0.9x respectively), should translate to downgrade in our OVERWEIGHT rating.

- Source: ARM

Disclosure – This article was culled from ARM Research newsletter and was not solely written for Nairametrics. The author of this article wrote it themselves, and did not write this article on behalf of Nairametrics.

{kind=link}