Nairametrics| Zenith Bank and GT Bank are two of the most profitable banks in Nigerian history. They were both the first to cross the N100 billion mark in after tax profits and have dominated the banking landscape over the last decade. However, one bank has consistently outperformed the other where it matters most. And that bank is GTB.

GTB vs Zenith

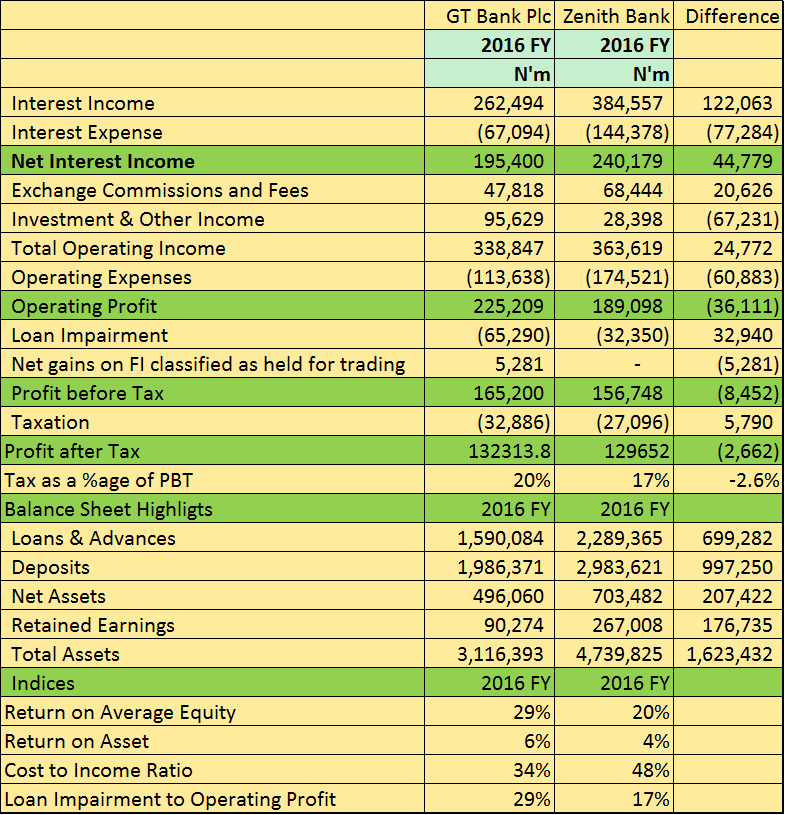

Zenith Bank on paper appears to be larger than GTB in terms of total assets, customer deposits, and even loans advanced. For example, in 2016, Zenith’s customer deposits of N2.9 trillion is more than GTB’s N1.9 trillion deposit. Zenith also had net assets of N703.4 billion compared to GTB’s N496 billion. Despite this, GTB continues to out perform Zenith where it matter. Here is why;

Net Interest Income

Here Zenith Bank raked in about N240 billion, N44 billion higher than what GTB made in 2016. However, GTB got N74 for every N100 of interest earned, while Zenith got N62 for every N100.

Other income

Zenith Bank also raked in more cash from commission and fees compared to Zenith Bank. However, GTB more than made up for it with gains from forex revaluation.

Operating Expenses

This is where GTB is stronger than most banks. Even though Zenith Bank had a higher operating income than GTB, the latter made up for it with a much lower operating expense. Zenith Bank spent N48 for every N100 of operating income, compared to GTB’s N34. We do observe that GTB spent incurred a higher impairment on its loans.

Return on Average Equity

As mentioned, Zenith has a net asset of about N703.4 billion. However, what it does with it is what really matters. In terms of return on equity it only posted 20% compared to GTB’s 29%. GTB outperformed again in 2015 at 26% to Zenith’s 18.4%. The same things was observed in 2014 with GTB’s posting a return of 27.9% compared t0 Zenith’s 18.8%

Super GTB

GTB’s business model is one that has been very difficult for a lot of Nigerian banks to replicate. The bank operates a low cost, revenue efficient model that relies less on manpower but more on prudent risk asset allocation while attracting cheap deposits. For most banks, it will take years to replicate and possible billions spent in restructuring to achieve this. GTB has consistently reported a cost to income ratio of about 45% and even beat that record this year to post a CIR of about 34%. Zenith reported a CIR of under 50%, for the first time since we started tracking.

For a shareholder, the two most important reward for investing in a company are growth in the company’s share price/valuation as well as consistent dividend payments. This demonstrates why despite Zenith Bank’s dominance in balance sheet size, it has consistently trailed GTB in terms of market valuation. Despite the relatively larger size Zenith has, it continues to post lower earnings per share ratio when compared to GTB. In terms of dividends, it also trails GTB in dividend per share. To attract a higher valuation than GTB, Zenith Bank shareholders will have to hope that it post a significantly higher earning per share.

It’s probably going to take something drastic to have Zenith Bank outperform GTB in terms of profitability and share price. For now, we do not see that happening, at least in the near term.

{kind=link}

Kindly look at Zenith Bank dividend per share compare to Gtb and revert appropriately.

It’s because GTB has one of the largest underpaid contract staff amongst the tier one banks in NIgeria. It’s not as if they are doing anything superficial in keeping operating costs low.

Very consistent in banking policy

One of the reasons you will say gtbank mase more profit is they stylishly sacked workers (asking them to forcefully resign and also converting car loan into normal customer loans at a very higher interest, gtb they just asked some people to resign this may 2017)

In short, buy shares in both of them and sit tight. NLT