Bond Yields Spike to 8-Month High as RM offshores cut down on NIGB Holdings amidst EM Rout

Bear market grips Lagos stocks on politics, emerging-market woes – Bloomberg

KEY INDICATORS

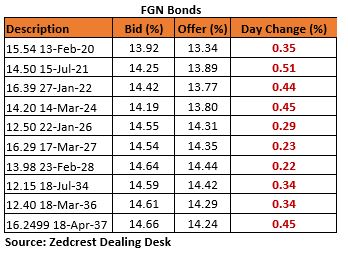

Bonds

The Bond market traded on a significantly bearish note in today’s session as real money offshore clients cut down on their FGN Bond holdings amidst a global emerging market rout exacerbated by the recent Turkish crisis. Yields have consequently hit an 8-Month high of c.14.40%, with significant selloffs witnessed especially on the 2024 -2036 tenors. The 2027s and 2036s were the most hit, having last traded at 14.55% and 14.60% respectively.

We expect this trend to persist and advice that clients remain short duration in the near term.

Treasury Bills

The T-bills market remained relatively flat, with most activities focused on the shorter end of the curve, which trended higher by c.30bps on average.

In the coming week, we expect yields to track slightly higher due to expected OMO and FX Interventions (wholesale & retail) by the CBN to offset inflows from Maturing OMO bills (c.N440bn on Thursday) and to support liquidity in the FX market.

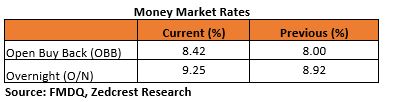

Money Market

The OBB and OVN rates inched slightly higher to close the week at 8.42% and 9.52% respectively, following a slight dip in system liquidity to c.N250bn positive.

We expect rates to trend slightly higher opening next week, due to anticipated funding for a wholesale FX auction by the CBN on Monday.

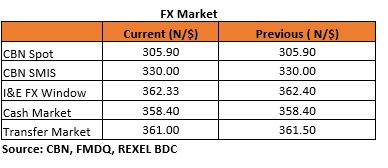

FX Market

The Naira remained stable at N306.00/$ at the interbank market. It however appreciated by 0.05% at the I&E FX window, closing at N362.00/$ (from N362.19/$ previously). At the parallel market, the cash rates appreciated by 20K to N359.50/$, while the transfer rates fell back by N1.00 to N362.00/$

Oil prices strengthened slightly today, with Brent crude futures rising by c.76cents to $72.76pb, after plunging earlier in the week on the back of escalating trade tensions and increase in US inventories. The CBN’s External reserves has however maintained a steady decline, falling by c.0.13% to $46.70bn as at 10-Aug, from $46.76bn on the 9th of August.

Eurobonds

The NGERIA Sovereigns remained significantly bearish in today’s session following the rout in emerging market assets. We witnessed the most selloff on the 2047s which lost about 2.50% on the day.

Activities in the NGERIA Corps were also mostly bearish, with the most selloff witnessed on the GRTBNL 18s, ACCESS 21s Snr and SEPLLN 23s. We however witnessed continued interests on the FIDBAN 22s, which gained about 0.50% on the day.

{kind=link}