OMO Auction tapers excess liquidity, bonds rally on demand

Nigerian Central Bank auctions N315.33bn in OMO bills to manage excess system liquidity

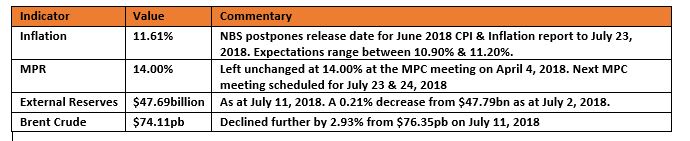

NBS postpones release of June Inflation figures

KEY INDICATORS

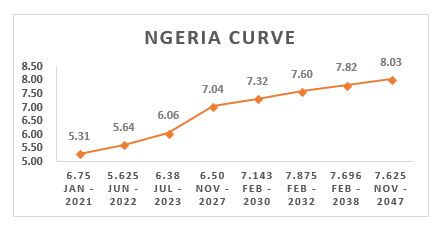

Bonds

The Bond market witnessed demand for locally-issued bonds, as market participants continued interests on the 2027s (mid-term) and 2036s (long-end) securities. Yields compressed by c.11bps on the average across board.

The Nigerian Bureau of Statistics has announced the delay of the release of the June 2018 Inflation report till later in the month (July 23, 2018), however the expectations for a lower figure remain unperturbed and will continue to support demand pressures in the interim. We retain a caution outlook on local bonds in the interim , until all possible factors come to play in providing a clear direction in yields.

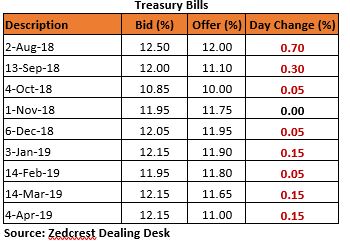

Treasury Bills

As expected, yields in the T-bills market reacted to the Central Bank of Nigeria’s OMO auction stop rates, which closed at 11.05% and 12.15% for the 70D- and 210-Day maturities. Market participants repriced traded maturities across board, which saw discount rates expand by c.0.18bps on the average.

T-bills will continue this adjustment to close the week, with market participants trading cautiously following expectations of possible further OMO auctions to further take out the remaining liquidity.

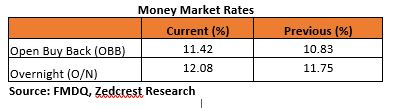

Money Market

The interbank market opened awash with liquidity (at N619.12bn), boosted by OMO maturities of N406.83bn, spurring the Central Bank of Nigeria to take via an OMO auction. On offer were the 70- and 210-Day bills, were a total of N315.33bn was sold at 11.05% & 12.15% stop rates respectively.

OBB and O/N rates dropped to open at 4% and 5% respectively, but moved upwards following the OMO auction to trade at 9% (OBB) and 10.00% (O/N) in late trades as market still remains relatively liquid.

FX Market

The Naira depreciated at the I&E FX Window, with the NAFEX rate losing 0.11% to close at N 362.25 from N361.87/$ previously. The Interbank rate however remained relatively flat, closing at N305.80/$.

In the parallel market, cash rates lost the gains from the previous day to close at N358.80/$, 0.03% lower than N358.70/$, while the transfer market however saw the Naira gain 0.14% to close at N362.50/$.

Eurobonds:

NGERIA Sovereigns continued to rally, as investors continue their interest for short-term traded tickets causing yield to drop by c.04bps on the average. The long-term traded tickers however lost c.02bps on the average.

The NGERIA Corps saw more investor interests, with yields compressing further by c.10bps across board. The toast of investors for the day were the FIDBAN 22s and SEPLLN 23s, where yields dropped by c.17bps and c.98bps respectively.

{kind=link}