Dangote Cement Plc 2013 9 Months ↑

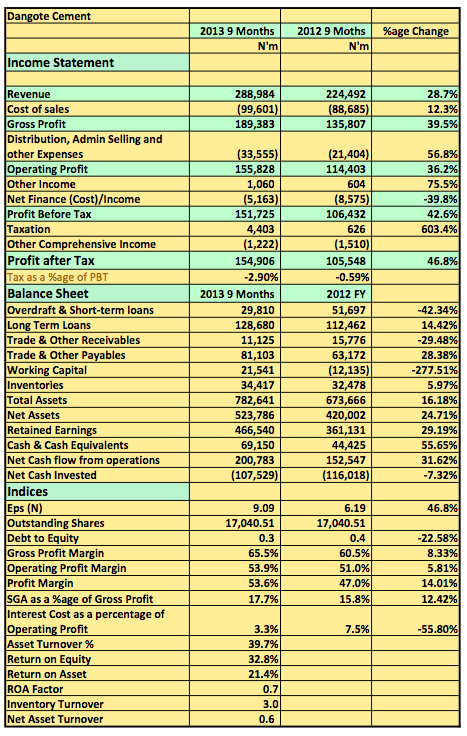

Dangote Plc released its 2013 9 Months results showing a 29% YoY rise in revenues to N289billion (2012 9months: N224billion). Gross profit also rose 40% to N190billion as the company kept up its amazing Gross profit margins. Pre-tax profits at the end of the period was N151.7billion a 42% rise over the same period last year. [upme_private]

2013 Q1-Q3

Key Highlights

- Dangote Cement is not new to double digit growth in revenue, however its Gross profit margin of 65% YTD is unmatched in the industry. One wonders how this is achievable. It is either their cement is more expensive or their management is exceptionally efficient and keeping cost down

- For example a margin of 65% indicates a mark up on cost of about 190%. That is for every N1 of cement produced the company sells at N190!!!

- The other reason seems more plausible; the company may just be very efficient they need not reduce price of cement unless off course competition requires it. In other words, their ability to maintain a high margin means they can control their pricing more effectively,

- In terms of profitability last year’s result was blown off by this year’s. However, it is a different story when you compare the results QoQ this current year.

- Profitability dipped by 18% this quarter compared to Q2. This was mostly attributable to a 12% drop in revenue this quarter compared to Q2. The company blamed drop in Gas utilisation this quarter at their Obajana factory in Nigeria’s Kogi state. It fell to 67 percent in the third quarter.

- Is it a cause for concern? Probably not after all 2012 Q3 pre-tax profits also came in lower than 2012 Q2 by 13%. However, the fact that pre-tax profits hardly grew QoQ this year may well be an indication that 2014 may just be a tough year for the company even though plans are underway to source additional gas and fuel supplies “in the coming years”.

- Interest expense is still under 4% per quarter, however opex seems to be averaging N11billion per quarter this year compared to N7billion in 2012.

- I guess sooner rather than later, their growth rate will have some form of correction amidst rising operating cost, competition and a market hungry for cheaper building materials.

- Dangote Cement strength is in its size market dominance. There is also room for growth as it is primed to go far beyond the Nigerian market if it growth becomes scarce. However, the effects of the massive investments on depreciation cost, amortization, finance cost will continue to posse a challenge on profits.

- Dangote Cement is in our portfolio and we hope to increase our purchase in the coming weeks. At N190 the price is N7 cheaper than how much we purchased it. That price is 21x trailing EPS and 7.8x book value per share. Share price as risen 61% in the last 1 year.

Dangote Cement released its 2013 9 Months results in the website of the NSE[/upme_private]

{kind=link}