Follow Us on Google Discover

Follow Us on Google Discover

FCMB, First Bank, and Fidelity Bank led the list of best-performing commercial banks in the third quarter of 2022. This is according to an analysis of the financial and equity performances of publicly quoted banks, carried out by Nairalytics, the research arm of Nairametrics.

The research pours into the performance of thirteen of Nigeria’s largest commercial banks analyzing improvement year on year over two quarters.

The analysis revealed that the thirteen banks raked in a sum of N298.84 billion as post-tax profit between July and September 2022, representing an increase of 29.9% compared to N228.54 billion recorded in the corresponding period of 2021.

The commercial banks remained resilient despite economic headwinds, which saw the nation’s aggregate GDP growth slowed to 2.25% in Q3 2022 from 3.54% recorded in the previous quarter and 4.03% in the corresponding period of 2021.

Also Read

Also, banks’ loans to customers grew by 5.5% between June and September 2022 to stand at N23.76 trillion, representing a net new loan of N1.23 trillion in three months. However, this showed a slightly slower growth than the 6.81% increase recorded in the comparable period of 2021.

Banking Sector data by NBS

Meanwhile, despite improved financial performance in the third quarter of the year, data from the National Bureau of Statistics (NBS) shows slow growth compared to previous periods.

- According to the NBS, the Nigerian banking sector (sector GDP) slowed from 20.06% and 25.5% growth recorded in Q2 2022 and Q3 2021 respectively to 12.03% in real terms in the period under review.

- This is the slowest quarterly growth rate since Q1 2021 when the economy was still recovering from the impact of the covid-19 pandemic.

- However, the Nigerian banking sector is a vital sector of the Nigerian economy, which sets the tone for many other sectors, vested with the responsibility of ensuring credit moves from sectors with excess capital/cash to others with a deficit in a bid to spur aggregate real economic growth.

How Nigerian banks performed Q3 2022

Customer deposits increased by 5% in the period under review to stand at N43.68 trillion as of September 2022 from N41.61 trillion as of June 2022.

- Only four out of the thirteen banks recorded a positive growth in the share price in Q3 2022 at the local equities market.

- The thirteen banks recorded an average cost-to-income ratio of 64.96% in the review period, compared to 69.11% recorded in the corresponding period of 2021, indicating more income as opposed to expenses.

- The banks printed an average return on average equity (ROAE) of 15.25% (annualised) in Q3 2022, in contrast to the 13.4% recorded in the previous year.

Best Performing banks in Q3 of 2022

Nairametrics presents a ranking of the best commercial banks in the third quarter of 2022, using metrics from their publicly released financial statements and performance at the local exchange.

- The key metrics considered in these analyses are total asset growth, loan book growth, profit growth, cost–to–income ratio, customer deposit growth, return on average equity and share price appreciation.

- Because we also know, each metric carries a different measure of impact, especially for investors, we assign weights to each category.

- Thus, our analysis applies a weight of 5% for asset growth, 15% for profit growth, 15% for loan book growth, 15% for customer deposit growth, 20% for change in return on average equity, 10% for changes in cost-to-income ratio, and 20% for share price appreciation, respectively.

Note: Ecobank was not included in this analysis due to most of its operations being outside the shores of Nigeria. You can read previous editions for H1 2022 and Q1 2022.

A. Leading banks by total asset growth: The thirteen banks under consideration grew their total assets by 4% from N63.59 trillion recorded as of June 2022 to N66.13 trillion as of the end of September 2022, representing an increase of N2.54 trillion in three months.

Access, Zenith, and First Bank recorded the highest asset value as of the period under review, however, the position changed in terms of growth rate. Below are the leading banks by total assets growth between June and September 2022.

- First position – Zenith Bank (+12.1%)

- Second position – FCMB (+10.6%)

- Third position – Union Bank (+4.8%)

- Fourth position – Jaiz Bank (+3.8%)

- Fifth position – UBA (+3.6%)

B. Leading banks by customer deposits growth: Customer deposits to the thirteen banks increased by 5% in the third quarter of 2022 to stand at N43.68 trillion from N41.61 trillion recorded as of June 2022.

Access, Zenith, and UBA recorded the highest customer deposits as of September 2022. Meanwhile, below are the leading banks by growth in customer deposits in Q3 2022.

- First position – Zenith Bank (+12.4%)

- Second position – FCMB (+11%)

- Third position – Jaiz Bank (+6.9%)

- Fourth position – Union Bank (+5.3%)

- Fifth position – First Bank (+4.7%)

C. Leading Banks by loan book growth: A bank loan is an important metric used in assessing the performance of banks. Notably, loans allow for growth in the overall money supply in an economy and open up competition by lending to new businesses. The interest and fees from the loans also form a major part of banks’ earnings.

The loan books of the twelve banks (Jaiz Bank excluded) that reported their customer loans grew by 5.5% to stand at N23.76 trillion as of September 2022 from N22.53 trillion recorded as of June 2022.

As of the period under review, Access Bank boasts the largest loan book at N4.62 trillion, followed by Zenith Bank and First Bank with N3.88 trillion and N3.6 trillion respectively.

Meanwhile, in terms of loan book growth, below are the top banks for Q3 2022;

- First position – Zenith Bank (+10.9%)

- Second position – Union Bank (+10.8%)

- Third position – UBA (+10.8%)

- Fourth position – Stanbic IBTC Bank (+6.7%)

- Fifth position – First Bank (+6.5%)

D. Leading banks by profit after tax (PAT) growth: A bank’s profit after tax is an important measure of how they are able to generate enough returns to share as dividends while also retaining for future business expansion.

The thirteen banks posted a profit after tax of N296.84 billion in Q3 2022, an increase of 29.9% from N228.54 billion recorded in the corresponding period of 2021.

In terms of profit after tax, Zenith, GTCo, and Access Bank led the list of banks with the highest profit, meanwhile, below is the ranking in terms of profit growth.

- First position – First Bank (+1k%)

- Second position – Fidelity Bank (+61.7%)

- Third position – Sterling Bank (+42.7%)

- Fourth position – Stanbic IBTC (+40.8%)

- Fifth position – Access Bank (+37.1%)

E. Leading banks by the cost-to-income ratio: The cost-to-income ratio is a key financial metric, which shows a company’s costs as a proportion of its income. It helps to give investors a clear view of how efficiently a bank is being run. Specifically, it shows how much input the bank requires to generate N1 of output.

Notably, the lower this ratio, the more profitable, productive, and competitive the bank will be. Here are the banks with the highest decline in their cost-to-income ratio:

- First position – First Bank (-31.6%)

- Second position – FCMB (-16.3%)

- Third position – Stanbic IBTC (-5%)

- Fourth position – Zenith Bank (-4.9%)

- Fifth position – Access Bank (-3.2%)

F. Leading banks by return on average equity (ROAE): The return on equity is also an important metric that shows the percentage of profit made on every N1 of the shareholders’ fund. It is used to measure the performance and efficiency of the banks.

This metric will show how well banks have maximized any increase in shareholders’ wealth. Below are the top banks with the highest increase in their ROAE year-on-year.

- First position – First Bank (+14.19%)

- Second position – Fidelity Bank (+4.75%)

- Third position – FCMB (+3.81%)

- Fourth position – Sterling Bank (+3.72%)

- Fifth position – Zenith Bank (+0.54%)

G. Top banks by share appreciation: Investors take positions in companies especially banks in exchange for capital appreciation and dividends. Whilst, they do not have control of dividend, they have control over when to sell their shares and pocked capital appreciation. This makes the metrics very important to us at Nairametrics.

The Nigerian equities market dipped by 5.4% in the third quarter of 2022, losing N1.48 trillion in market capitalization, while the listed banks suffered significant sell pressure. Meanwhile, the banking sector index also closed the quarter down 4.67%.

Out of the thirteen banks listed on the Nigerian Exchange, only four of them recorded share price appreciation in the review period.

- First position – Wema Bank (+8.2%)

- Second position – Fidelity Bank (+7.6%)

- Third position – Sterling Bank (+2.0%)

- Fourth position – Union Bank (+0.8%)

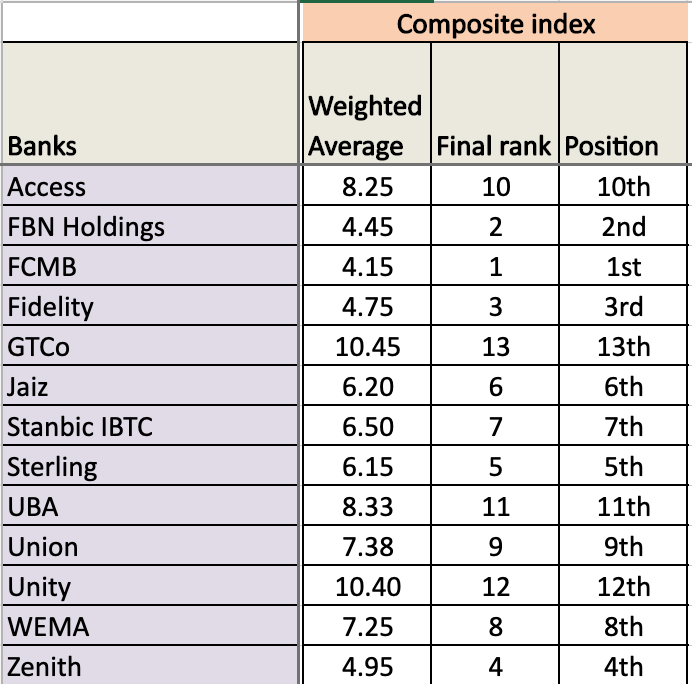

Final Scorecard: The final ranking allocates equal weights to each of the metrics considered in this analysis, with the bank with the highest weighted rating selected as the best-performing bank for the quarter.

- Based on our analysis FCMB is the best-performing bank in Q3 2022.

- The bank scored a weighted average score of 4.15 points, having ranked second in three categories, third in one, and fourth in one category.

- The bank did not rank first in any category but did just enough across the categories to come out tops.

- First Bank and Fidelity Bank followed with 4.45 points and 4.75 points respectively.

Snapshot of our ranking

A. How they perform per category of measure

B. Ranking of each bank based on their respective performances across sectors

C. Final score based on a weighted average of the performance of each bank for each category.

How do we determine the best performers?

We focus on seven key metrics, Asset growth, PAT growth, Loan growth, Deposit growth, ROAE, Cost to income, and share price growth.

- The percentage change between the third quarter of 2022 and the corresponding period of 2021 is considered.

- Positive growth in the context of any metrics counts as a positive in our ranking while a decline is negative. An example of context setting is profits and cost. For example, a rise in profits year on year is positive growth while a decline in cost to income ratio is also positive growth.

- Banks are not ranked based on the achieved growth in any of the seven key metrics. For example, the bank with the highest positive growth in any metric ranks first.

- We then multiply the bank’s position in each category with the assigned positions for the category to determine the final weighted score.

This compilation is based on research conducted by Nairalytics Research. This article was also updated to provide more information on how we determine our score.

Contact info@nairametrics.com for more information or comments about this article.