Follow Us on Google Discover

Follow Us on Google Discover

Money Market

The average money market rate dropped by 6.36% to settle at 3.54% from 9.90% in the previous week due to the significant improvement in system liquidity during the week. The system liquidity is estimated to have closed the week at a cN692 billion.

Major inflow for the week included: OMO Maturity of cN735bn and Coupon Payment of cN42bn while major outflow included Weekly Wholesale, Invisible and SME FX auction of $210mn, and OMO sale of cN323bn The Open Buy Back (OBB) and Overnight rate (O/N) fell to 3.21% and 3.86% from 9.29% and 10.50% respectively in the previous week. Barring several OMO auctions this week, we expected the Money Market rate to remain low.

[READ ALSO:Why NNPC may sack depot managers]

Also Read

Forex: USD/NGN

The foreign exchange market remained relatively stable last week as the CBN Official Rate decline marginally by 3bps to close at N306.90/$ while the rate at I&E FX window fell by 0.23% to close at N362.93/$. The rate in the parallel market remained unchanged at N360.00/$. We expect rates in the parallel market to remain constant as the apex bank continues to supply FX into the market, coupled with its frequent Wholesale and Retail SMIS programme.

Bond: FGN

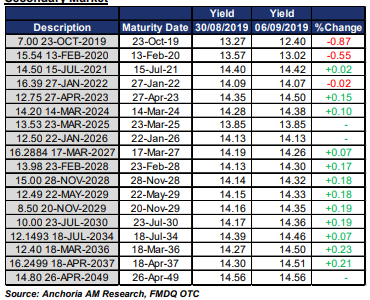

The secondary sovereign Bond Market closed in a slightly bearish note last week with the average yield up 2bps to closed at 14.15% from 14.13% in the previous week. The narrative was different for the sovereign and Corporate Eurobond market as the average Sovereign Eurobond yield fell by 31bps to close at 6.25% from 6.56% in the previous week, while the average yield on Corporate Eurobond fell by 32bps to 5.48% from 5.81%.

During the week, Zenith Bank announced its intention to exercise a call option on its outstanding 2022 Eurobond worth $500million on 16th September 2019. This week, we expect the Bond market to continue the renewed demand interest seen at the later part of the last week as Crude oil price moved above the budget benchmark.

Treasury Bills

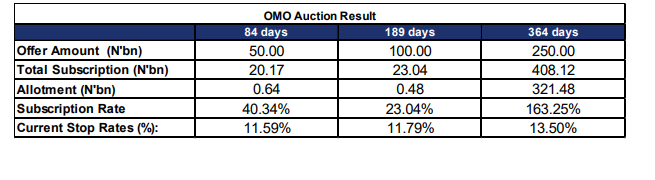

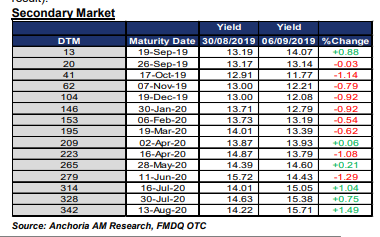

Due to buoyant system liquidity, the treasury bill (secondary market) closed on a bullish note. The average T-bills yield fell from 13.84% to 13.33% in the previous week. (see next page for Last week OMO result).

Commodities

Oil price strengthens last week on the backdrop of the news that the People’s Bank of China (PBoC) would introduce more bank reserve requirement (RRR) that will help stave off ongoing economic headwinds and possibility for reduction in crude oil production by OPEC.

[READ ALSO: Investors renew demand for FGN bonds ahead of expected maturity]