Follow Us on Google Discover

Follow Us on Google Discover

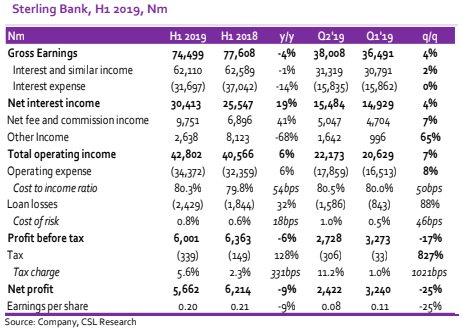

Sterling bank delivered a decent performance during H1 2019 as the efforts of the bank in attracting low-cost deposits and optimizing its deposit mix impacted Net Interest Margin (NIM) positively. Net Interest Income grew 19% y/y while NIM improved significantly to 7.5% in H1 2019 (H1 2018; 6.2%) on the back of lower funding cost (6.5% in H1 2019 vs 8.2% in H1 2018).

[READ ALSO: Bet9ja’s Headquarters raided by court officials]

We expect the bank’s continued investment in digital platforms and continued expansion of its business operations aimed at deepening its penetration in the retail segment of the market to keep Operating Expenses (OPEX) slightly elevated. We, however, expect the investments in its digital platforms to support growth in Non-Interest Income in the medium to long term. We have raised our FY 2019e PBT by 16% to N13.2bn (from N11.4bn previously, FY 2018; N9.5bn) and FY 2019e EPS to N0.43 (from N0.32 previously, FY 2018; N0.28). We also estimate ROAE of 11.5% in 2019e, compared to 9.2% delivered in 2018.

We have updated our model and the overall impact is a revision in our target price upwards to N2.84/s from N2.46/s previously. We are upgrading the stock from a HOLD to BUY considering the 21% upside implied by the latest closing price of N2.35/s amidst a fairly positive outlook. We arrive at our target price based on an implied 0.70x PBV multiple to our 2019 forecast BVPS of N4.06/s.

Also Read

[READ MORE: MAN raises concerns over AfCFTA]

CSL STOCKBROKERS LIMITED CSL Stockbrokers,

Member of the Nigerian Stock Exchange,

First City Plaza, 44 Marina,

PO Box 9117,

Lagos State,

NIGERIA.