Follow Us on Google Discover

Follow Us on Google Discover

Welcome to Nairametrics‘ summary of the daily performance of major economic indicators and highlights from trading sessions and key statistics such as Treasury Bills and Bonds. This is brought to you by Zedcrest.

This report is dated June 3rd, 2019

Key Indicators

Also Read

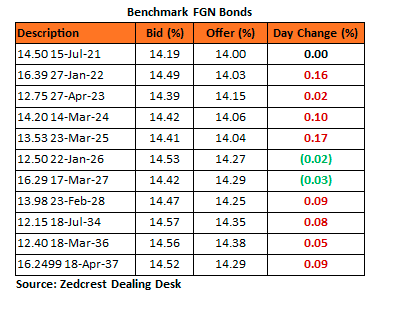

Bonds: The Bonds market opened the month at a slow pace, with little flows been passed during today’s trade session. As yields expanded across the bond curve by c.6bps on the average signalling weakened appetite for FGN Bonds.

We expect market players to trade cautiously in the coming week, as oil prices stabilise amid escalating global trade tensions spearheaded by the US.

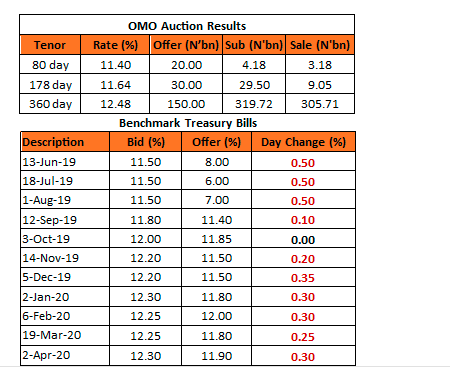

Treasury Bills: The T-Bills market also started the new month on a muted note mostly due to the announcement of an OMO auction by the CBN. Yields across the NTB curve expanded by c.30bps on the average, as the market adjusted to the anticipated supply from the CBN.

At the OMO auction, the CBN sold a total of N317.94bn across three maturities. The stop rates for the 80, 178- and 360-day tenors were 11.40%, 11.64%, and 12.48% respectively, marginally lower than the previous auction.

We expect yields to remain at these levels during the rest of the week, as there is an outside chance for another OMO auction to mop-up maturities expected later in the week.

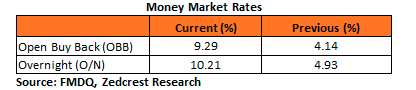

Money Market: Rates in the money market opened the week higher following an OMO auction by the CBN. The Apex bank mopped up c.N317.94bn of excess system liquidity through its OMO sale as system liquidity closed at c.N192bn positive. The OBB and OVN rates closed at 9.29% and 10.21% respectively.

We expect rates to stabilize later in the week, with c.N177bn expected in OMO maturities this week. The CBN is expected to stem the excess system liquidity using its Retail FX Bi-Weekly auctions.

FX Market: At the Interbank, the Naira/USD rate remained unchanged at N306.95/$ (spot) and N356.92/$ (SMIS). The NAFEX closing rate in the I&E window however increased marginally by 0.01% to N360.76/$, whilst the market turnover dropped by 13% DoD to 184.75m. At the parallel market, the cash and transfer rates strengthen to close at N358.80/$ and N362.50/$ respectively.

Eurobonds: The NGERIA Sovereigns resumed trading with continued bearish sentiments in the light of lower oil prices, with Brent’s recovery still lower than last week’s closing level. Yields consequently expanded by c.4bps on the average across the sovereign curve.

In NGERIA Corps, we witnessed continued interest on the shorter-dated tickers, with gains in ACCESS, FBNNL and ECOTRA 21s sustained for a second consecutive trading session. We witnessed better sellers for the ETINL 24s, +6bps higher on the day.

________________________________________________________________________

Contact us:

Dealing Desk: 01-6311667 Email: research@zedcrestcapital.com

Disclaimer: Whilst proper and reasonable care has been taken in the preparation and accuracy of the facts and figures presented in this report, no responsibility or liability is accepted by Zedcrest Capital or its employees for any error, omission or opinion expressed herein. This report is not an investment research or a research recommendation and should not be regarded as such. The information provided herein is by no means intended to provide a sufficient basis on which to make an investment decision.