Welcome to Nairametrics‘ summary of the daily performance of major economic indicators and highlights from trading sessions and key statistics such as Treasury Bills and Bonds. This is brought to you by Zedcrest.

This report is dated May 23rd, 2019.

***Oil gets clobbered as trade war fears mount***

Key Indicators

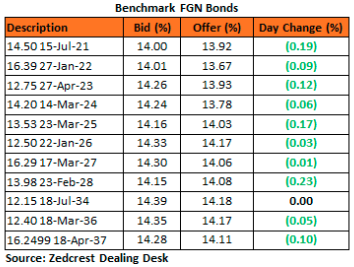

Bonds: The FGN Bond market traded on a bullish note, with yields lower by c.10bps on the day, following the significant downtrend in bond auction rates in the previous session.

We, however, expect yields to retrace slightly higher tomorrow following the renewed OMO intervention by the CBN, where effective yield cleared at 14.24% on the long tenor bill offered.

Treasury Bills: The T-bills market turned slightly bearish, with rates trending higher by c.20bps, following the OMO auction announcement by the CBN.

Whilst the CBN offered 150bn of the OMO bills, a total of N373bn subscriptions were received. The CBN consequently sold a total of c.N361bn, with stop rates clearing significantly above market expectations especially on the 357-day, which was cleared at 12.50% (+70bps above secondary market bid).

Given the renewed OMO sale by the CBN, we expect the market to remain bearish tomorrow, with funding pressures from the bi-weekly retail FX auction, expected to further pressure rates.

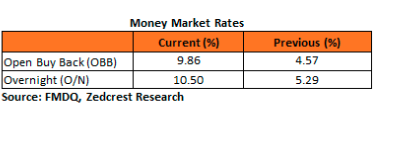

Money Market: Rates in the money market inched higher by c.5pct, due to outflows for the OMO auction sale by the CBN. The OBB and OVN rates consequently ended the session at 9.86% and 10.50%, with net system liquidity estimated at c.N90bn closing the day.

We expect rates to spike tomorrow, as banks fund for the bi-weekly retail FX auction by the CBN.

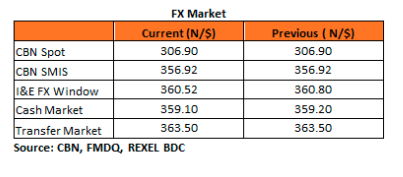

FX Market: At the Interbank, the Naira/USD rate was unchanged at N306.90/$ (spot), and N356.92/$ (SMIS). The NAFEX closing rate in the I&E window however decreased by 0.08% to N360.52/$, as market turnover rose by 370% to $342m, due to renewed FPI inflows for the CBN OMO auction. At the parallel market, the cash rates decreased by 0.02% to N359.10/$, while the transfer rate remained unchanged at N363.50/$.

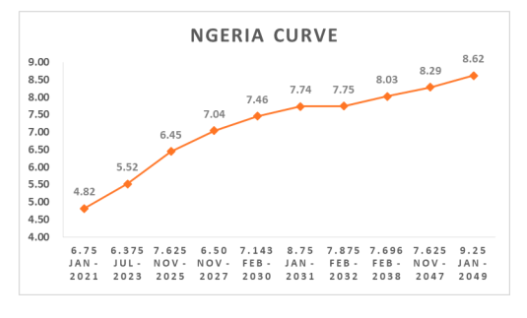

Eurobonds: The NGERIA Sovereigns were significantly weaker in today’s session as oil prices plunged on the back of further strains in the US-China trade negotiations. Yields were consequently higher by c.7bps on the day, with the most selloff witnessed on the long end of the curve.

We witnessed strong demand for the NGERIA Corps, with the most interests still on the FIDBAN 22s and ETINL 24s.

Contact us:

Dealing Desk: 01-6311667 Email: research@zedcrestcapital.com

Disclaimer: Whilst proper and reasonable care has been taken in the preparation and accuracy of the facts and figures presented in this report, no responsibility or liability is accepted by Zedcrest Capital or its employees for any error, omission or opinion expressed herein. This report is not an investment research or a research recommendation and should not be regarded as such. The information provided herein is by no means intended to provide a sufficient basis on which to make an investment decision.

{kind=link}