Daily performance of major economic indicators and highlights from tradings sessions and key statistics such as Treasury Bills, bonds, FX rates, inflation, oil price.

- DMO to offer N70bn FGN Bonds tomorrow as N100bn FGN Sukkuk Bond Offer Closes

- FG, World Bank PSRP Loan Negotiation Ongoing – Fashola

KEY INDICATORS

Bonds

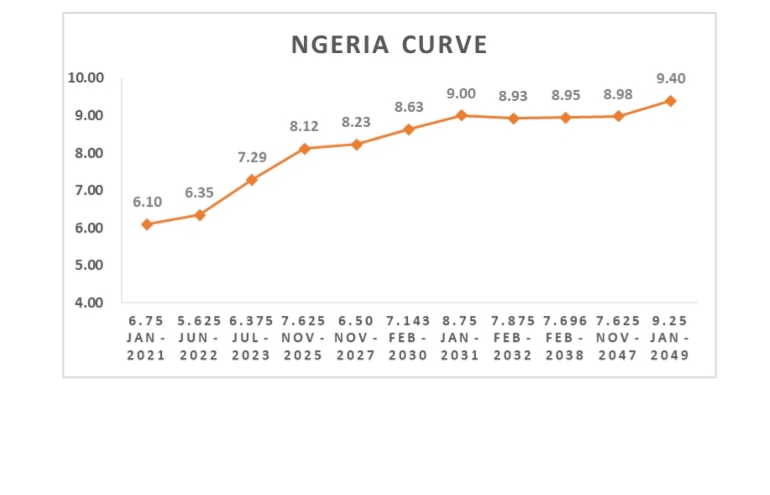

The FGN Bond market remained relatively flat, except for slight sell on the 2027 bond, which was the most actively traded on the day, with yields marginally higher by c.6bps on the ticker. On the average, yields were however unchanged on the day.

With the closure of the FGN Sukkuk bond offer today, the DMO will auction N20bn, N15bn and N35bn of the 2023, 2025 and 2028 FGN bonds tomorrow. We expect subscription levels at the auction to remain low given the recent lull in demand for bonds in recent sessions. Yields are consequently expected to clear marginally higher from their previous levels, whilst also noting that the DMO is not under significant funding pressure and would be willing to manage rates at the auction.

Treasury Bills

The T-bills market returned bearish in today’s session, as the CBN maintained its OMO interventions in the market with total sale of c.N25bn of the N150bn offered. Yields consequently trended higher by c.5bps, as selloffs on the short end of the curve, outpaced slight demand around some mid tenors.

We expect the market to remain slightly bearish as the CBN maintains pressure on system liquidity via its continued OMO auctions.

Money Market

Rates in the money market moderated by c.20pct, with the OBB and OVN rates closing at 19.33% and 21.95%, as system liquidity opened the day at c.N43bn positive, whilst market players were able to access the CBN’s SLF window to fund their obligations. With the OMO sale of c.N25bn today, system liquidity is estimated at c.N18bn positive as at COB today.

We expect rates to remain elevated tomorrow, with the CBN expected to conduct another round of OMO interventions due to the c.N472bn in OMO maturities expected on Thursday.

FX Market

At the Interbank, the Naira/USD rate remained unchanged at N306.95/$ (spot) and N359.24/$ (SMIS), while the NAFEX rate in the I&E window appreciated further by c.0.01% to N364.96/$ from N365.18/$ previously. Meanwhile, at the parallel market, the cash rate remained unchanged at N365.00/$ while the transfer rate fell by c.0.27% to N368.00/$.

Eurobonds

The NGERIA Sovereigns remained slightly bearish following slight sell mostly on the longer end of the curve (47s & 49s) which were higher by c.5bps on the day.

In the NGERIA Corps, yields on the DIAMBK 19s rallied c.120bps lower, whilst we witnessed renewed interests on the Access 21s, FBNNL 21s and Zenith 22s.

Disclaimer:

Whilst proper and reasonable care has been taken in the preparation and accuracy of the facts and figures presented in this report, no responsibility or liability is accepted by Zedcrest Capital or its employees for any error, omission or opinion expressed herein. This report is not an investment research or a research recommendation and should not be regarded as such. The information provided herein is by no means intended to provide a sufficient basis on which to make an investment decision.

{kind=link}