Follow Us on Google Discover

Follow Us on Google Discover

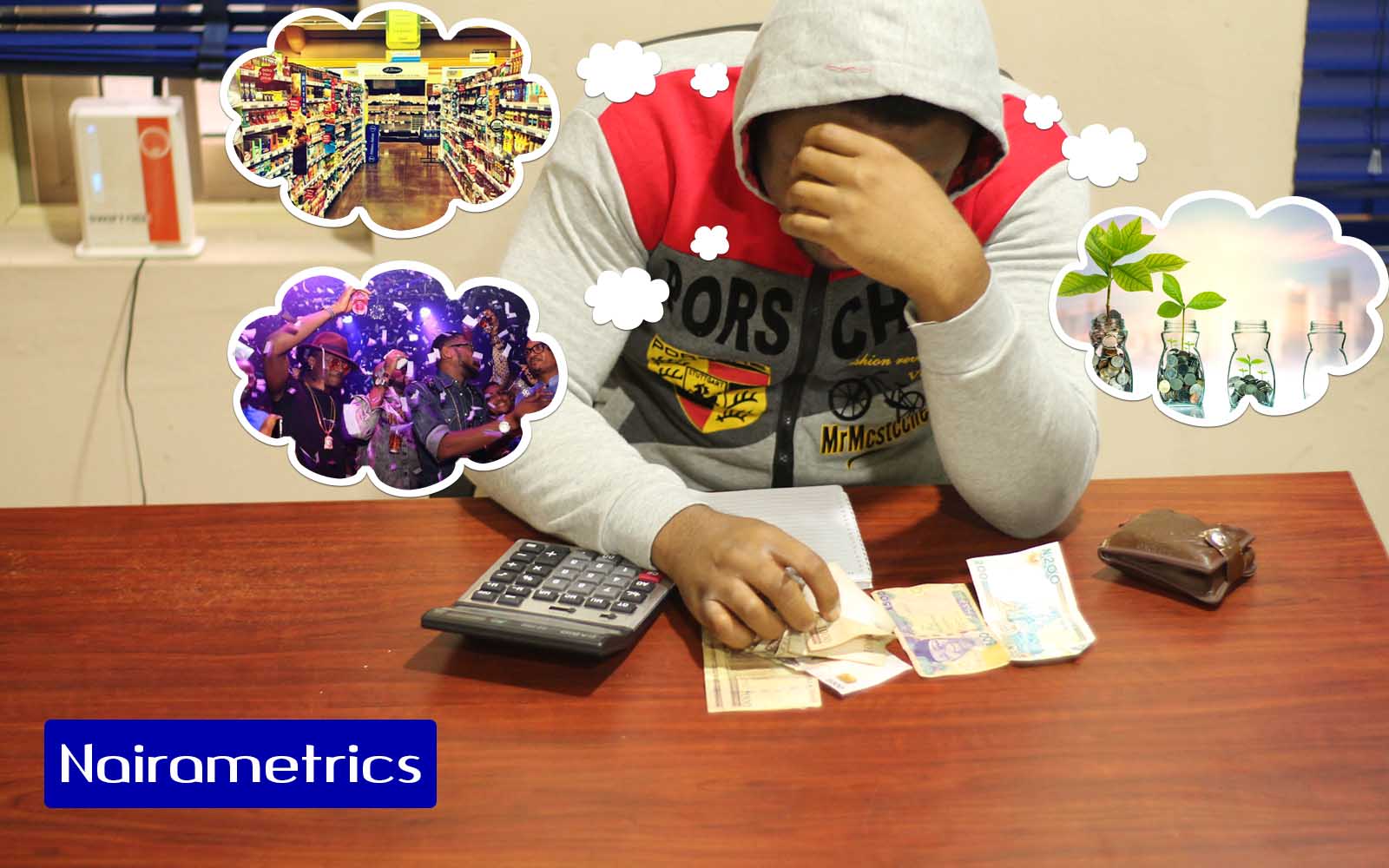

It’s that time of the month when salaries are paid, and 27-year old John could not seem to stop fiddling with his android phone as he awaited an important SMS from his bank. The young man, who works in one of the biggest advertising agencies in Lagos, was undecided. And as his phone finally buzzed with the notification of his salary payment, he pondered for the last time whether to stick to his investment plans or cheat once again like he did the month before.

Just a few months earlier, John had begun reading a lot about personal finance and investing. This, of course, changed his understanding of wealth creation. He learned that if he could form the habit of stashing away a portion of his monthly salary for the purpose of investment, he might become a relatively rich man by the time he is 40.

The narrow path to financial independence

John had learnt about some forms of investments he could make like treasury bills, the stock market and mutual funds. He chose treasury bills because he figured that they are safer and more reliable in terms of guaranteeing returns.

But it wasn’t long after the young man began investing in treasury bills that he became discouraged. This was because the amount of money he could afford to invest was not yielding him as much returns as he anticipated. And this is understandable because his money wasn’t enough to produce impactful profits. At a 12% interest rate per annum, the N50,000 he could afford to invest in TB monthly only yielded him N6,000 at the end of the year. This was not good enough for him.

Also Read

So, he decided to seek better investment options. As he later remarked while seating across the table from me in a restaurant, “And that was how I got into crypto.”

Ponzi schemes the “surest” forms of investments?

For a country like Nigeria that boasts of a population of 185 million people and a GDP of over $500 billion, portfolio investment is a quagmire for a lot of young people. Besides the lucky few like John, most young Nigerians are unemployed. Even a lot of those who are employed do not earn enough money to save, let alone invest.

Data obtained from the National Bureau of Statistics (NBS) shows that Nigeria’s youth unemployment rate is as high as 35%. As a result of this, most of these young adults often have to resort to freelancing in order to earn just enough to get by each day. For others with jobs, however, the situation is a bit better, though they can’t seem to find worthy investments.

According to Ugodre, Founder of Nairametrics, this is one of the major reasons why many young Nigerians fall prey to Ponzi schemes. He believes that unlike the regular forms of investments, the high returns associated with Ponzi schemes are understandably too enticing for them, regardless of the risks. In his words:

“If you invest N50,000 for a chance to earn N150,000 in two months, compared to N6k per annum, it’s not hard to understand the choices they make. This is especially so when they have seen their friends evidently earn this much.”

But some are sticking to regular forms of investment

28-year old Nonso told us how the economic crisis of 2015 created a unique investment opportunity for him. At the time, he had just turned down a job offer from one of Nigeria’s top commercial banks in order to pursue a master’s scholarship offered by the African Union. The scholarship guaranteed Nonso a monthly stipend of $750, money he ensured to save up throughout the 18-month period of the programme.

Having successfully saved up about $10,000, he profited by trading the currency in the black market. Recall that the Naira’s exchange rate against the dollar was high during this period. Moreover, many Nigerians were in constant need of hard currency. Nonso kept trading his dollars in the black market until he decided to try other forms of investment, precisely treasury bills.

Unlike John who could only afford to invest N50,000 per month, Nonso had more money for long-term fixed income investment. Consequently, he kept investing in treasury bills between 2016 and early 2018 when he finally left Nigeria.

“A lot of Nigerian youths are unemployed. Even most of the employed ones I know are investing their money on relocating. 50% of my former classmates at Access Bank have left Nigeria either for Australia, Germany, USA or the UK. More are still working on their applications to leave.” -Nonso

A common trend among our young interviewees

Much like Nonso, 23-year old Amby was awarded a scholarship during her first year as a medical student in one of Nigeria’s Federal Universities. The scholarship guaranteed her a substantial amount of money which would be paid yearly throughout the six-year period of her study. She told us that she made a decision to invest the money in a life insurance policy because “I needed to keep my money in a place where I won’t touch it and yet the interest would be higher than normal.”

TB is still relatively more attractive with less risk. Though rates are still tumbling down.

— Bayo™ 🦇 (@bayoadetunji) October 19, 2018

Similarly, Razaq who is 28 and works in one of the biggest NGOs in Nigeria, believes investment in treasury bills and equities are essentials. According to him, treasury bills are safe, and equities always present opportunities for growth.

Razaq, however, acknowledged the fact that equities can be risky sometimes. Some of the ways he averts losses are by diversifying his portfolio and also closely monitoring the stock market to know when to buy and sell.

“I buy when prices are low. I also buy more than one stock in order to diversify the risk. I monitor prices frequently to know when to exit.”

Meanwhile, for Mr Achara who works in the banking sector, his choice of investment is determined by what is yielding the most interest at any given time. For now, he said he is interested in treasury bills because of the increase in rates.

Others are simply investing in their small businesses

Recall that a recent analysis by Nairametrics revealed how young Nigerians are afraid to invest in the Nigerian stock market. While the findings of that report are quite alarming, having depicted Nigerian youths as a group who would rather squander their money than invest, the truth remains that there are millions of youths who make daily investment decisions. They may not all be investing in treasury bills or buying equities, simply because some of them are starting new businesses with their savings.

A typical example of such Nigerian youths is Femi, a 30-year old Nigerian male who has established one of the biggest plantain plantations in his locality. Femi told us that he has always been interested in farming right from early on in his life. And after investing in other farmers for a while, using the platform FarmCrowdy, he finally decided in 2017 to start his own farm and hopefully have others invest in it someday.

On a final note…

While it is arguable that many Nigerian youths do not currently make much efforts to invest, the truth is that quite a number of them are doing just that. These young investors are also embracing different dimensions to investment, including investment in smart farming, cryptocurrency and the traditional money market.

It is important to note that they make these investments because they understand that in order to have less financial stress in the future, they have to make the plans now and invest, no matter how small the investment.

Hopefully, having read through this article, you too will begin to think about what forms of investments can work for you. This is imperative, though we understand that deciding to invest as an average young Nigerian can be one of the most difficult financial decisions to ever make.

As 29-year old Harry put it, “deciding to invest as a youth is all about discipline.” This is because, asides the fact that most youths’ incomes are limited, there are many things that money can be squandered on. However, discipline and a deep concern about one’s financial future can always help. So, be very concerned about your future and endeavor to make the right plans today.

“At a 12% interest rate per annum, the N50,000 he could afford to invest in TB monthly only yielded him N6,000 at the end of the year. This was not good enough for him” This calculation is wrong. At 50k invested monthly on a 12% interest rate PA, the total interest value would be between 38,000 to 39,000. I want to assume that investment is on a compounded basis.

uhmm…I don’t seem to get how you got 38,000 naira..note this is per Annum

“At a 12% interest rate per annum, the N50,000 he could afford to invest in TB monthly only yielded him N6,000 at the end of the *year”.

*month I guess was what d author meant to write