Daily performance of major economic indicators and highlights from trading sessions and key statistics such as Treasury Bills, bonds, Forex inflation, oil price.

- Funding Rates Moderate as FAAC Inflows Bolster System Liquidity

- BPE to raise N300b for 2018 Budget funding – Okoh

KEY INDICATORS

Bonds

The bond market traded on a relatively flat note, as supply pressures persisted, despite slight interests from clients on some mid and long tenured bonds.

We expect yields to maintain an uptrend, due to weaker client demand post the FGN Bond auction, and the continued uplift in T-bill rates on the long end of the curve.

Treasury Bills

The T-bills market maintained a slightly bullish posture, with yields moderating further by c.5bps on average. This came on the back of inflows from FAAC payments which bolstered system liquidty considerably, with the most interests from market players seen on the Jan – March maturities.

We expect the market to trade on a relatively calmer note in tomorrow’s session, as market players position for the NTB auction, where the CBN intends to rollover a total of c.N145bn in NTB maturities. Rates are expected to clear considerably higher, especially on the 364-day, due to the double hike in OMO stop rates from the last NTB auction.

Money Market

In line with our expectations, the OBB and OVN rates moderated by c.5pct to 9.50% and 10.33% respectively. This came on the back of inflows from FAAC payments (c.N382bn), estimated to have bolstered system liquidity to c.N490bn from c.N110bn opening today.

We expect rates to remain relatively stable tomorrow, as there are no significant outflows expected.

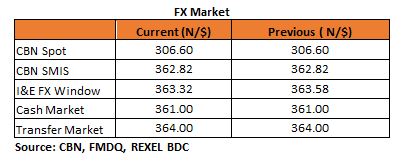

FX Market

At the Interbank, the Naira/USD rate remained stable at N306.60/$ (spot) and N362.82/$ (SMIS). At the I&E FX window, the NAFEX closing rate appreciated further by c.0.07% to N363.32/$ from N363.58/$ previously. Rates were however unchanged at the parallel market segment, with the cash and transfer rates closing at N361.00/$ and N364.00/$ respectively.

Eurobonds

The NGERIA Sovereigns weakened in today’s session, with yields trending higher by c.7bps. The weakest bonds on the day were the 2038s and 2047s which lost c.0.80pp.

The NGERIA Corps were slightly bullish, with interests seen on the DIAMBK 19s, ACCESS 21s Snr and UBANL 22s. We, however, saw better sellers on the FBNNL 21s.

Disclaimer:

Whilst proper and reasonable care has been taken in the preparation and accuracy of the facts and figures presented in this report, no responsibility or liability is accepted by Zedcrest Capital or its employees for any error, omission or opinion expressed herein. This report is not an investment research or a research recommendation and should not be regarded as such. The information provided herein is by no means intended to provide a sufficient basis on which to make an investment decision.

{kind=link}