Daily performance of major economic indicators and highlights from trading sessions and key statistics such as Treasury Bills, bonds, FX rates, inflation, oil price.

DMO Manages Auction Rates, With Slight Uptick on the 10-yr

FG proposes N8.73trillion for 2019 budget

KEY INDICATORS

Bonds

The bond market traded on a relatively flat note today, except for some speculative sales on the 2027 and 2028 bond towards the end of trading. Yields consequently ticked marginally higher by c.1bp on average.

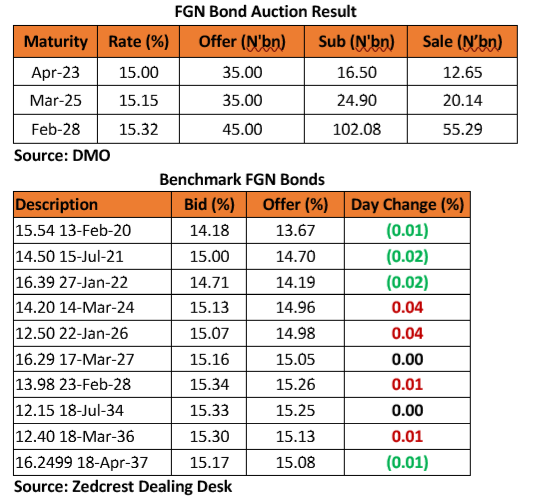

The Bond Auction by the DMO was moderately subscribed, with total bid size of c.N143bn received of the N115bn offered. The DMO however raised only a total of c.N88bn which was c.N8bn less than the c.N96bn sold at the previous auction. The DMO maintained rates on the 2023 and 2025 bonds at 15.00% and 15.15% respectively, while the clearing rate on the 2028 bond ticked higher by c.7bps to 15.32% from its level (15.249%) at the previous auction.

We expect slight demand on the 2028 bond tomorrow, while other bonds are also expected to compress slightly, in tune with the relatively moderate level of demand at today’s auction.

Treasury Bills

The T-bills market remained slightly bearish, with yields ticking higher by c.13bps on average. This came as market players remained under pressure from the relatively tight level of sytem liquidity, whilst expectation for a further OMO auction by the CBN tomorrow forced slight selloff on the longer end of the curve.

We expect yields to remain elevated due to expectations for the OMO auction tomorrow, and for a further tightening of system liqudity via a retail fx auction and bond auction settlement on Friday.

Money Market

In line with our expectations, the OBB and OVN rates remained elevated, closing today at 16.67% and 17.21%, as system liquidity remained relatively depressed at c.N62bn positive.

Despite the c.N284bn expected inflows from OMO maturities tomorrow, rates are expected to remain elevated, with the CBN expected to keep system liquidity tight via a further OMO Sale. We however note that the CBN is equally likely to refrain from conducting an OMO auction due to the huge amount of system outflows expected for a Retail SMIS and Bond Auction settlement on Friday.

FX Market

At the Interbank, the Naira/USD rate remained stable at N306.55/$ (spot) and N362.52/$ (SMIS). At the I&E FX window a total of $339.03mn was traded in 482 deals, with rates ranging between N350.00/$ – N365.00/$. The NAFEX closing rate depreciated slightly by c.0.02% to N364.01/$ from N363.94/$ previously.

At the parallel market, the cash rate appreciated by 30k to N360.70/$, while the transfer rate remained unchanged at N364.00/$.

Eurobonds

The NGERIA Sovereigns flattened out in today’s session, with yields closing relatively flat on the day, except for slight sell seen on the Nov 2027 bond (+5bps).

The NGERIA Corps were mostly flat, except for slight sell on the DIAMBK 19s and UBANL 22s.

Disclaimer:

Whilst proper and reasonable care has been taken in the preparation and accuracy of the facts and figures presented in this report, no responsibility or liability is accepted by Zedcrest Capital or its employees for any error, omission or opinion expressed herein. This report is not an investment research or a research recommendation and should not be regarded as such. The information provided herein is by no means intended to provide a sufficient basis on which to make an investment decision.

{kind=link}

God bless to the peoples of Nigeria, pmb and osj is continue 2019.