Bond Yields Trend higher as Market Players Stay Risk off

NASS Promises Minimum Wage Review before Year End

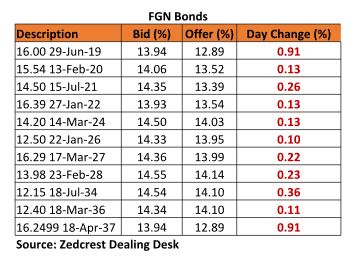

Bonds

The bond market remained bearish, with yields rising higher by c.26bps. This came on the back of some selloff on the longer end of the curve, consequently forcing spreads farther apart, with bids weakening significantly to c.14.29% on average. We expect yields to remain slightly pressured, due to the relatively weak local appetite and fears of continued offshore selloff.

Treasury Bills

The T-bills market traded on a slightly bearish note, with yields ticking higher by c.10bps, following some selloff, mostly on the shorter tenured maturities. This came as market players looked to free up some liquidity for funding of their wholesale FX bids. We however witnessed slight buying interests on the 4-Oct (92-day) maturity, in anticipation of client demand ahead of the PMA on Wednesday. We expect yields to trend slightly lower due to expected inflows from FAAC payments and OMO maturities later in the week.

Money Market

The OBB and OVN rates trended significantly upward by c.20bps to 30.00% and 32.50% respectively. This came on the back of provisioning by banks for FX sales by the CBN estimated at c.$210m (N70bn). System Liquidity was published at c.N150bn, up from c.N110bn in the previous session. We expect rates to remain relatively stable at these levels as there are no significant funding pressures expected tomorrow.

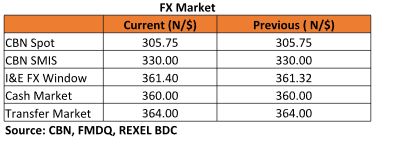

FX Market

The Interbank rate remained stable at its previous rate of N305.75/$. The I&E FX rate depreciated slightly by 0.02% to N361.40/$. In the parallel market, cash and transfer rates remained stable at N360.00/$ and N364.00/$ respectively.

Eurobonds:

The NGERIA Sovereigns traded on a mixed note, with investors buying the shorter end (21s and 23s), whilst selling on the long end (27s – 47s). Yields consequently ticked higher by c.1bp on average, with the most selloff seen on the 2032s which fell by –0.45pt.

The NGERIA Corps were mostly bearish, with selloffs witnessed on most of the traded tickers except for the FIDBAN 22s which witnessed slight recovery (+1.10pt) from its previous day selloff. The most selloffs were seen on the DIAMBK 19s, ACCESS 21s Snr and UBANL 22s.

{kind=link}