Ever wonder where your pension fund contributions are invested? Before we get to that, let’s share some interesting data about Nigeria’s pension industry.

Other News

Data from the Pension Commission reveals that a total of 7,823,911 workers make pension contributions in Nigeria every month. Data from the Pension Commission also reveals that we had about 932, 435 contributors in 2006 showing just how far we have come with pension contributions in line with the Pension Reform Act 2004 which was amended in 2014. The growth rate is an astronomical 4% per quarter or 16% per annum.

Total Pension Fund Asset Under Management (AUM) which is the total amount invested by Pension Fund Administrators (PFAs) was about N7.5 trillion as at February 2018. This amount is invested by different PFAs, depending on which one you use.

The PFAs invest this money into asset classes approved by the Pension Commission and have to use a combination of asset allocation skills, risk analysis, and timing to determine the best classes of assets your money is invested in. The Pension Commission periodically issues the breakdown of which asset class gets the most share of investing and it might surprise you if you are just reading this for the first time.

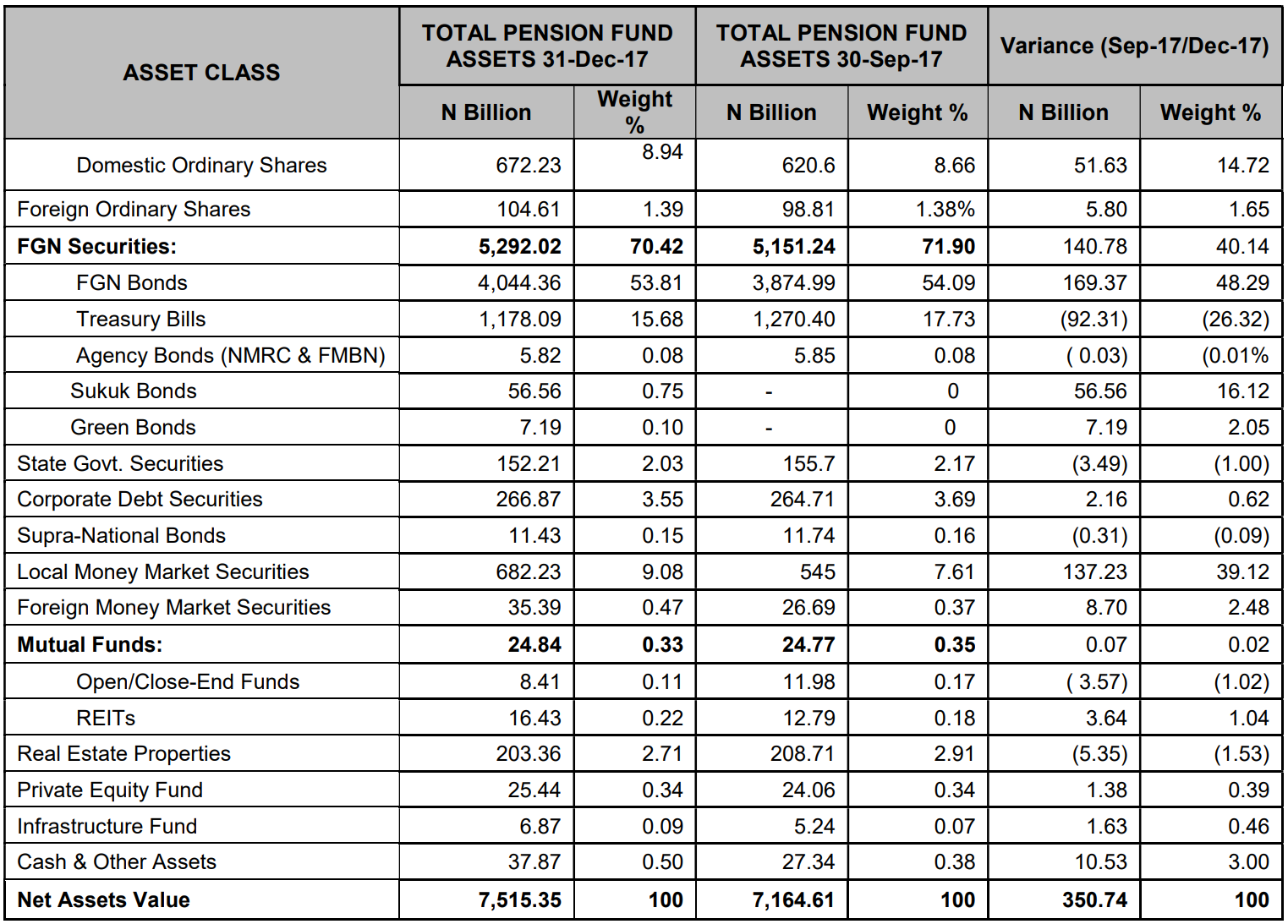

Here is the breakdown:

Based on the table above, Nigerian PFAs invest about 70% of pensions in FGN Securities. To break it down further, about 53.8% is invested in FGN Bonds and another 15.68% is invested in Treasury Bills.

Pension funds are allowed to take some risks and invest another 8.94% in shares and another 3.55% in Corporate Bonds. They are also allowed to invest in Mutual Funds and as at 2017, they invested 0.33% of funds under management in there. They can also invest in real estate and currently, they have about 2.71% invested.

Why invest in these asset classes

Let’s start with FGN Bonds. Nigerian Pension Fund Administration is very risk averse which is why most of their funds are in FGN securities. They believe that by lending to the Government, your investments have low risk and also enjoy some of the high-interest rates FGN Bonds offer.

The Federal Government uses the funds to run government business which includes, paying civil servant salaries, building roads and bridges, investing in healthcare and even paying the remuneration of members of the National Assembly. In return, the Government pays interest.

By investing in Equities, PFAs take a bit of risk and invest in shares just like anyone else. Despite the risk, shares fall within the top 5 of where pension funds put their money. Savvy investors typically study pension fund investment in equities because it is a good bellwether for how the stock market might perform.

When PFAs invest in shares, they do so because they want to earn dividends as well as some capital appreciation. They also have a Pension Index, which is compiled by the Nigerian Stock Exchange. The Pension Index includes the stocks that Pension Funds are allowed to invest in.

PFAs also invest in Mutual Funds to help diversify their portfolio. In investing, it is advisable that you spread your investment instead of concentrating them in a single portfolio. When you do so, you can better diversify your risk and possibly earn better returns over the long term. Mutual Funds, like Pension Funds, invest in different classes of assets. We also have some that are focused on a unique class of assets like Real Estate.

How this affects you

Finally, your pension funds are invested in a diversified set of asset classes which are meant to help protect your savings while giving you decent returns. Some analysts believe that Nigerian PFAs should be more aggressive and invest in riskier asset classes to improve returns. Some cynics believe that the government is happy with the level of investment they get because it means that they get a steady source of buyers for their securities, have minimal competition and can use the money for whatever they want.

They also control monetary policy and, as such, can raise interest rates or drop them depending on where inflation is. It is important to note that government action can also trigger inflation like it did during the exchange rate debacle of whether to float or not that hurt the naira between 2015 and 2017. Higher inflation rate also erodes the value of your investment in pension funds.

For example, last year, the best PFA returned 22.24% for its contributors. The first 8 returned at least above 16% for the year. If you adjust for the fact that inflation averaged about 15% last year, then perhaps it isn’t as good as it looks. Nevertheless, Nigerian PFAs should strive to return over 25% annually to give their contributors a decent inflation-adjusted return. That may not be possible if PFAs continue to invest 70% of their funds in risk-free government assets. There has to be a balance somewhere in between.

There is a dearth of investment vehicles into which they can invest. The investment universe in Nigeria is limited and I think Pencom doesn’t want to allow them to invest off shore; it would be another form of capital flight. They need to get the government to liberalise faster, open up the economy faster so as to expand investment opportunities for them.

PENCOM and the pension reform are good. But why are holders of pension savings accounts have to wait for more than 16 months on average to access their money?