Follow Us on Google Discover

Follow Us on Google DiscoverThe Central Bank of Nigeria a few weeks back concluded its monetary policy committee meeting increasing the rate at which the Central Bank lends money to commercial bank from 12% to 14%. That was the highest jump in history.

The effect of such price increases is that the lending rates equally move in the same direction ensuring that what lenders pay for their loans rises in tandem. Commercial lending rates have been in the northwards of 24% since the we started experiencing the drop in the price of crude oil.

With the MPR now increased, analysts also expect to see a movement in the rate at which the government pays when it borrows money from the public. It does this via Treasury Bills or Bond Issuance.

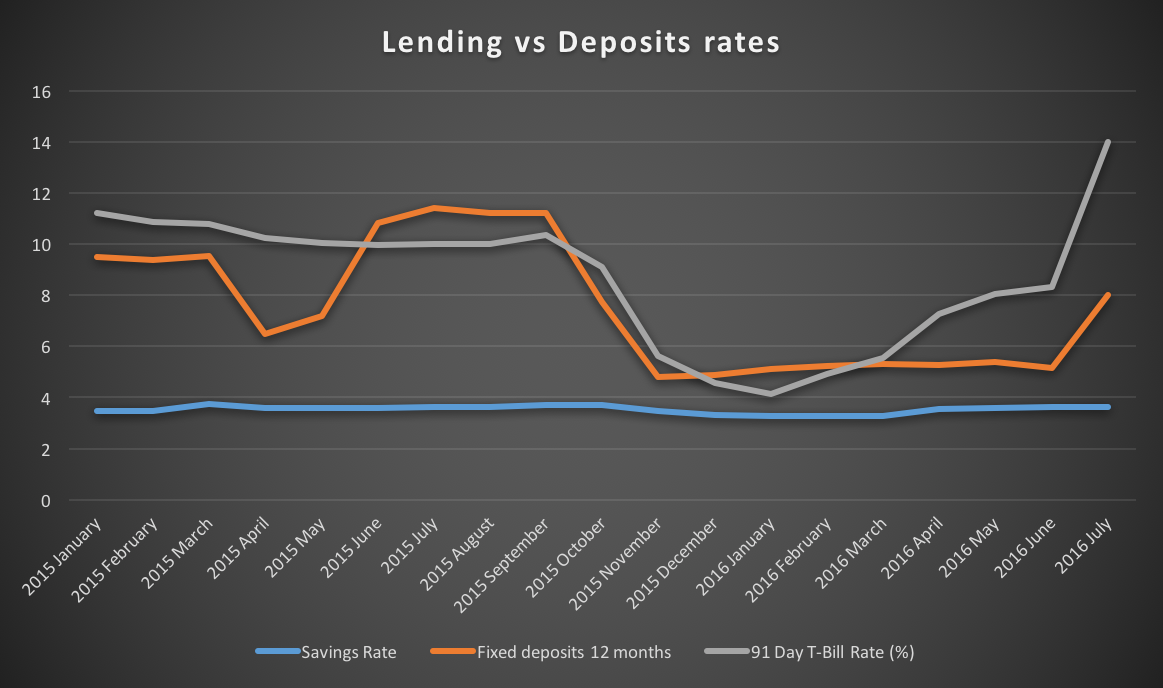

One rate which hardly follows policy rate changes are your savings deposit rates. As the chart below depicts, despite an increase in MPR and mending rates, deposit rates have remain stubbornly low. This is even more shocking when you consider that the inflation rate is currently at about 16.5%.

Also Read

Source: Nairametrics/CBN

What this means?

This basically means that idle funds kept in your bank account at an interest rate of about 3-3.5% is a waste of your money. You are probably better off depositing that money in fixed deposits. From the chart above, it is obvious that the treasury bills rates, which is the grey line is now much higher than the fixed deposits and savings deposit rates.

Nairametrics mostly recommends that idle funds be invested in treasury bills as they are safer and attract high yields. Instead of saving at a rate of 3-5% per annum and getting a negative real savings rate of -13% (savings deposit rates of 3.5% less inflation of 16.5%). The latest Treasury bills data shows a yield of about 19% for 182 days treasury bills.

Fortunately, I have learnt that savings account is not the best way to save money and I have since embraced fixed deposit. The only challenge is fixed deposits usually have higher minimum starting amounts so out of reach for a lot more people. Again, taking it further to T-Bills, how can one personally invest in T-bills, would brokers not be required?

You don’t need brokers. Just go straight to your bank and ask to fill a form. Within 20 mins you will be done

Really? Wow! Interesting. SO how about minimum amount and how does one monitor the whole process and get the money out?

Surely there should be a Minimum Value for I vesting in T-Bills right? Please what’s the Minimum?

Yes please whats the minimum value for investing through the bank

Minimum is N10k

Thanks for the info, a lot of people do but know about treasury bills

Thanks for these awesome article. So how can i go about investing in treasury bills?

Thanks for this great article, how can go about investing in treasury bils?

This is really good. Thanks for sharing investment opportunities in TBills.

Interesting post… I learnt my lesson a long time ago

Yea that’s true Kay you have a point.

I agree with you sir, nice share.

Sir, your write up on idle fund was written in August 2016, but now in 2020, where can one invest his or her idle money because both savings and treasury bills rates have fallen to almost zero.