Renaissance Capital (Rencap) released an Op-ed this week that suggest Naira should be devalued on the back of a similar devaluation by Kazakhstan. The article has attracted support and criticism from both side of the devaluation argument and goes to display what really is at stake for everyone who is for and against the Naira devaluation.

Here is the article;

- Kazakhstan devalued the tenge by 22% to KZT253/$1 and has allowed for a move to a more flexible exchange rate. Could Nigeria do the same? We think the most likely outcome for Nigeria, is a slightly smaller (15-20%) move, and a managed float, over a free float.

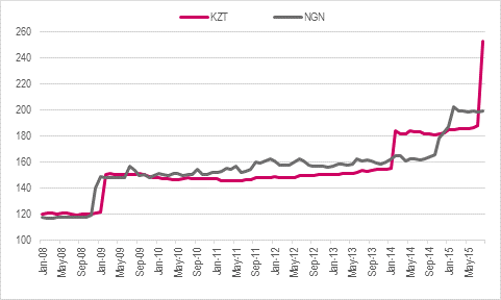

- Why do investors compare Nigeria with Kazakhstan? Two parallels that are drawn between Nigeria and Kazakhstan are that they are both big oil exporters and their currencies have followed similar trajectories in recent years (see Figure 1). Most notably, both countries’ central banks devalued their currencies within 10 weeks of each other in 2008-09; Kazakhstan actually devalued its currency after Nigeria. The plummeting oil price triggered both devaluations.

Figure 1: Exchange rates – NGN/$1 and KZT/$1

- The last time the Kazakhstan devalued the tenge – by 20% in February 2014 – Nigeria did not follow suit, because the oil price was well supported at the time. One may recall, that the context of the KZT devaluation in February 2014 was that Kazakhstan had joined the customs union that includes Russia, which has a similar economy, and with the rouble weakening, Kazakhstan became worried about Dutch disease. This time around a plummeting oil price has triggered the KZT devaluation and we believe will do the same in Nigeria, either via a sharp one-off move or multiple step changes.

- How much do we expect the NGN to move? The NGN is 20% overvalued, according to our real effective exchange rate analysis (see our 13 July note, Sub-Saharan Africa’s currencies: Which are most vulnerable? click here). That implies the exchange rate should be at c. NGN240/$1. However, the central bank’s fixation on a strong naira, which is evident from the succession of restrictive policies (including tightening of monetary policy and FX rules, as well as the de facto ban of 41 imports) it has put in place over the past year, to defend the naira, leads us to believe that any devaluation is likely to fall short of the naira’s fair value. Hence our NGN230/$1 view at YE15.

- Risk scenario: The slide in the oil price (below $50/bl) raises the risk of a sharp one-off move, over a more gradual depreciation, and it also increases the risk of a bigger than 15% depreciation before YE15.

- Managed float vs free float. We gathered from our most recent discussion with the Central Bank of Nigeria that a move to a managed float, from the current fixed peg is most likely following an adjustment in the exchange rate. We believe a free float is a low probability outcome. However, the if an oil price of below $50/bl proves to be durable, the more difficult it will become for the central bank to avoid a free float.

{kind=link}