Unilever Nigeria Plc. (9 months ended September 2014)

- Unilever Nigeria Plc (Unilever) released unaudited results for 9 months ended 30th September 2014 wherein revenues declined 4.3% YoY to N43.6 billion while PBT and PAT fell 49.5% and 48% YoY to N2.5billion and N1.8billion respectively.

Tight trading environment drives revenue contraction…

- At N14.3billion, revenues are 10% lower YoY and 15% behind our forecasts for the seasonally strong Q3 14. This reading fits the negative growth patterns recorded across coverage consumer goods companies thus far and suggests generally tight trading environment.

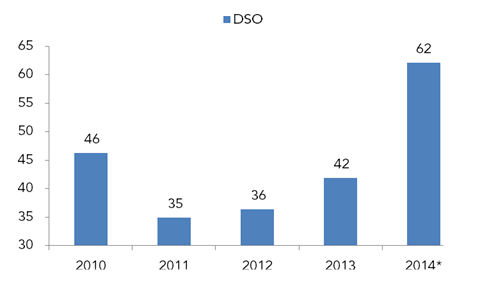

- As with closest peer PZ which noted intensifying competition in the HPC segment, we believe Unilever’s topline weakness stems from further pressures on HPC front (~60% of revenues) in addition to the softening contribution from its northern operations which accounts for 30% of sales. In line with the flagging growth trends across the sector, Unilever’s days sales outstanding jumped 71% YoY to 61days vs. 4-year average of 40 days which provides firm hints about underlying struggles with volume growth.

- …But downtrend across commodities underpins gross margin expansion

- As with peers, the benign commodity price trends continued to induce input cost gains with Q3 14 COGS declining faster than revenues (-15.3% YoY to N8.6 billion) resulting gross profits largely flat from Q3 14 at N5.8 billion. We believe this reflects the downtrend in key inputs for Unilever – Crude Palm Oil (-4% YoY, -15% YTD) and oil prices (-7% YoY, -23% YTD) and helped account for the 380bps YoY expansion in gross margins to 40.1%.

Nevertheless, opex increases neuters input cost gains

- In line with Unilever’s guidance to increased marketing and distribution expenditure over FY 14, OPEX rose 10% YoY to N4.8 billion during the quarter, though at a more tempered pace than H1 14 levels (+27.6% YoY), resulting in opex-to-sales climbing 610bps YoY to a record high 33.5% (Q3 14E: 23.2%). Thus Q3 14 EBIT declined 33.9% YoY to N952 million with related margins 240bps lower YoY at 6.6%.

Higher finance costs exacerbates earnings weakness

- Net finance charges rose 32% YoY to N484 million on account of a cutback in finance income (-74% YoY) and slightly higher finance costs (+4% YoY) which respectively reflect lower cash balances (-28% YoY to N1.8 billion) and a two-fold YoY expansion in borrowings to N14.1 billion.

- Overall, revenue weakness and elevated opex expenditure scarred Q3 14 performance with PBT and PAT declining 56.4% and 53% YoY to N469 million and N357 million respectively. Corresponding margins contracted 350bps YoY and 230bps YoY to multi-year lows of 3.3% and 2.5%.

FVE to trend lower on higher opex and interest expense expectations

- The sizable deviation from our forecasts are likely to drive moderation in our full year expectations for Unilever. Farther out, we are likely to raise our opex assumptions slightly higher than previous to reflect the rising trend in recent quarters. Similarly, the uptrend in borrowings which have risen on average 55% YoY over 2014 should result in higher interest expense in coming quarters. In sum, we still see sizable scope for earnings compression in coming quarters which should result in downward revisions to our FVE estimate for Unilever.

- Unilever trades at a current PE of 48.4x vs. 21.7x for Bloomberg Middle East and Africa peers. Although Unilever has declined 18% since our last update, its last trading price remains at a premium (11%) to our FVE (N35.5). We maintain our SELL rating on the stock on valuation grounds.

{kind=link}