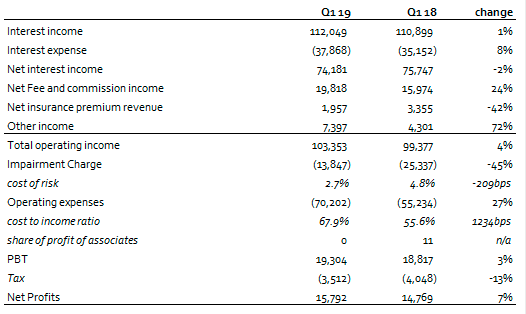

FBNH’s latest financial report for Q1 2019 showed that Interest Income grew marginally by 1% y/y to N112.0bn. We believe this was largely due to the decline in Net Loans to customers, down 12% y/y to N1.67trn in Q1 2019.

Interest Expense on the other hand was up 8% y/y to N37.9bn: This was driven mainly by an increase of 120% y/y to N7.2bn in interest paid on deposits from banks.

Meanwhile, Customer Deposits grew 8.3% y/y to N3.52trn, with low cost deposits making up 78% of total deposits. Overall, the bank’s Net Interest Income declined marginally by 2% y/y to N74.2bn in Q1 2019.

Net Fee and commission Income grew strongly in Q1 2019: Specifically, this was up 24% y/y to N19.8bn. The sturdy growth in Net Fee and Commission Income was mainly on the back of the significant growth in e-banking income (up 83%y/y), account maintenance fees (up 8% y/y) and brokerage fees (up 95% y/y). Surprisingly, Credit related fees grew 28% y/y despite the declining loan growth.

Other Income growths were recorded: Net gains on FX, Net Insurance Premium, Net gains on investment securities, Net gains or loss on financial instruments, Dividend Income, and other Operating Income grew 72% y/y to N7.4bn in Q1 2019 from N4.3bn in Q1 2018.

Impairment Charge declined: It declined 45% y/y to N13.8bn, compared to N25.3bn in Q1 2018; thereby resulting in a decline in Cost of Risk (COR) to 2.7% compared to 4.8% in Q1 2018. Based on our discussion with management, Atlantic Energy, a major exposure of the bank that is partly responsible for its high NPL ratio of 25.9% as at FY 2018, has been fully provided for.

OPEX grew significantly: It was up 27% y/y to N70.2bn in Q1 2019 from N55.2bn in Q1 2018. This negative, completely offset the single digit growth in total Operating Income (up 4% y/y to N103.4bn), thereby leading to a deterioration in cost to income ratio ex-provisions to 67.9% in Q1 2019 compared to 55.6% in Q1 2018.

Pretax Profit Showed Increase: Despite the rise in Operating Expenses, Pretax Profit grew marginally by 3% y/y to N19.3bn in Q1 2019, up from N18.8bn in Q1 2018. Net profits also grew 7% y/y to N15.8bn Q1 2019 from N14.8bn in Q1 2018. Annualised RoAE also improved to 12.0% in Q1 2019 from 9.0% in Q1 2018.

Our recommendation: We have a Buy rating on the stock with a target price of N12.27/s. Current price: N7.25/s.

________________________________________________________________________

CSL STOCKBROKERS LIMITED CSL Stockbrokers,

Member of the Nigerian Stock Exchange,

First City Plaza, 44 Marina,

PO Box 9117,

Lagos State,

NIGERIA.