Money Market: The money market rate increased last week as the Overnight rate (OVN) and Open Buy Back (OBB) rose to 10.00% and 9.14% from 5.93% and 5.29%, respectively. Consequently, the average money market rate increased by 3.96% to settle at 9.57% due to outflow seen on Monday which caused the money market rate to grow significantly.

The System Liquidity is estimated to have increased to close at cN590bn from cN250bn from previous week. Major Inflow for the week included: OMO Maturity of cN151bn, CBN retail refund of cN250bn, and inflow from CBN discounted promissory note.

Major outflow for the week, on the other hand, included: Weekly Wholesale, Invisible, and SME FX auction of $210m, OMO Sales of c N456.38 (c N312.38bn on Monday and c N144bn on Thursday). Barring any significant inflow this week, we expected the money market rates to inch upward as the CBN issue OMO.

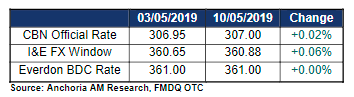

Forex: USD/NGN: The CBN Official rate rose marginally by 0.02% last week to close at N307.00/$ while the rate in the Investors and Exporters’ FX Window inched slightly up by 0.06% to close at N360.88/$, despite an increase of 12% in average market turnover during the week.

However, Naira at the parallel market remained unchanged to close at N361.00/$ (using the Everdon BDC Rate). We expect rates in the parallel market to remain constant as the apex bank continues to supply FX into the market, coupled with its frequent Wholesale and Retail SMIS programme.

Commodities: Brent Crude Oil and WTI Crude Oil fell by 0.32% and 0.45% to close at $70.62 and $61.66 per barrel respectively, despite geopolitical tensions between the United States and Iran. The fall in the crude oil price was due to uncertainty surrounding global trade as the tension between US and China continues.

Fixed Income

Bond: FGN: The Bond Market closed on a bullish note last week as average yields fell by 12bps to close the week at 14.06%, following the news of re-appointment of the CBN Governor for another five-year term.

Yield across all maturities fell with the exception of the longest tenor bond (2049) which rose by 3bps. Notable last week was the activities on 2023, 2034 and 2027 bonds, with yield declining by 62bps, 41bps, and 32bps respectively.

We expect the bullish to continue in the bond space as market participants anticipate a decline in the rate of short-term instruments at the auction.

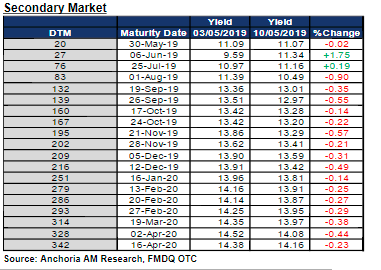

Treasury Bills: The secondary treasury bills market closed on a bullish note last week due to a relatively buoyant liquidity. The average yield fell by 21bps to close at 12.91% from

13.13% in the previous week.

During the week, the CBN renewed its liquidity mopping activities with

spot rate on issued OMO falling across tenors.

——————————————————————————————————

CONTACTS

Anchoria Asset Management Limited

5th Floor, Elephant House

214, Broad Street

Marina

Lagos

Investment Research research@anchoriaam.com +234 908 720 6076

Wealth Advisory investor-relations@anchoriaam.com +234 818 889 9455

Anchoria Asset Management Limited

5th Floor, Elephant House

214, Broad Street

Marina

Lagos

Investment Research research@anchoriaam.com +234 908 720 6076

Wealth Advisory investor-relations@anchoriaam.com +234 818 889 9455