Daily performance of major economic indicators and highlights from tradings sessions and key statistics such as Treasury Bills, bonds, FX rates, inflation, oil price.

Money Market Rates Compress Further As CBN Stays Mute on OMO

***Oil Hits 2019 High as Demand Outlook Brightens***

Key Indicators

Bonds

The FGN Bond market opened the month on a relatively flat note, with slight demand on the 2025s offset by sell pressures on other maturities. Average bond yields consequently remained unchanged at 14.35%.

The market has maintained a slightly bearish posture in recent sessions, with some players still looking to take profit at current levels. We expect this trend to persist in the near term.

Treasury Bills

The T-bills market traded on a slightly bullish note, with yields compressing marginally by c.5bps due to the continued absence of an OMO auction by the CBN and the improved system liquidity levels from FAAC inflows in the previous session.

We expect the slight moderation in yields to persist as market players look ahead to the NTB auction scheduled to hold on Wednesday.

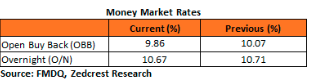

Money Market

Rates in the money market fell by c.5pct down to single digit levels as system liquidity was bolstered significantly to c.N325bn positive following the inflows from FAAC payments in the previous session, even as the CBN continued to hold off on an OMO auction.

We expect rates to remain relatively stable, barring a renewed OMO sale by the CBN.

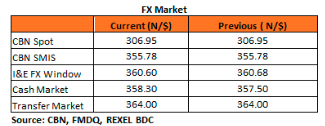

FX Market

At the Interbank, the Naira/USD rate remained unchanged at N306.95/$ (spot) and N355.78/$ (SMIS). The NAFEX closing rate in the I&E window appreciated by 0.02% to N360.60/$, whilst market turnover dipped by 57% to $156m. At the parallel market, the cash rate fell back to N358.30/$ whilst the transfer rate remained unchanged at N364.00/$.

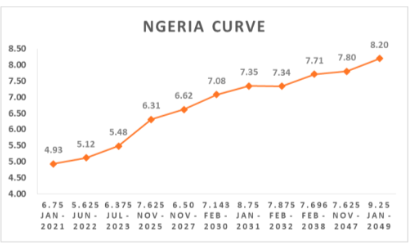

Eurobonds

Investors remained slightly bullish on the NGERIA Sovereigns, with yields declining further by c.6bps on the day. This is coming as growth fears in developed markets subside and investors renew risk on bets in choice EM assets.

In the NGERIA Corps, we witnessed renewed interests on the UBANL 22s.

__________________________________________

Contact us:

Dealing Desk: 01-6311667 | Dayo: 07032208237 | Seyi: 08023231396 | Nnamdi: +2348133385000 | Tosin: +2347039394376

Email: research@zedcrestcapital.com