The way Buhari is going it’s like all of us will die so that naira will live – M

The rapid deterioration in the naira at the parallel market is popping up on screens and discussion boards everywhere. Individuals are deciding whether to jump into the dollarization band wagon or remain ‘fencist’. For businesses, the rapid spiral is forcing firms to re-write previously drawn up contingency planning as the naira breaks to record lows. All this while the official rate remains, as an ostrich, buried in the sand at N199 backed by patriotic innuendos and views that it is appropriately priced at the current level.

To counter calls for a downward adjustment in the naira peg, policy wonks at the apex bank and the presidency and social media ‘commentariat’ often frame devaluation as a sort of policy alternative with merits and demerits. It is to this class that this article is targeted at. There’s no need for complex arguments and the sort. I will try as in earlier columns to put forward the case for devaluation as a conclusion from numbers. In my first piece I tried to simplify this gap but the thing with the anti-devaluation gang led by President Buhari is that they consistently elect to situate the devaluation argument in the realm of words and policy and not in numbers. The argument for devaluation today is just simple – adjusting the realities of lower dollar supply occasioned by oil prices. To retain a static position despite a tectonic shift on the ground on which the NGN sits would be an exercise in futility.

Since June 2014 oil prices have crashed by over 70% from the golden $100/barrel years between 2011 and 2014 to an average of $31/barrel in January 2016. Using CBN data, oil inflows into the official FX reserves which averaged $40 billion per annum between 2011 and 2014 plunged to $19billion in 2015. Oil receipts accounted for well over 90% of Nigeria’s foreign reserves and by and large robust oil prices provided the fire power for the CBN to declare that USDNGN rate

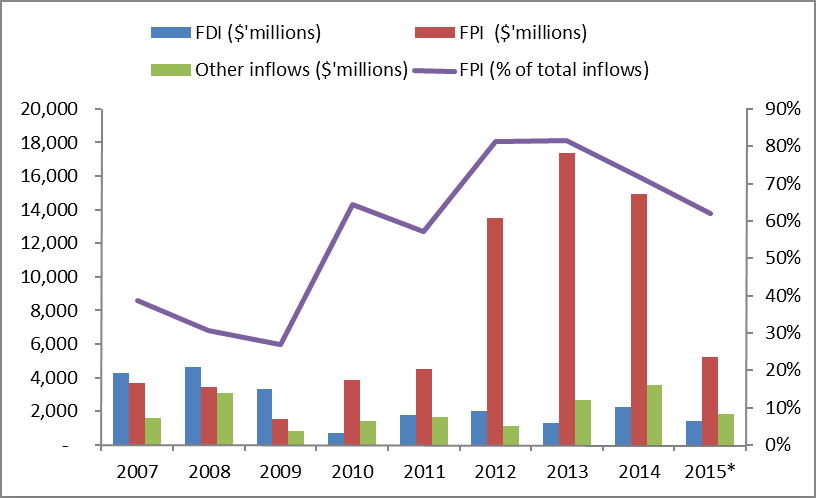

To buffer up its position, the CBN entered into countercyclical tightening (despite inflation was declining over the period from its long term trend average) to attract foreign portfolio investors using a combination of base rate hikes, increases in reserve ratios and aggressive open market operations. Basically the CBN stifled domestic activity for the interest of FPI to support the currency. In hindsight the tactic worked as during the period the US Federal Reserve was pumping $85 billion a month into global financial markets which was resulting in a sort of reverse osmosis – cash moved out the low interest rate environments to the high rate environment of emerging/frontier economies like Nigeria. Over 2012-2014, CBN data clocked in roughly $15billion dollars per annum of fickle foreign portfolio investments into Nigerian equities and stocks. On the contrary, the more stable sort of capital flows – Foreign Direct Investments- declined over the period. To hasten the attractiveness of Nigeria to the world, the then CBN governor loosened previously imposed capital account restrictions which placed a one year holding period on FPI flows. In doing so, he increased the exposure of the Nigeria’s immature financial markets to the speed, dynamism and trickery of the foreign investor. Simply he made us vulnerable to a sucker punch when the fickle investors headed for the exit doors.

Figure 1: Capital Account Flows

Trouble began with termination of the quantitative easing program in 2014 and the collapse in the oil price over the year resulting in a proper osmosis as FPI flows exited developing countries, picking up speed out of oil exposed countries back to whence they came. Thus Nigeria was hit with a double whammy – reducing FPI flows and lower oil export receipts leading to a dollar supply shortage.

With the 70% drop in oil prices, it’s a simple conclusion that the apex bank’s ability to defend the naira has eroded to a large extent by a similar magnitude. How can we adjust to the 70% drop? There are several options. Firstly, as some countries have done simply ignore the drop and use reserves to defend the value of your currency such as Saudi Arabia and the rich gulf nations with reserve levels over $100billion have done. This works because you reserve levels are too much relative to dollar demand. (Imagine today the CBN got $100billion vs. $27billion). Another way of adjusting is to pass on the shock by debasing (or devaluing/ weakening) your currency which Russia has done. Alternatively, you can suppress your dollar demand to zero and trudge along without adjusting the FX rate.

Lastly you can adopt a combination of policies by using reserves and devaluing and hoping to patch through which is what the CBN is doing. The apex bank devalued the NGN by roughly 25% since the start of the crisis, used reserves which have dropped 37% since the start of the crisis and tried to suppress import demand which dropped 10-15% since the 2014.

The problem with use of reserves is that, borrowing an accounting concept you are trying to solve an income statement problem with a balance sheet item. Unless reserves are high enough it will fail. Even worse starting in the second half of 2014, the CBN began entering into FX swap arrangements to the tune of $9.8billion with only roughly $5billion of those liabilities being repaid, which implies the 30-day moving average should be reduced by the remainder $4.8billion obligations in making comments about CBN ability.

Moreso, economic agents in the rush to protect them are frontloading demand meaning more trouble at the door. I think running through these numbers its clear a dollar funding gap exists. CBN resort to the gap is to outlaw a lot of items in the gap in the hope that they die out – banning 41 items, cutting off BDCs from official supply. Having been kicked out of the official these guys move to the parallel segment to survive heaping more pressure at the segment and driving the rate higher. Simply unless imports crash at the speed of the oil price collapse, fiat declarations to curtail import demand won’t work.

Table 1: Selected economic data

| 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | |

| Bonny light – mean ($/barrel) | 79.76 | 113.15 | 113.72 | 110.99 | 100.40 | 53.21 |

| % Change | 41.9% | 0.5% | -2.4% | -9.5% | -47.0% | |

| CBN Oil Inflows ($’millions) | 26,163 | 41,329 | 42,556 | 36,982 | 38,625 | 19,271 |

| % Change | 58.0% | 3.0% | -13.1% | 4.4% | -50.1% | |

| CBN annual dollar sales | 30,172 | 41,188 | 27,549 | 35,234 | 48,056 | 33,332 |

| Foreign reserves year end | 32,339 | 32,640 | 44,178 | 43,611 | 34,469 | 29,070 |

| % Change in foreign reserves | 0.9% | 35.4% | -1.3% | -21.0% | -15.7% |

So the obvious question is who bears the brunt of the remaining gap? This is where the anti-devaluation argument swerves into theory, argument, ideology and patriotism. There’s no free lunch anywhere, failure to transmit the terms of trade shock to the currency value means someone is paying for the free lunch. The question really is not about why or why not to devalue but when are we going to act to stem the declining FX reserves. We can still argue now over whether to devalue or not because we have reserves – when reserves reach crisis lows the choice will be worse. So why are we waiting? Effectively our posture means we are simply betting that oil prices will recover in time to stave off reserve depletion. So that’s what it really is the anti-devaluation argument is premised on stalling to take the bitter pill till oil prices recover. It’s not about preventing the poor from suffering as President Buhari put it? If it were then what was the intent in raising kerosene prices by 66% in January and hiking electricity tariffs by roughly 50-70% in February? Saving the poor as well?

At this point a line from the book Why Nations Fail by Acemoglu and Robinson comes to mind. It goes African leaders are not unaware that a particular policy is bad. They do and have well trained advisers and economists to do dirty data work. However, African leaders are not voted into office by financial markets but rather by voters so effectively policy choices boil down to what leaders feel they can get away with not what is actually required.

I doubt our president or his advisers are unaware of data pointing to the fundamental case for devaluation. They are simply playing to a different audience. It is ironic that a party which was voted on a mantra of change is resisting the need to change a stance out of sync with the horizon. An FX rate is a price so why should a price be constant when everything is in flux? Prices as with everything in life, including APC’s mantra, must change when the environment demands changes. Mr. President the streets await your ‘change’.

All data and charts sourced from the CBN

Follow Walle on twitter @walesmit