Let us do a quick exercise before diving into this week’s note. Need you to raise five fingers up.

- Put a finger down if you were not shocked by the Q4 GDP output.

- Put a finger down if you expect a FY GDP of -1.92% YoY or less.

- Put a finger down if you expected Nigeria to be out of a recession in Q4 2020.

- Put a finger down if you expected the agricultural sector to experience its strongest output in 16 Quarters.

- Put a finger down if you expected that the agricultural and service sector will outperform in Q4 2020.

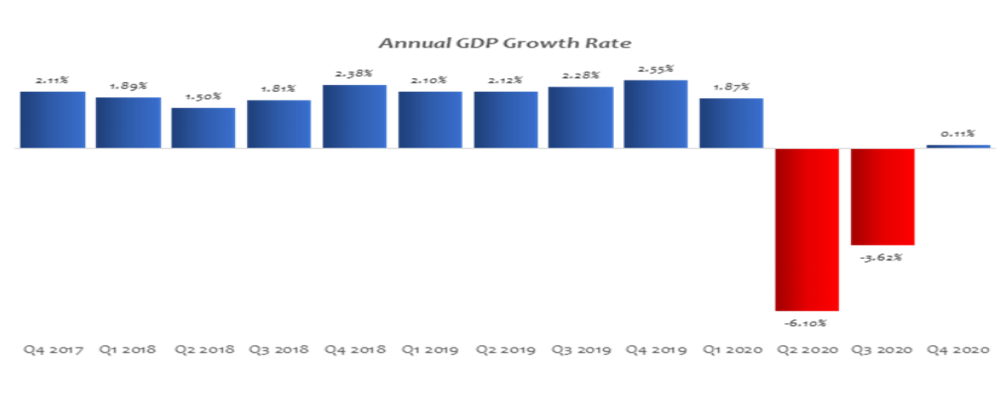

If you still have all five or four fingers up, you are not alone in this as the Q4 2020 GDP figures came as a shock, beating consensus expectation of another decline in Q4 2020. If you have all your fingers down, I would like to know where you got your crystal ball. Nigeria’s Gross Domestic Product (GDP) grew by 0.11%(year-on-year) in real terms in the fourth quarter of 2020, representing the first positive quarterly growth in the last three quarters. Overall, in 2020, the annual growth of real GDP was estimated at –1.92%, (vs IMF’s -3.2% YoY). To avoid responses like, “it’s the Lord’s doing”, we will be diving into the sectors that were responsible for this growth.

GDP

We will resist the temptation to lean into unproven narratives of statistical manipulation but rather attempt to demystify the GDP numbers by identifying the activity sectors that spurred the reported growth. An examination of the performance of the sectoral trinity, consisting of Agriculture, Industrial, and Service, helps provide a sense of meaning to the reported growth. In the review quarter, the Agriculture and Services sectors grew by 3.42% and 1.31%, respectively, and these two sectors jointly contribute 81.23% to the GDP of the country, hence, driving the overall GDP growth.

The growth recorded in the agricultural sector is the highest seen in sixteen quarters, but we unfortunately, cannot attribute the improved performance to the huge influx of funds that the fiscal and monetary authorities have been pumping into the sector through schemes like the Anchor Borrowers’ Programme. Rather, the lid placed on food importation via the border closure and the limitations on FX access for certain categories of food importers tipped the scales of demand and supply in favor of domestic agricultural players. Also, agricultural growth was underpinned by a 3.68% and 2.38% improvement in crop production and livestock subsectors, respectively. So, you can seek solace in the agricultural sector growth when next you go food shopping and are faced with soaring prices. For the service sector, the improvement was driven by the growth in the Information and Communication (14.70%) and Real Estate (2.81%) sectors, both of which jointly account for 40% of the service sector. The real estate performance marked the end of a six-quarter decline.

The GDP recovery offers no thanks to the oil sector, as it only deepened its downtrend. The oil sector in the fourth quarter of 2020 recorded a real growth rate of -19.76%, which makes the -13.89% recorded in the second quarter of the year look somewhat good. The blame for this poor oil performance can be largely attributed to lower production levels, as we recorded a YoY production decline of 22.00%, with oil production averaging 1.56mbpd in the review quarter as against 2.00mbpd recorded in the corresponding quarter of 2019. The explanation for the drop in production can be traced to domestic production disruptions, as well as output limitation by OPEC+. Back in 2017, a recovery in the oil sector was instrumental to the emergence of the country from the recession, but over the years, the non-oil GDP contribution has gradually encroached into the oil sector’s quotient, increasing from 91.21% in the second quarter of 2017 to 94.13% in the fourth quarter of 2020. This helps provide more meaning to the recent GDP growth seen, as a non-oil recovery weighs more on the performance of the overall GDP, while the oil sector’s impact gradually diminishes.

The fourth-quarter GDP performance was magical and unexpected, but there is still enough room for worry. The weak recovery recorded is expected to be the first of many tepid growth rates, and such economic sluggishness should last through 2021. The structural problems of the economy remain, hence, the chances of the economy recording sustainable growth seem bleak.

All Yields are heading north…

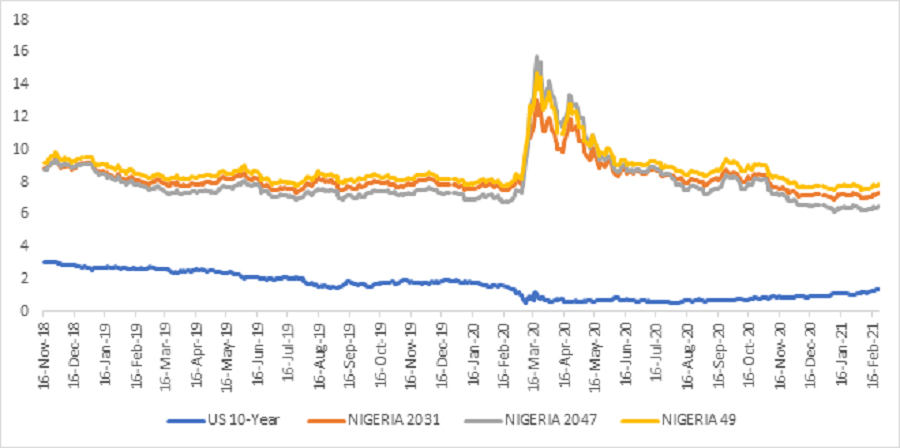

It seems we are not the only country experiencing a rise in fixed income yields. The yield on the United States benchmark 10-year Treasury notes climbed to a one-year high of 1.36% on Monday. Since the beginning of February 10-year yields have risen about 26 basis points, on track for their largest monthly gain in three years. Unlike the Nigerian fixed income yields which have been on the upward trajectory largely due to a sharp decline in the market liquidity chasing excess supply of securities. The rise in US Treasury yield has been hinged on inflation expectations as the vaccination programme gains momentum while stimulus expectations continue to drive a positive outlook for the economy in the near to medium term. The stock market also felt the brunt of the fast rise in yields as the S&P 500 was down 0.22%, while the Nasdaq Composite slumped 1.53% on Monday. However, the Dow Jones Industrial Average rose 0.39% or 144 points.

US 10-Year Treasury vs S&P 500

Looking at the chart above, it seems the United States defied the theory that states that there is an inverse relationship between the yields in the fixed income market and the equities market, as yields in the fixed income markets and equities market had a positive correlation between the period of August 2020 to January 2021. (One word, Reflation Trade)

Reflationary trades involve buying assets exposed to faster economic growth, price pressures, and higher yields. Riskier equities tend to benefit at the expense of haven assets such as the U.S. Treasury. Equities that benefits are small caps and cyclical sectors such as banks and energy producers. It also includes cruise operators, airlines, and other travel and leisure companies that will benefit from an end to lockdowns. It’s the go-to trade when economies emerge from a recession. This begets the question, “would we see reflationary trades in Nigeria given that we just came out of a recession?”

Spread Analysis (US 10-year yield, NIGERIA 31 and NIGERIA 49)

If U.S. Treasury yields continue to rise, central banks in emerging markets may need to hike rates to sustain foreign inflow. We might be looking at an end to the global central bank dovish stance sooner than expected. From the Eurobond perspective, the NIGERIA 31, NIGERIA 47, and NIGERIA 49 have traded at a three 3-year average spread of 670 bps, 650 bps, and 720 bps of the U.S. 10-year yield in the past 3 years.

Given the U.S. 10-Year yield current spread differential of 600 bps, 520 bps, and 650 bps between the NIGERIA 31, NIGERIA 47, and NIGERIA 49s, we expect a further rise in yields across the Nigeria sovereign papers.