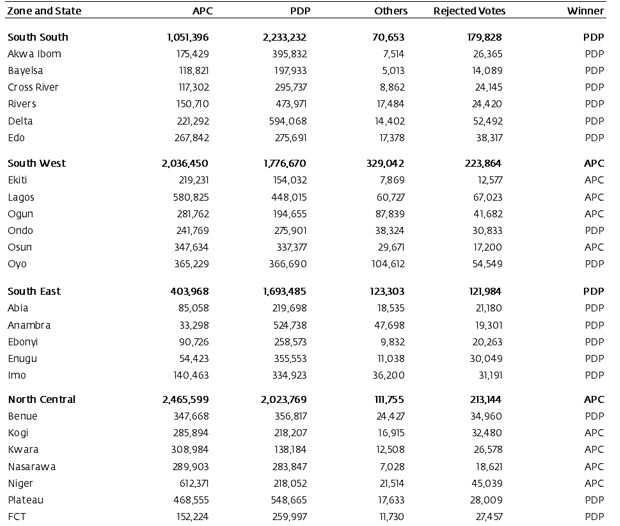

- This morning’s announcement of election results saw the All Progressives Congress (APC) of President Muhammadu Buhari retain the presidency, defeating the challenge from the Peoples Democratic Party (PDP) of Atiku Abubakar.

- This implies a continuation of government based on firm regulation and security. However, while Buhari’s first term sailed into the oil price crash of 2015 and the recession of 2016, economic conditions are different – arguably better – now.

- The APC’s renewed majority in the Senate is significant. The Senate proved frustrating to Buhari’s agenda in his first term, 2015-19. Expect the budget to be passed quickly this year.

Foreign currency

Nigeria will almost certainly continue with a managed exchange rate. As we argue in Coronation Research: Year Ahead 2019, A Year of Two Halves, 15 January, the Naira is within 10% of its fair value, so fundamental pressure to revalue it is weak. FX reserves are US$42.4bn, which we calculate is compatible with Naira/US$ stability, at close to NGN363/US$1, for the rest of 2019.

Interest rates

The Central Bank of Nigeria (CBN) currently offers a risk-free-rate 587bps above inflation, which keeps foreign investors in Naira money markets. As we argued in January, if inflation trends down mid-year, there may be scope for rate cuts in Q4, or even Q3.

Equity market

There was a brief pre-election rally, which partly unwound last week. High economic growth rates were not a feature of the last APC administration. That said, the trend in non-oil GDP growth, evident in recent data, suggests that the economy is doing better than earlier thought. As we argued in January, we believe that under such conditions there is upside risk in bank stocks.

Development and growth implications

Political implications

The international context. Last Saturday’s elections proceeded, for the most part, without violence, and the Independent National Electoral Commission (INEC) went about its business in a businesslike way (albeit after a one-week delay). These facts are likely to be seen with relief by the international community.

Inevitably, there are allegations of irregularities. However, in the African context of a highly contentious electoral outcome in the Democratic Republic of Congo late last year, and hotly-contested elections in South Africa due later this year, Nigeria looks stable and orderly (though perhaps not quite as hopeful as Ethiopia after the election of a youthful and reforming Prime Minister last year).

At the same time, the political picture in Nigeria is not entirely settled. There are still governorship and state assembly elections to be held on 9 March, and in some of Nigeria’s 36 states we expect these to be hotly-contested.

The domestic context

A feature of President Buhari’s first term was the conflict between the President and the Senate. Despite the APC having a majority in the Senate, it was a Senator with opposition sympathies (he later defected to the PDP) who held the Senate presidency.

Friction between the executive and legislative arms of government was a recurring theme during President Muhammadu Buhari’s first administration, 2015-19. The President depended, more than the previous administration, on executive orders where possible. The most serious example of his conflict with the legislature came with the six-month delay in the passage of the 2018 budget, which represented the longest ratification cycle for any full-year budget since 2000. The President presented the budget bill on 7 November 2017 and the act was not signed into law until 16 May 2018.

The Senate President, 2015-19, has now lost his Senate seat. The APC has a simple majority in the Senate which implies that it will be able to elect a Senate President. However, at this stage, with not all the Senate elections declared, it is unclear exactly how strong the APC position in the Senate, and the House of Representatives, will be. On balance, however, it looks as though the President may have an easier relationship with the legislature than during the period 2015-19.

Economy and unemployment

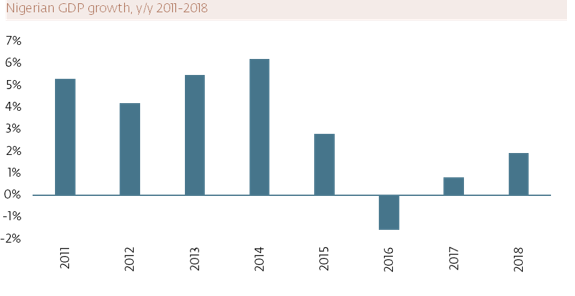

A feature of President Muhammadu Buhari’s first term as President was weak economic growth, 2015-18. GDP developed well below trend and fell into recession in 2016. One key cause was the oil price collapse in late 2014 and 2015 which put pressure on: government revenues; the Naira exchange rate; the trade account; and Nigeria’s ability to import critical industrial inputs.

Low growth has been associated with rising unemployment, which not only took off in 2015 and 2016, as the economy slowed and went into recession but continued to rise during the weak recovery that followed.

The administration’s policy emphasis during this period was on: security; the fight against corruption; tax compliance; and tight regulation, which included exchange controls. Agriculture (25% of GDP) was supported with subsidized fertilizer and soft loans, and never went into recession, and an Economic Recovery and Growth Plan was enacted. One can argue that, after Naira devaluations in 2016 and 2017, the worst is behind us.

Economic growth – the green shoots

Although 2018 GDP growth, at 1.93% y/y, was slow, there are a number of positive items in the data. Non-oil growth is accelerating and reached 2.70% y/y in Q4 2018, compared with the overall growth rate of 2.38% y/y. Of the six largest sectors in the economy, Agriculture, Trade, Manufacturing, and Telecoms have all recorded at least two consecutive quarters of growth.

External shocks characterised the years 2015-18: oil price shocks (2015), followed by a rise in US rates (2018). In forecasting US$58.00/bbl average oil prices for 2019 we demonstrate how the world has adjusted to new realities.

If external shocks in the coming period 2019-23 are not as great as those during 2015-19, then the nascent economic recovery might give this administration an opportunity to address pressing domestic issues. These include the insurgency in the North East, the herdsmen crisis in the Middle Belt, and disruption in the Niger Delta. Economic growth is a better platform for politics than a recession.

Interest rates

Following the Naira/US dollar devaluations in 2016 and 2017, average annual domestic inflation increased from 9.00% y/y in 2015 to 16.55% at the end of 2017. The job of the Central Bank of Nigeria (CBN) was to both stabilize the currency – and the exchange rate has been broadly stable since August 2017 – and to bring down inflation. Early in 2018, the CBN began to win the battle against inflation and so it brought down the risk-free rate, which it sets with its open market operations (OMO).

Later in the year, the Monetary Policy Committee (MPC) of the CBN began to express concern about the level of foreign investor participation in Nigeria’s fixed income markets and the danger posed to foreign exchange reserves if those investors left. Soon afterward (in August) the CBN began to raise the risk-free rate so that foreign investors would continue to invest in OMO bills and T-bills. This policy has succeeded, in our view, in keeping foreign exchange reserves high (currently US$42.4bn) and the currency stable.

On the other hand, a risk-free rate 587bps above inflation might seem excessive in the context of domestic growth. And a slightly lower spread over inflation might be judged possible when it comes to attracting Foreign Portfolio Investment (FPI). Therefore, if inflation trends down towards 10% y/y towards the middle of this year (the CBN’s target range is 6% – 9%), then we may see interest rate cuts. These could appear in Q4 2019, less likely in Q3.

By Coronation Research