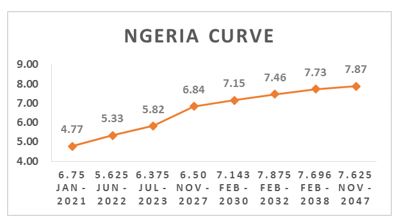

Bond Yields Trend Higher as Market players Cut losses on the 10-Yr

Nigeria’s 9mobile takeover nears as regulator finalizes review – Reuters

KEY INDICATORS

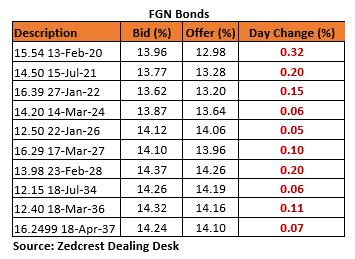

Bonds

The Bond market remained scantily traded in today’s session, with very few trades observed mostly on the 2020s and 2034s. Market players were however bearish on the 2028s following the significantly higher stop rate on the bond at the previous day’s auction. This consequently pushed yields higher by c.13bps avg., as spreads widened across other maturities.

We expect yields to remain slightly pressured, but with some intermittent client demand expected on the longer end of the curve.

Treasury Bills

Activities in the T-bills market remained slightly bearish, as the CBN intervened in the market via an OMO auction sale to mop up excess inflows (c.N400bn) from maturing OMO bills. A total of c.N350bn of the 91- and 210-day bills offered were purchased by market players, with stop rates maintained at 11.05% and 12.15% respectively. Secondary Market Yields consequently inched higher by c.3bps, following slight sell mostly on the 30-Aug and 31-Jan maturities.

We expect yields to remain relatively stable, as system liquidity remains relatively buoyant at c.N280bn, following the net inflows from today’s OMO maturity.

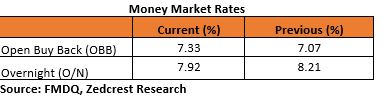

Money Market

The OBB and OVN rates remained relatively stable at 7.33% and 7.92% respectively, as system liquidity is estimated to increase slightly by c.N50bn as at close of business today.

Rates are expected to close the week at these levels, as there are no significant outflows expected, with exception however of c.N67bn Bond auction debits, which should be largely offset by c.N50bn bond coupon payments on the Jan-2022 maturity.

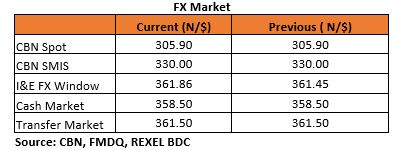

FX Market

The Naira remained stable at N305.90/$ in the Inter-bank market, whilst depreciating slightly by 0.11% to N361.86/$ at the I&E window. The Parallel market rates also stayed flat, closing at N358.50/$ and N361.50/$ at the Cash and transfer market segments respectively.

The CBN’s external reserves has however maintained its recent decline, down to $47.26bn as at 25th of July, as the CBN has sustained its interventions across the various market segments, in the wake of weaker inflows from Foreign portfolio investors.

Eurobonds

The Nigerian Sovereigns remained firmly bullish, with yields compressing by c.20bps across the curve. We witnessed the most interest on the 2047s, which gained about 2pct d/d.

Investors remained slightly bullish on the Nigerian Corporates, with most interest seen on the DIAMBK 19s, ACCESS 21s and UBANL 22s.