Nairametrics| Last week, the International Monetary Fund (IMF) released its Article IV report on Nigeria, which essentially is the international agency’s review of key macroeconomic developments in Nigeria over 2016 and its recommendations for policy makers on how to manage the economy in the near and medium term. The report, which can be assessed here, is supposed to provide an objective view point of the Nigerian economy from the standpoint of a neutral party, and is usually highly illuminating. I will try to provide my take on some segments of the IMF’s analysis in the next few posts but will start with the exchange rate.

The four approaches to valuing the naira

As ever, nothing gets the blood of the average Nigerian pumping these days than conversations around the naira. In the article IV report, the IMF claims (on page 15) that at the current exchange rate of N315/$ at the interbank, the naira is 18% overvalued by its estimates. Indeed, in a separate telephone call with Reuters, the IMF mission chief to Nigeria claimed that the currency is anywhere between 10-20% overvalued at the current rate. IMF writing is not for the layman, and indeed a lot of the report delves into the esoteric language familiar to followers of the econometric wing of the dismal science.

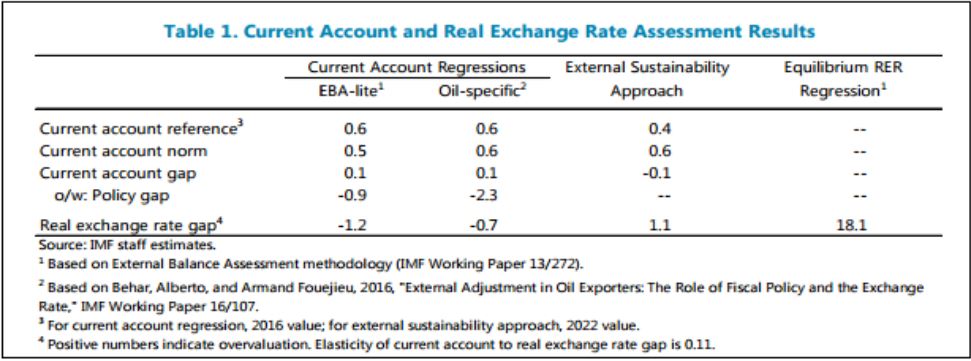

Now in any economic type writing, the best place to find the author’s Achilles heels is the appendix, where beneath all the economic/statistical jargon several hidden/naïve assumptions lie. In page 57, which deals with external sector assessment, the IMF makes use of three procedures:

- the current account or External Balance Assessment (EBA) approach

- the External Sustainability (ES) approach

- and the Equilibrium Real Exchange Rate Regression (ERER) approach.

The EBA approach can be adjusted to focus on oil type economies so in a sense we end up with four approaches. The results of all methods are displayed below.

From the extract, a positive number implies currency over-valuation and so it is clear that the 18% number the IMF is bandying about in the media is from the ERER approach. So what of the other three approaches? From the extract, it is clear the two EBA approaches are mildly negative implying the naira is modestly undervalued, while the ES approach suggests a 1.1% overvaluation. If we assume a margin for error, the broad inference from three approaches (EBA-lite, oil specific EBA and the ES) suggest the naira is well roughly square with where it should be trading – in simple terms, fairly valued. Three out of four is 75% – a pass in any book – but strangely, the IMF neglected to mention the results of these approaches in its main report or in media briefings, but elected to go with the result from the ERER approach.

Immediately, this set alarm bells ringing. Though the IMF would issue what, in hindsight, looks like a standard disclaimer (Caution is warranted in interpreting these results); the report would further state that …“The fit of both the current account and the ERER approaches is poor for Nigeria”.

Now if you did any statistics in school, the word ‘fit’ jumps out – a poor fit in a regression analysis is indicative that the model under consideration has a low R-squared, implying that variation in the explanatory (independent) variables do not account for the bulk of movement in the dependent variables. In simple terms, any conclusion arrived at using a model with a poor fit cannot hold water in any debate.

Thus, why would the IMF parade 18% as the extent of naira over-valuation when its own “econometricians” have discarded the model used in arriving at 18% number? A little further, the IMF puts the following paragraph which I requote verbatim:

Notwithstanding these issues, a possible explanation for the results is that the CA and ES approaches reflect transactions undertaken at exchange rates across all market segments—as well as transactions not undertaken due to lack of FX—while the ERER model considers only the interbank rate. The ERER approach thus points to an overvaluation of the interbank exchange rate, while the other approaches do not suggest current account misalignment, though their relevance in the current context is unclear given the presence of FX restrictions and multiplicity of exchange rates.

Put simply, the language implies that while the model does not look so good, the IMF eggheads think (more like guess wildly) that due to certain issues with the data the ERER more closely explains what is going on with the naira.

So let me summarize what the IMF has done, they have run four complex econometric procedures, and admitted that two of these methods, the CA and ERER are poor models for the Nigerian data. However they have elected to adopt the result of one approach (ERER) as the basis for their conclusion that the naira is over-valued by 18%.

If that does not have your whiskers up in the air, now let’s look at IMF’s naira assessment for its article IV report for 2015 which can be assessed here.

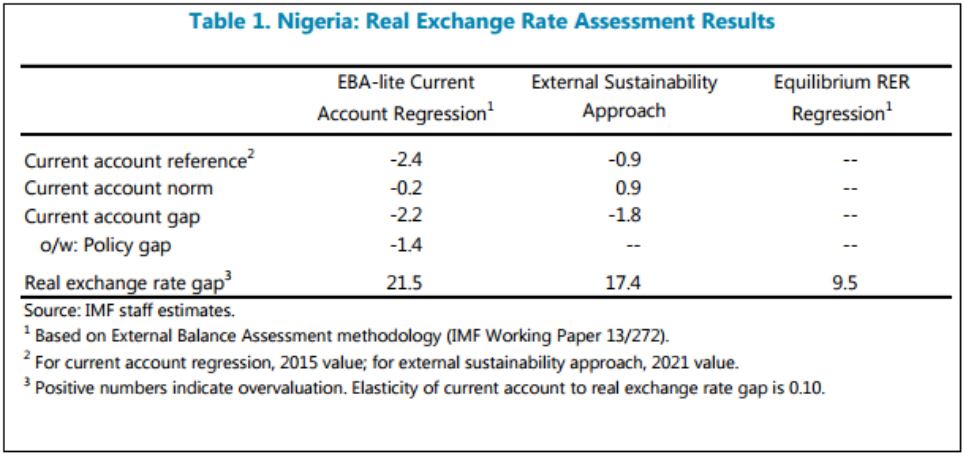

This time around, the IMF used only three approaches all of which, in the words of the Bretton Woods agency, suggest the naira was overvalued in 2015.

“These quantitative approaches point to an external position that is weaker than that implied by medium-term fundamentals and desirable policy settings, with a current account gap of 1.5 percent to 2 percent of GDP and a real exchange rate gap of about 15-20 percent”.

Hold on, but the ERER model says only 10%, so why is the IMF tugging at the 15-20% range. The answer lies in the IMF’s own assessment of the ERER model, which I have extracted below.

From above, the IMF says in clear terms that the conclusion reached from the ERER methodology of 9.5% overvaluation should not be taken seriously for 2015, but that of the other two techniques are fine. So in the space of one year, the result of the ERER model has gone from being treated with caution to being used as the basis for the IMF’s conclusion that the naira is overvalued.

Puzzled, I decided to go back one more year to 2014, whose report can be viewed here, and if you guessed right, the IMF again cautioned against drawing any inference from the ERER approach as in the extract below.

A summary of IMF’s valuation of the naira 2014-2016

So let me summarize our review of IMF reports in the last three years on naira valuation. While the ERER approach has a poor fit in 2016 and despite bad-mouthing the methodology in the last two years, the IMF proceeds to utilize the model’s conclusion that the naira is overvalued by 18% in the main report. Importantly, the IMF elects to be silent in the main report and in press briefings, that its other models which were the basis of its naira views in prior years implied that the naira was fairly valued.

Clearly, the method inconsistency, willingness to adopt techniques which point to higher naira overvaluation and silence over methods which suggest otherwise, hint a marked bias in the IMF assessment of the naira exchange rate. It is not out of hand to posit that the IMF does not appear to be playing a neutral role, as it is clearly favouring methods which are providing it with a suitable argument. Why? I will leave the answer open to imagination and debate but I think it is sufficient to say doubts should now exist over the IMF’s assertion.

In my personal opinion, while I do not think that the IMF has an ulterior motive, I believe that when examining Nigerian data and its economists come across findings unfamiliar to their western backgrounds, instead of treating these developments as uniquely Nigerian and trying to seek out local context for clues, the IMF guys naively try to force-fit their own country experience to interpretation. Naturally, when the next cycle of economic reviews comes around, the excuse used the last time become a poor explanation for current developments which results in inconsistency. If this scenario persists Nigerians will certainly be justified to raise suspicions about IMF’s intent and I do not think its views can be taken as infallible at least within the context of the naira’s fair value.

So what is the NGN’s fair value?

Over long periods of time, currencies tend towards the direction (note I did not say magnitude or estimate) implied by its balance of payment position (i.e. current account and capital flows). Till date no one has observed the famous purchasing power parity in actuality, it is a purely long run concept which is meaningless in the realm of the now.

However, over shorter time periods, currency forecasting is more an art than a science. As I argued last week, after the over 46% drop in the value of the naira since 2014 relative to the 55-60% drop in oil prices, the naira was much closer to long run fair trend average than ever before. Indeed, as earlier stated, the IMF’s own results in its 2017 article IV report appear to affirm this fairly valued naira thesis.

So, why is demand and supply not clearing out at these levels? The current dislocation is where the CBN should take knocks for its ill-advised decision to jettison interbank NGN trading in February 2015, when it imposed a hard peg of N199/$. Though it would later adopt a ‘floating exchange rate regime’ subsequent re-imposition of another peg at N305/$ in September 2016 would reveal its true intentions. With no price discovery currently, we are stuck in a limbo and my biggest worry is when we do eventually allow more naira trading, it will painfully require further devaluation. The sooner we get over this stage, the better, as naira trading now seems to be taking place in another rather crude platform which has a way of creating expectations on naira trajectory rightly or wrongly.

Currencies can overshoot their values in the short run as proved by a German economist, Rudiger Dornbusch, in his ‘Over-shooting’ theory. The CBN, and Nigeria’s fiscal policy makers, should be ready to allow a return to naira trading as we did prior to 2015 with modest overshoot now that our external position appears to be improving. While naira weakness and its resulting inflation hurts aggregate demand via real incomes, the allocation ills associated with the current frozen and increasingly multi-tiered FX regime imply greater costs to economic activity.

NB: As I argued last week, a return to naira trading does not imply implementation of a pure float, rather, pending the institutional adjustments required for a full floatation, a managed floating regime, as we had pre-crisis, serves as a more realistic, tolerable second best argument.