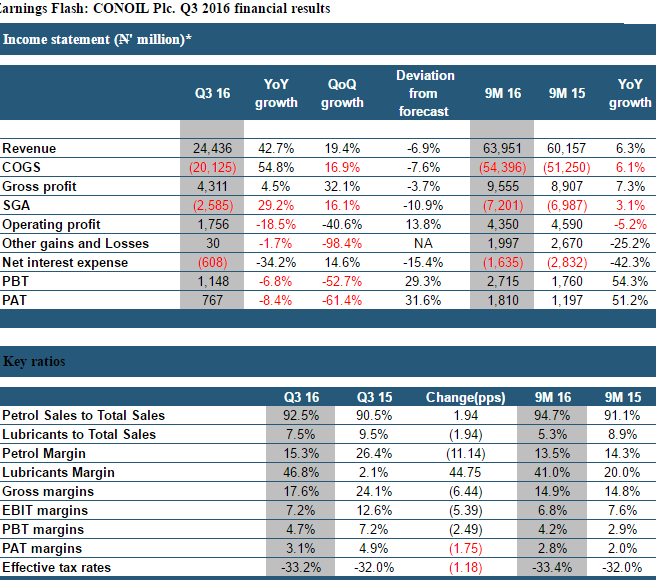

Yesterday, Conoil Plc. released its 9M 2016 results, wherein revenue rose 6.3% YoY to N63.9 billion while a slower increase in COGS (6.1% YoY) drove a slightly faster rise in Gross Profit (+7.1% YoY to N9.5 billion). Supported by a significant decline in net finance cost (42.3% YoY) as well as tamer rise in opex (3.1% YoY), PBT and PAT expanded 54.3% and 51.2% YoY to N2.7 billion and N1.8 billion respectively. EPS of N2.7 was largely in line with our estimate of N2.9 save for our miss on lubricants segment.

Focusing on Q3 16, revenue for the period rose 42.7% YoY (19.4% QoQ) to N24.4 billionlargely on the back of a 45.7% YoY (14.0% QoQ) rise in petrol sales. However, COGS which expanded 54.8% YoY (16.9% QoQ) tapered gross margin by 6pps on a year ago basis to 17.6% (15.9% in Q2 16).

Further down, opex expansion of 29.2% YoY (16.1% QoQ) to N2.6 billion, despite a slight increase in other operating income’ to N30 million (-98% QoQ and -1.7% YoY), drove PBT and PAT 6.8% YoY (-52.7% QoQ) and -8.4% YoY (-61.4% QoQ) to N1.1 billion and N767 million respectively.

On a segment basis, lubricants business recorded its highest gross margins since inception (46.8%) as cost-to-sales ratio dipped to 53.2% in Q3 16 (59.0% in 9M 16) –a 20pps contraction from an average of 72.9% over the preceding 8 quarters. For us, the decline in sales is surprising as we had expected higher cost pressure due to impact of NGN depreciation in non-petrol segments. We hope to get more clarification from management on this front.

For petrol, despite the 24.1% decline in volumes from the preceding quarter (-13.2% YoY) to 155.8 million litres, the +50-58% QoQ increase in fuel prices was more than enough to push petrol sales 14.0% higher QoQ to N22.6 billion –a 45.7% increase on a year ago basis. The drop-in petrol volumes, which is lower than the drop reported by Forte Oil (60.0% QoQ) and Total (43.2% QoQ) was largely due to the company’s relatively tamer price increase to a band of N140 – N143 per litter compared to N145 by other players.

Overall, underlying performance shows significant improvement though rising opex and imminent cost pressures will be central in our outlook for Q4 16.

Conoil currently trades at P.E and 2016 P.E of 13.8x and 8.3x vs. peer averages of 19.8x and 14.7x respectively. Our FVE of N41.70 implies a premium of 16% to current price of N30 –we maintain our BUY rating on the stock.