If you were a pig (bulls make money: bears make money: pigs get slaughtered) and you bought and held First Bank stock over the past five years your holdings would have gone nowhere fast.

As a matter of fact you would have lost money.

First Bank is Nigeria’s biggest Bank by assets with the potential to be the lender generating the highest profit due to the numerous revenue levers it has in view of its dominant position in Africa’s largest economy.

A comparison between FBNH and First Rand Limited (FSR : SJ), which is in a similar position as the largest banking group in Africa’s second largest economy South Africa, shows this is not the case.

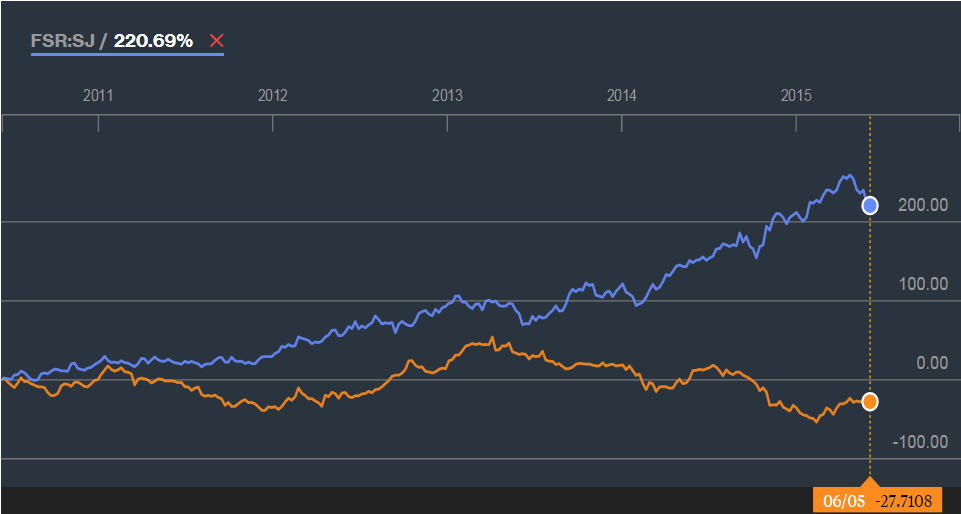

Fig 1: FBNH vs. FSR: SJ five year stock chart

Source: Bloomberg

Big economy…Small banks

The chart above shows First Rand which is listed on the JSE is up 220.69 percent in 5 years, while FBNH is down 27.7 percent in the same period.

Nigerian Banks have a $503 billion economy to exploit but their valuations are puny compared to South African lenders, showing low linkages with the real economy.

Nigeria’s financial services sector contributed just 3 percent to rebased GDP, compared with 15 percent for South Africa.

South Africa’s FirstRand Ltd has a market cap of $23.8 billion (R294.4 billion) that is 15 times larger than FBN holdings market capitalization of $1.6 billion (N321.26 billion).

Banks operating in South Africa’s $350 billion economy, had total assets of $352.3 billion (R3.7 trillion) in 2013, compared with Nigerian bank assets of $139.5 billion (N22.64 trillion).

The South African lenders assets would equal 100 percent of GDP, compared to 28.2 percent for Nigerian lenders.

First Bank as poster child for underperformance

Looking through the banks Full year 2014 financials show that First Bank is not a particularly well run bank.

The lenders cost to income ratio (CIR) rose to 66 percent in 2014 as total costs jumped to N235.8 billion on revenues of N354 billion. This compares to 43.4 percent CIR f0r industry leader GTB. The bank needs to bring its CIR down near to the 50 percent mark to improve profitability.

The return on Equity (RoE) was 16.8 percent in 2014, which is less than the banks cost of equity. Despite its wide branch network, the bank was only able to grow deposits by 4 percent, meanwhile its employees jumped to 10, 464 workers from 8,837 in 2012.

We think that technology should be replacing some of this growth in employee numbers to improve productivity and profitability.

Looking ahead there is no short term catalyst to own First Bank shares in our opinion and in fact the lender faces a couple of negatives.

FBNH is highly exposed to dollar – naira Foreign exchange (FX) volatility as FX makes up 56 percent of loans and 31 percent of deposits on its balance sheet.

The deteriorating macro – environment mean some loans may go sour for lenders, especially in the oil and gas space.

FBNH is currently exposed to the tune of $400mn to a single obligor named Atlantic energy.

Former CBN governor Lamido Sanusi raised significant concerns about the transparency around contracts awarded to Atlantic and other related companies, such as Septa Energy and Seven Energy, including concerns about non-remittance of oil sale proceeds to the federal account.

According to Renaissance Capital:

“Considering the media coverage these transactions have had over the past year, we think it highly likely that the new government could have them reviewed. Atlantic Energy and its loan from FBNH and Skye appear to us to be the most likely target here…given the risk that some of these transactions could lead to NPLs at the banks. This is important because we do not think there is the regulatory/political will to see the Asset Management Corporation of Nigeria (AMCON) executing another round of NPL purchases in the banking system so soon.”

Ratings agency Standard and Poor’s meanwhile believes that FBNH will need to raise capital soon to meet Central Bank (CBN) Capital Adequacy Ratios (CAR).

“First Bank is one that in the next 12 to 18 months will have to do some sort of capital raising or come up with a balance sheet strategy that may include slowing growth or removing assets,” S & P said in April.

In the meantime investors in First Bank shares are stuck in a down trend since early 2013 (see Fig 2).

Fig 2 : FBNH five year chart

The only positive in the chart above is the potential head and shoulders breakout that could happen at the N15 per share mark.

PAT MELIK