PZ Cussons Nigeria Plc. (6 months ended November 2014)

- PZ Cussons Nigeria Plc (PZ) reported 2.5% YoY contraction in revenues to N31.7 billion for 6 months ended November 2014 while PBT and PAT declined 37% and 38% YoY to N1.9 billion and N1.4 billion respectively.

Tight trading in HPC drives sales contraction

- On the heels of flat top-line growth in FQ1, sales declined 4.6% YoY in FQ2 15 to N16.6billion– 7% behind our forecasts. Amid cautious trading environment in Northern Nigeria due to insecurity issues, PZ management notes tight competition in soap and detergent segment–with hints of price discounting–weighed on its key Home and Personal Care (HPC) division (~70% of sales). The slack pattern in HPC continues to over-ride double digit growth in its electrical business where PZ reports higher patronage of its low-end Haier Thermocool generators.

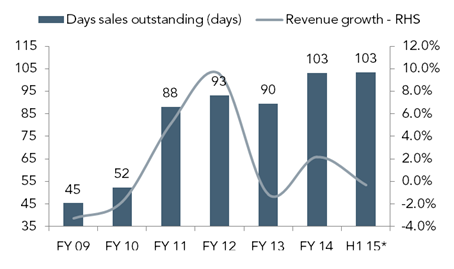

Figure 1: Trends in revenue growth and days sales outstanding

Price discounting and Naira devaluation offset benign input cost picture

- Whilst mean crude oil prices plunged 18% over FQ2 15, pass-through to PZ’s petrochemical input costs, which likely lagged the reporting period, was offset by impact of 8% USDNGN devaluation at the end of November. Assisted by price discounting across its HPC segment, the foregoing resulted in FQ2 15 COGS declining slower than revenues (-2.6% YoY to N12.1 billion) resulting in an 8.6% YoY cutback in gross profits to N4.5 billion (FQ2 15E: N4.9 billion). Consequently, gross margins fell 130bps YoY to 27.3%

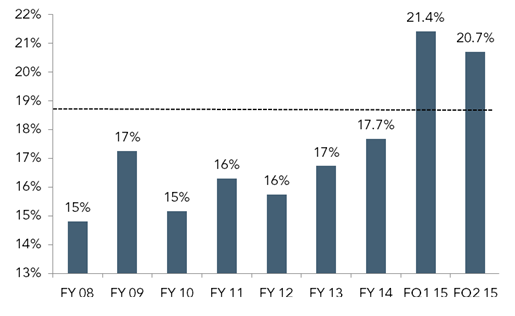

Figure 2: Imported raw materials-COGS ratio

Source: Company Financials, ARM Research

Brand renovation expenditure underpins higher OPEX

- In line with trends across our consumer coverage universe, FQ2 15 operating expenses rose 7.3% YoY (FQ1 15: +9% YoY) to N3.4 billion (FQ2 15E: N3.3billion). Although no breakdowns were provided, PZ’s guidance to brand renovation over FY 15 suggests higher marketing expenses drove uptick in OPEX. Consequently, EBIT declined 35% YoY to N1.2 billion with related margin shrinking 3.3pps YoY to 7%.

Figure 3: OPEX-to-sales ratio

Source: Company Financials, ARM Research

Net finance expense exacerbates earnings pressure

- In contrast to the trailing 6-quarterly trend of net finance income, PZ reported net finance expense of N90.6 million over the quarter in part reflecting a 57.9% QoQ contraction in cash balances to N1.4 billion and short term borrowings over the period. Largely reflecting the gross margin contraction and higher OPEX, FQ2 15 PBT and PAT declined 41% and 43% to N1.1 billion and N799 million with corresponding margins 4pps and 3.2pps lower YoY at 6.4% and 4.8% respectively.

Tepid growth outlook and higher risks in macro-environment underpin downgrade to our recommendation

- Current reading extends the trend of sub-par top-line growth reported by PZ on account of the challenging trade environment its key HPC segment faces. Whilst earnings outlook should be buoyed by the benign trend in crude oil prices which we estimate bolsters GM by 2-3pps, sustained USDNGN volatility and prospect of higher S&D costs as PZ seeks to match intensifying competition dampens pass-through of input cost gains. Lowering our mean sales growth projections over forecast horizon from ~10% previously to more closely match PZ’s trailing 5-year CAGR (3.7%) and raising our discount rate assumptions to capture rising sovereign yields following the oil price declines drives moderation in our FVE to N19.45. PZ trades at a current PE of 28.1x vs. 24.76x for Bloomberg Middle East and Africa peers with its last trading price at a 28% premium to our FVE which implies a change in our recommendation from NEUTRAL to SELL