Nascon recently changed its name from National Salt Company to Nascon Industries Plc. The name change was for a strategic reason and it has nothing to do with branding. The company is starting to find out that life as a salt maker (even if they are the market leader) is not as rosy as it used to be. [upme_private]

Key Highlights

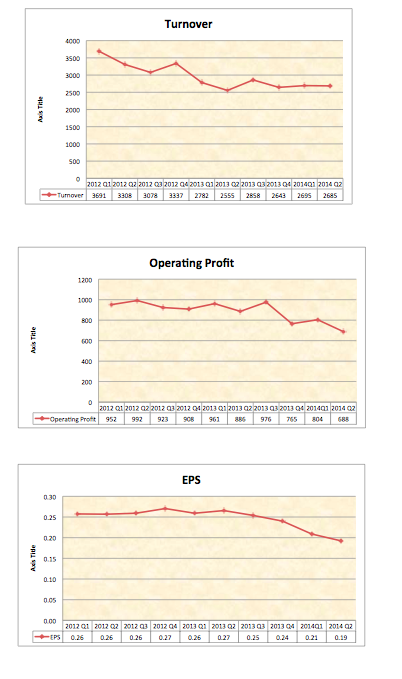

- Revenue has been on a decline over the last 10 quarters

- Margins have also dropped off significantly

- Unrest in the North has negatively impacted on their business

- Volumes are currently down

- The company is diversifying into Vegitable Oil and Tomato Paste business and has changed its name to reflect the move

- Share price is currently at fair value and is expected to drop in further by the end of the year

The decline Nascon over the last two years has been reporting a steady decline in revenue growth. The company has moved from posting N3.7billion a quarter in revenue to about N2.7billion a quarter. This slide in revenue has been consistent over the last 10 quarters and it seems it is far from abating. Operating profits, which is another key metric that I follow has also been on a decline over the last 10 quarters as the chart below depicts. It’s therefore no surprise that the company continues to post a declining earnings per share over the last 10 quarters.

Solutions The company has identified these problems and decided to do the needful by diversifying into vegetable oil as well as making tomato paste. It is hoped that these will provide alternative revenue source for the company and reduce its dependence on Salt. The prospects here are mouth-watering and with the right political influence, Dangote can turn this into a money spinner. But let’s not be carried away, there are lots of power players in these markets already and I am not sure there is even room for growth. However, it is a plus that the company is at least not sitting down doing nothing. They already spent almost N4billion on their diversification plans and all of this is purely debt free. It is important to remember that even after posting a 23% decline in profits for the 2014 H1, Nascon still posted a return on average equity of 17% (34% annualised). That is still a great piece of business to own.

Buy, Sell or Hold? The decision to buy, sell or hold this stock is not an easy one. Currently the share price is trading under N10 and just about its fair value considering its latest result and outlook. On current basis my gut instincts is a sell and on short terms basis it’s a hold. It’s sell is because nothing currently indicates an upside for this stock considering that growth has stalled and may continue to be tepid at most and dividend will not be paid again till next year. There is very little to create a momentum around the share price at the moment so I see no reason holding on if you are looking for capital appreciation.

Hold on a short term basis boils down to a possibility that a big announcement may occur in the next six months. The company maybe looking at raising fresh equity or may be looking at acquiring smaller companies as it seeks to diversify it earnings. The possibility of a smooth election next year as well as a positive turnaround in the security situation in the North may also play a huge role in turning its fortunes around. Basically, nothing in its business is expected to positively affect the share price in the next 6 months except off course something big (other than results) occurs. This makes holding this stock a recipe for buying it on the medium to long term. Its potential down the line is visible and its fundamentals still remain sound. I have included Nascon as a buy in out Stock Picks based on a short to medium term outlook for the stock. We like the company and still feel it is a sound business. The problem it is facing are huge but not endemic. They are also working hard to reverse this trend. All their efforts however, will be noticed in months if not years. Preferred price is under N9.50 and we believe this stock will still drop to under N9 by the end of the year. We will keep buying at a price lower than our intrinsic value as we also keep a close eye on the stock as events unfold.[/upme_private]