Gala, Swan, Dulux, Mr Biggs etc are all house hold brands in Nigeria and are owned by one company – UACN Plc. UACN Plc is one of the oldest companies in Nigeria and is one of the largest conglomerates quoted on the floor of the Nigeria Stock Exchange. The company is also a member of the NSE 30 most capitalized companies and is one you regard as a blue chip company. However, it currently trades for about N68 and has ranged between N35-N70 in the past one year. At that price, a decision to own the stock in our portfolio will mostly have to depend on our valuation of the stock. We will begin with a brief SWOT analysis of the company’s fundamentals followed by our assumptions and model used in valuing the shares of the company. [upme_private]

Strengths

- UACN is a cash cow and owns major brands with high cash generating capabilities. It has about N8b in the bank and working capital of about N11b

- UACN has generated about N292b in revenues in the last 5 years combined at an annualized average of N58billion per annum growing at 5% CAGR

- It posted N69b in revenue in 2012 and is likely to post about N80b for full year 2013. It already did N60b in the first 9 months of 2013.

- UACN is also profitable and has posted consistent profits in the last 5 years. It averages an annualized profit of N3.3billion annually

- UACN also has a high dividend payout ratio and has paid about in the last 5 years and average of 90% of profits declared as dividends.

- Its share price has risen almost 200% in the last 5 years and 98% in the last one year alone.

- Its businesses is very well diversified with an effective value chain. They have succeeded in creating a vertically integrated line of business which helps fight competition

Weaknesses

- Despite its high dividend payout ratio, dividend yield was about 1.1% when it paid dividend in 2013. By far lower than market average of 5%

- Margins are rather low for the company. Operating profit margin is just 11% following their latest 9 months release.

- Return on Equity averages 9% in the last 5 years way below what you expect from a blue chip company

- Heavy reliance on its food and beverage sector for turnover. 65% of revenue is currently from its F/B division.

- The only outlet for investor returns based on the current price is via capital appreciation. That provides no guaranties especially if the market believe the share price is over valued or under valued.

Opportunities

- UACN Plc remains a formidable company and is a fantastic inclusion in any portfolio

- Its business are well known and they sell products and services Nigerians use daily. This ensures revenue will continue to rise

- Its property division contributed N3.3b to profits in 2013 alone. This trend may persist as they expand their real estate business into more profitable assets such as offices and retail.

- Renewed interest in the country’s economy is helping drive economic growth and attracting FDI’s. This presents a huge opportunity for the company to provide word class office space and services further widening revenue base.

- The company is also obviously not relying on growing organically as it continued to acquire businesses, spin off some and also realign interest in its subsidiaries. The company has the cash flow to do all this.

Threats

- Intense competition recently ongoing in the F/B industry may threaten revenues and reduce profit in the coming years. Most of their new competitors also have deep pockets and are nimble enough to pivot as market dynamics change.

- The peculiarities of their businesses suggest high operating expenses may continue to be a challenge for the company.

- In fact, its 2013 9 months result showed they had to rely on income from sale of property to beat last years pre-tax profits.

- High interest rates is also a source of concern

- There is little evidence of an upside for investors as the share price appears to reflect the expected 2013 full year EPS already

Valuation Assumptions

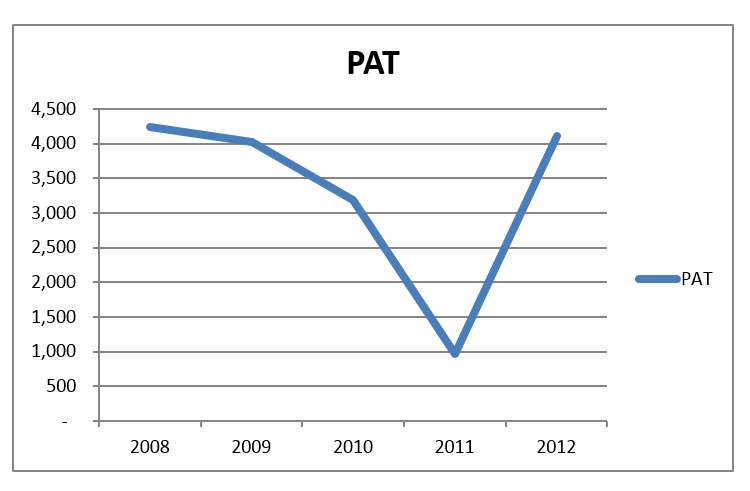

- UACN Group EPS has been haphazard and inconsistent to say the least. See above However we based our earnings projection on a 3 year CAGR of 9%

- We expect revenue to continue to grow at a CAGR of 5% to ensure profitability growth is sustained as projected. Revenue growth may also rise higher or lower depending on how its various acquisitions and spin offs pay off.

- UACN ROE averages 9% however we used a DCF of 15% in discounting EPS. At Ugometrics we like our investments returning at least 15% (Investor ROE). Always remember your ROE is different from the ROE of the company due to the premium or discount you pay on the Net Asset Per Share.

- P.E ratio is about 32x and PEG ratio is estimated at 3.65x suggesting an overvalued stock on the surface.

- We however priced in what we call “sentiment value” in our valuation to capture the sentimental trend associated with the stock. We achieve this by multiplying the derived intrinsic value by the 5 year CAGR of the share price appreciation

Result

UACN by our valuation is worth about N38 in intrinsic value at N47 if you factor in market sentiments. Even at our suggested price earnings yield is way below our 15% marker. However, this is compensated by the fact that the company payouts on average 94% of dividends. Whether that trend will persist in the future we really can’t tell for now.

Opinion: Overvalued

Other assumptions & methodology used

Valuation is done based on DCF of future adjusted earnings per share. This is added to the terminal value and the current Book Value per share.

- Buyer of the share is only a minor shareholder with no influence that can be liken to any form of control

- Expected yield is based on the most recent ROAE of the company

- Inflation rate is projected at 9% average for the next 5 years

- Shares bought will be held for a minimum of 5years

- A margin of error of 8% is apportioned to make up for its uneven PAT

Request for the spreadsheet used if you want to tweak some of our assumptions.[/upme_private]

{kind=link}

Is this valuation for UACN still valid? What do you think of the N37 current price range?

Thanks

Overvalued in my opinion