Bond Yields Expected to Tick Higher following Weak Auction Results

Ignore pressure to sign-on to AfCFTA agreement, MAN urges FG

KEY INDICATORS

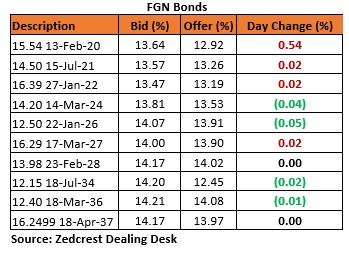

Bonds

The Bond market traded on a relatively quiet note, as market players waited on the sidelines in anticipation of results of today’s Bond auction, which has been much anticipated to provide a direction for movement in yields in the near term. Yields ticked slightly higher by c.5bps on average, due to weaker bids on the shorter end of the curve.

Results from the bond auction showed a continued weakness in demand for the shorter tenured bonds, with most bids skewed towards the 10-yr bond. The DMO was consequently only able to raise about N66.90bn from a total offer size of N90bn, with stop rates rising by c.29bps from their previous levels. The highest uptick was witnessed on the 2028s (+49bps), in tune with the gradual normalization of the bond yield curve.

We expect the market to be slightly bearish, especially on the mid to long end of the curve, as market players react to the higher stop rates at the auction.

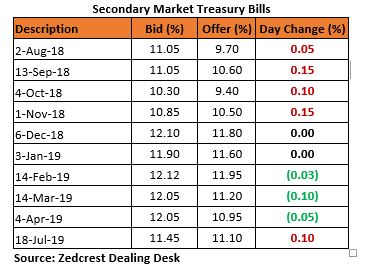

Treasury Bills

Activities in the T-bills space were slightly bearish, with some sell-off witnessed mostly on the Aug – Jan Maturities. This came on the back of expectations for a renewed supply of OMO T-bills at an auction by the CBN tomorrow. Yields consequently inched higher by c.5bps on average.

We expect yields to be fairly stable tomorrow, as the CBN is expected to conduct another auction to mop up inflows from c.N293bn Maturing OMO bills.

Money Market

The OBB and OVN rates remained relatively stable at 7.07% and 8.21% respectively, as system liquidity remained relatively buoyant at c.N230bn, despite the outflows from the OMO T-bill sales in the previous session.

Rates are expected to be relatively stable tomorrow, on the back of OMO maturity inflows, which should be offset by an OMO auction by the CBN.

FX Market

The Naira remained stable at N305.90/$ in the Inter-bank market, while it maintained gains across other market segments. The CBN’s external reserves has however maintained its recent decline, down to $47.30bn as at 24th of July, as the CBN has sustained its interventions across the various market segments, in the wake of weaker inflows from Foreign portfolio investors.

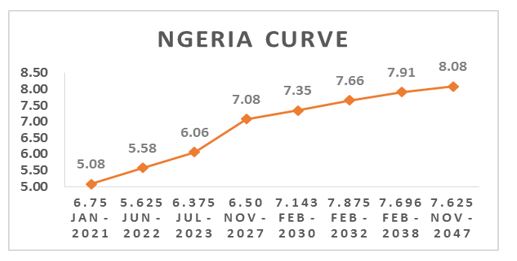

Eurobonds

We witnessed renewed interest on the Nigerian Sovereigns, with yields compressing by c.4bps across the curve. We witnessed the most demand on the 2030s, which compressed by c.7bps (+0.50pt).

Investors were also bullish on the Nigerian Corporates, with demand witnessed mostly on the GRTBNL 18s, FBNNL 21s, UBANL 22s and FIDBAN 22s.

{kind=link}