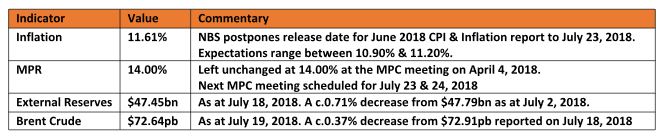

KEY INDICATORS

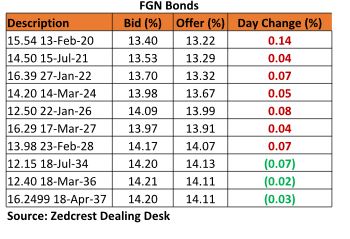

Bonds

The bond market opened weaker following the release Q3 2018 FGN Bond Calendar by the Debt Management Office. Yields expanded by c.7bps as sell offs were witnessed on the short to mid-end of the curve. Pockets of demand were however witnessed on the long end, where yields compressed by c.4bps on the average.

We expect the market to close the week on a bearish note as market participants evaluate the impact of a 50% increase in the amount on offer at the next bond auction.

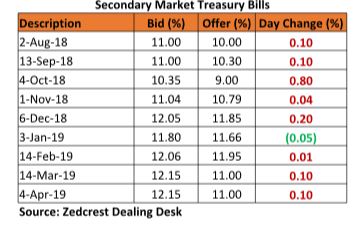

Treasury Bills

T-bills reversed previous gains from previous trading sessions, as discount rates expanded by c.16bps on the average across the benchmark securities. Profit taking was witnessed today as market players positioned for higher yields at the OMO auction floated by the CBN.

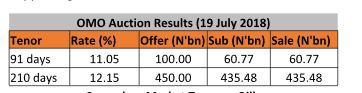

The CBN sold a total of N496.25bn at the OMO auction across two maturities, effectively clearing out the entire demand. The 91- & 210-day bills on offer were closed out at stop rates of 11.05% & 12.15% respectively.

We expect market participants to continue sell-offs on the short to mid-end of the curve to provide funding for the SMIS Retail FX sale expected by the CBN tomorrow. The funding pressures thus supporting our bearish outlook for T-bills.

Money Market

Despite the sale at the OMO auction by the CBN, system liquidity remained buoyant to close at c.N397.16bn. Rates in the interbank money markets closed trading at 6.83% and 7.42% for the Open Buy-Back (OBB) rates and overnight (O/N) respectively.

Expected funding pressure from the SMIS Retail FX sale by the CBN tomorrow should cause a further squeeze in liquidity, and we expect an uptick in interbank funding rates to close the week.

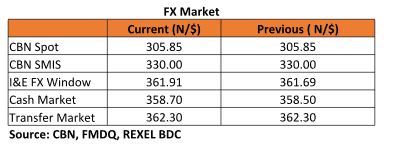

FX Market

The Naira remained relatively stable, as the Interbank rate closed at N305.85/$ for a second trading session. The NAFEX rate appreciated depreciated by 22k, closing at N361.91/$ (from N361.69/$ previously).

The Naira was relatively flat at the parallel market. The USD cash rate lost N0.20k to close at N358.70k while the transfer rate remained stable at N362.30/$ respectively. The CBN is expected to offer dollars for sale at its Retail SMIS auction tomorrow to take out retail demand, average sale amount so far for the retail SMIS is c. $320bn.

Eurobonds:

The bearish trend for the NGERIA Sovereigns continued, with yields expanding further by c.02bps on average across most traded tickers. Demand pressures were however witnessed on the NGERIA 38s, as yields compressed by c.24bps.

The NGERIA Corps also witnessed continued buy interest across most of the traded tickers. We witnessed the most demand on the longer-dated tickers; Access 21s as well as FIDBANK 22s.

{kind=link}