A review of Nigeria’s trading partners over the past decade shows that in recent times, specific to Imports, the proportion of goods being imported has shifted from the western countries to the east of the world (think Asia).

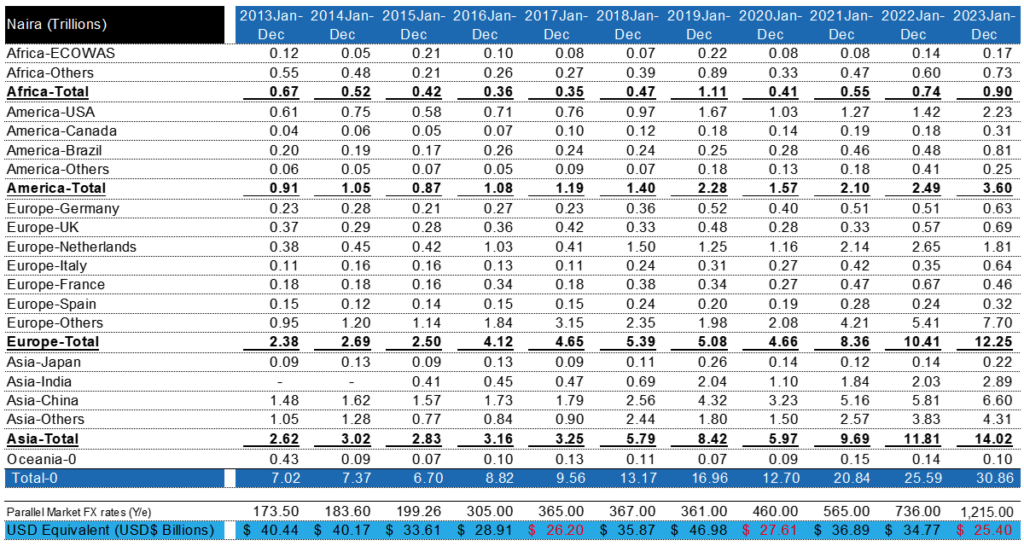

The first table shows that on a nominal basis, the value of imports grew from N7 trillion in 2013 to over N30 trillion in 2023.

However, in international terms, the value of Nigeria’s imports typically ranges between USD $30billion to USD $40billion. Albeit in difficult years (2017-recession, 2020-covid and 2023-dollar shortage) the value of imports drops below that range.

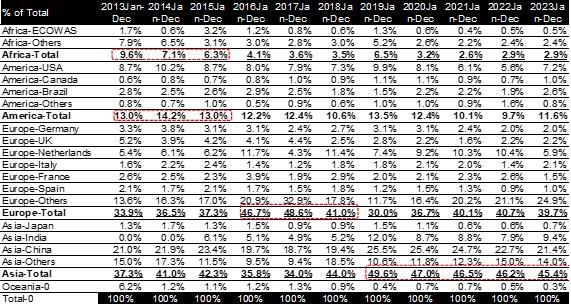

Taking a deeper look at Nigeria’s import value by country, readers will observe that in the trailing decade between 2013 to 2023, the location of Nigeria’s imports has traversed across regions.

- Specifically, between 2013 to 2015, Nigeria’s import was sourced from America and Africa, this switched to Europe between 2016 to 2018 at >40% of Import.

- However, since 2019, Asia has become the largest source of imports for Nigeria at over 45% of Imports.

- Remarkably, India which was NOT a source of import in 2013 now accounts for almost 10% of Nigeria’s import in 2023.

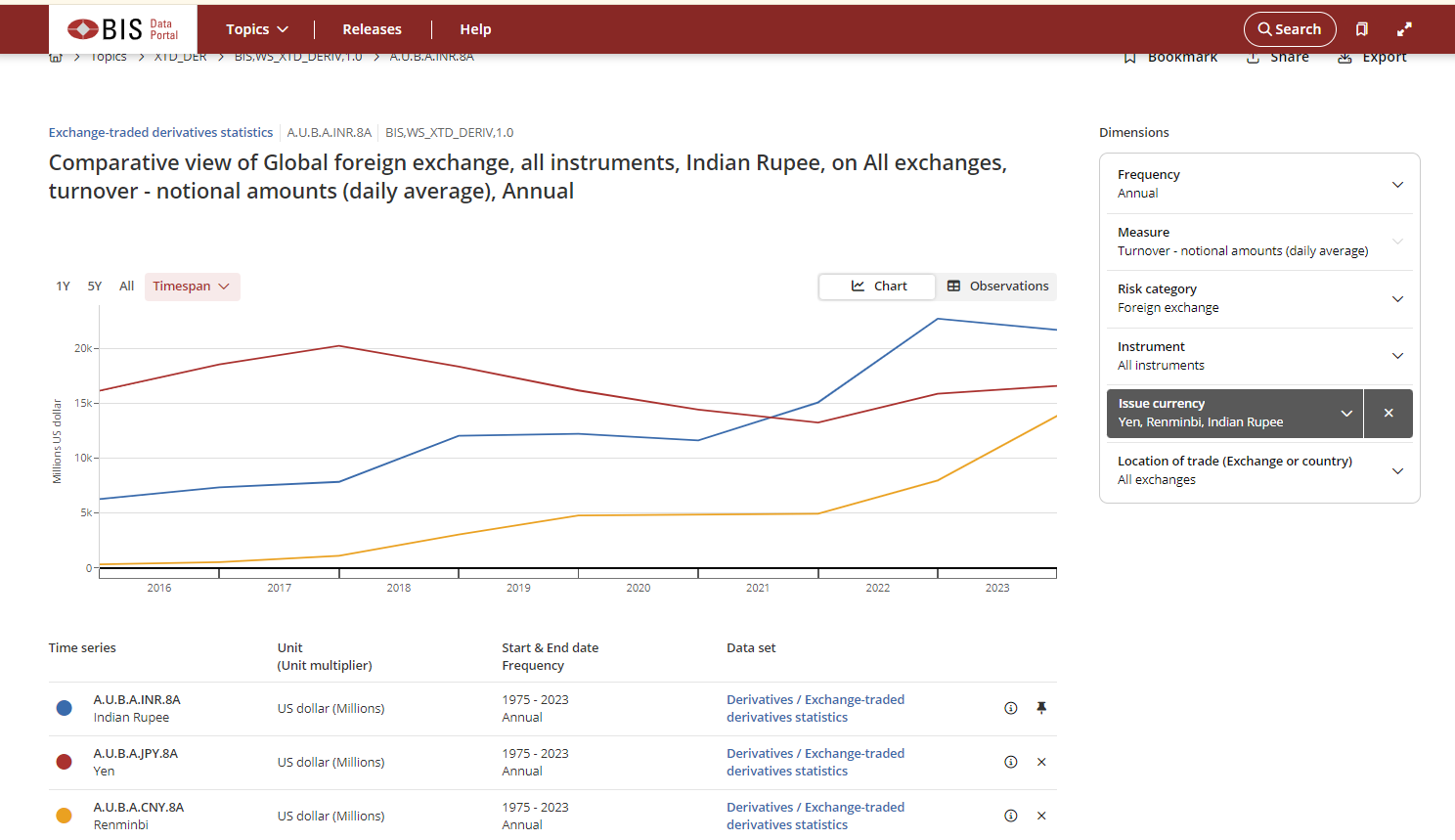

Notably, the currencies used by our key Asian trade partner nations are JPY, CNY, and INR.

As outlined in the chart from BIS below, the volume of activity for these currencies on the global stage continues to rise such that these Asian currencies that can be sourced from many Foreign Exchange markets.

Why does it matter that Nigeria’s imports have shifted East?

Despite this shift of imports to the east, Nigeria’s daily financial news landscape about foreign exchange is perpetually inundated with the Naira-dollar quagmire, as well as, Nigeria’s Central bank’s incessant attempts to halt a dollar target which is simply bolting out of the APEX Bank’s reach.

On a daily basis, all Nigerian news outlets continually replay ad-infinitum how much naira is required to buy a single dollar such that this has become a fascination of how many variations of Naira-USD rates can be published daily (AM vs PM)

As if the fascination by news outlets is not sufficient, our Central bank compounds this fascination with unrelenting circulars about the various actions being taken to manage foreign exchange, [RDAS, Dollar sales to BDCs, FX circulars and now an Amnesty for those who have stashed dollars).

- The Central Bank even goes as far as publishing ONLY the exchange rate for USD prominently on its website to solidify the ongoing perception that the sole focus in Foreign Exchange Management is on USD liquidity and pricing.

- All other currencies which Nigerians have to trade with barely get a mention and Nigerians have to unilaterally resolve challenges required to settle cross-border transactions with emerging Asian trading partners.

So this begs the question

- Why is there still so much infatuation with the Dollar, especially given that data shows that Nigeria’s trade has shifted east (i.e. to Asian countries)? Thus, from a trade perspective, the dollar does NOT need to be the predominant currency of concern.

- What is being done by the Central Bank to ensure Nigerians have the ability to settle transactions in Asian Currencies thus supporting a more seamless shift to import goods from Asian countries which are known to be cheaper than Western counterparts?

Why does the infatuation with the Dollar persist?

Here are three reasons why some economists would argue that the infatuation with the Dollar persists,

1. Firstly, from a Central Bank perspective, the fundamentals of Reserve Management require countries to hold sufficient reserves to be able to meet their liabilities. Countries typically hold reserves in Foreign Currencies that are deemed safe, secure, liquid and fungible.

- Nairalytics and Nairametrics readers can learn more about Foreign Reserves here and here

- Note that these reserves are reported to the IMF which tracks and updates the COFER report. Data shows that for Central banks worldwide, the dollar remains the predominant currency to keep their reserves

2. Secondly, countries occasionally need to borrow on the international stage. From a risk perspective, Countries and currencies that have large reserves to cover multiples of their liabilities are perceived as better (i.e. less risky) than countries with smaller reserves.

3. Thirdly, for International Trade, most trading partners prefer using currencies that are widely accepted, supremely fungible and can serve as a global store of value (i.e. USD, EUR, GBP, Yen).

- Remember in international trade there is a huge latency between when goods are ordered then shipped then delivered, such that large shipping transactions can easily take 3 months to 6 months. Thus, a stable currency such as USD is required to give suppliers the confidence to issue invoices and settle cash on a 3 to 6-month lag, whilst mitigating the risk of incurring translation losses

However, the above reasons are only relevant for aspects of the Central Bank’s remit around FX Stability and Reserve Management. The CBN is also responsible for price stability and containing inflation.

Unfortunately, a singular focus on attracting USD will not be sufficient to achieve the CBN’s additional responsibilities relating to price stability and addressing inflation. This is because there is a steep cost to attract Dollar inflows to Frontier and Emerging Markets. Whereby Central Banks for Frontier Markets and Emerging Markets are limited to using tools such as

- raising interest rates higher and higher, implementing strict capital control measures and imposing administrative oversight actions such as requiring businesses to complete Forms amongst others.

It should go without saying that high interest rates, administrative oversight, capital control measures and continuous transaction costs create a challenging business environment and hinder economic growth

Furthermore, having trade settlement scenarios that are tripartite with currency hops creates transaction frictions. Simple economics tells us any transaction friction carries an associated cost.

- For context, imagine a Nigerian trader in Aba supplying shoes to his clients in Ethiopia with an agreement for trade settlement currency in USD.

- In this scenario, the client in Ethiopia will convert the Ethiopian Birr into USD, and pay for the goods. The Nigerian trader based in Aba will receive the USD and then convert it back into Naira to settle his input costs.

- This scenario creates challenges for scaling the relationship. Growing the business requires sourcing more USD first.

Similarly, Nigerian businesses importing goods from Asia countries, currently need to enter separate arrangements to obtain the USD and then pay for the goods. The Asian supplier will receive the USD to convert back to local currency to settle business input costs.

So what should Nigeria’s Central Bank be considering in light of emerging trends on Imports/Trade Partners?

It is little wonder that from an intra-African trade and Nigeria-Asia trade perspective, a colossal obstacle to scale remains timely transaction settlement.

As Nigeria seeks more trade with the Asia continent, two actions that should be paramount for Nigeria’s Central Bank remain

- Larger Bilateral FX Swap arrangements similar to the Yuan Swap, as well as,

- Stronger commitment to deploying technology-driven cross-border payment solutions.

- Nigerians should be able to open their banking app and pay suppliers in India/Japan/China (even if amounts are capped to say 50 million monthly)

We saw a lot of fanfare regarding the launch of PAPSS, as well as, the e-Naira initiative. However, neither has yielded the transformational results touted by the initiatives.

The pros and cons of bilateral currency swaps can be a topic of debate in future articles. However, everyone knows that a long-term and more cost-effective alternative is for the Central Bank of Nigeria to facilitate the deployment of cross-border settlement solutions.

Adopting technology to facilitate seamless cross-border currency settlement will solve a critical aspect of international trade settlements (some startups are already solving this problem see Nala, Tranglo, Nium or even meCash.

Now that the CBN is addressing FX volatility with some stable trend in FX rates being observed, AND Nigeria’s foreign exchange reserves growing, it is now time to revisit simplifying cross-border with robust security.

Enabling Nigerians to pay for imports directly in Asian currencies will arguably reduce the nation’s import unit costs, lower inflation, and improve our cost of living and quality of living.

Incremental benefits such as enabling Nigerians to tap into the India Healthcare market to source high-quality and affordable drugs directly or purchase new products rather than used equipment will also be a win-win for consumers.

So do we still really need the dollar?

{kind=link}