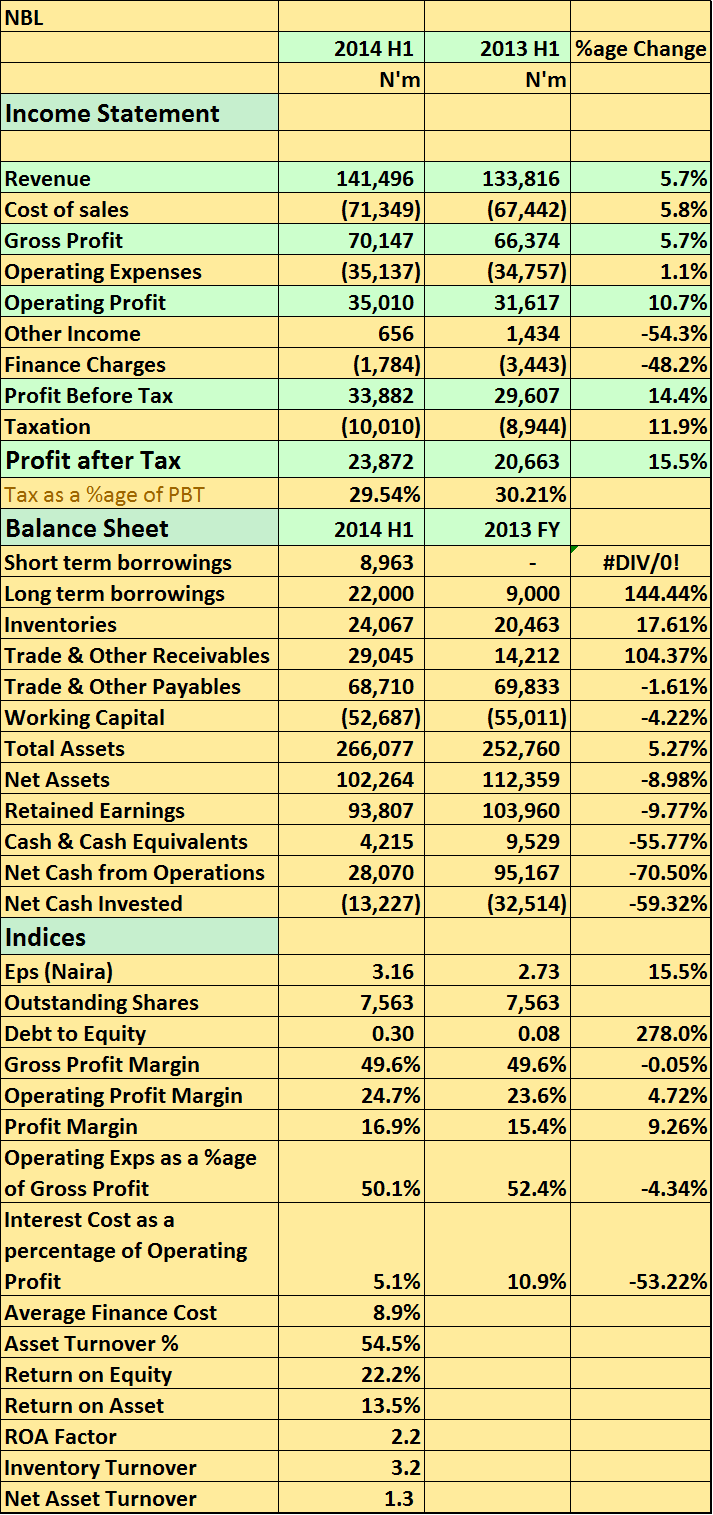

Nigeria Breweries released its 2014 Half year results showing a Year on Year (YoY)15.5% rise in earnings per share to N3.16 (2013 H1: N2.73). Revenue was also up 5.7% to N141.4billion compared to N133.8b reported in the same period 2013. On paper, this looks like a good result considering the following pointers;

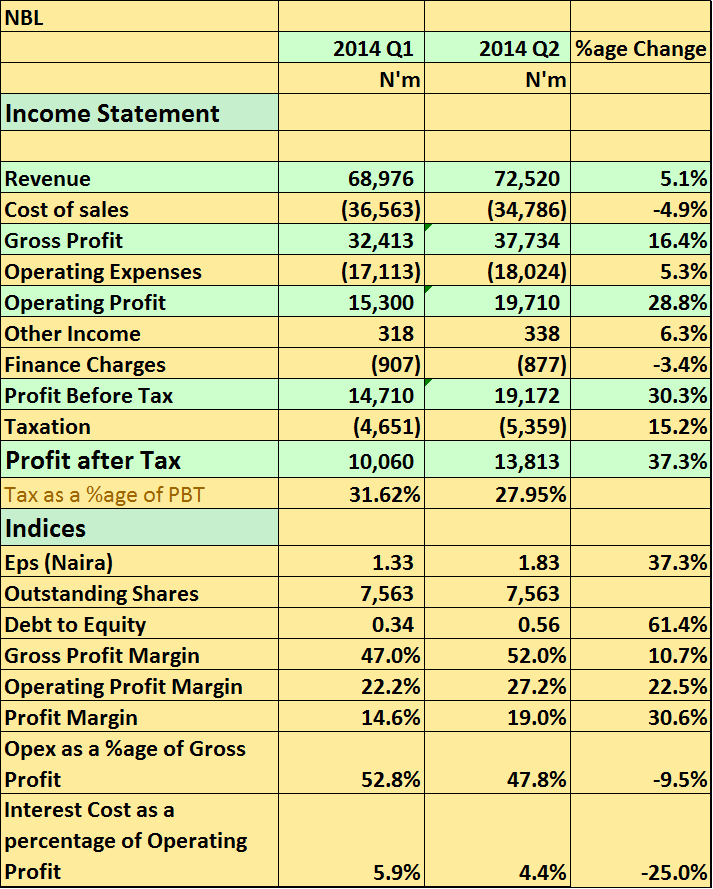

- Despite the fact that revenue rose 5.7% YoY, it also rose 5% this quarter compared to first quarter of 2014.

- The N72.5 billion in revenue posted for Q2 2014 (March – Jun) is the highest for any Q2 results since I started tracking in 2012. This is particularly notable when you consider the fact that the brewery sector has been facing intense competition of late.

- Operating profit (without taking other income into consideration) also rose 28% Quarter on Quarter (QoQ) and 10.7% YoY. It shows operating expenses has remained stable this year. N18billion in operating expenses this quarter still keeps their cost with 2013 averages.

- Trade receivables increased by N1billion during the quarter, though still a concern. Higher receivables over periods is a worry because it creates a default risk which we do not want.I however, believe the brewery giant is watching this closely too.

- Interest cost also dropped 3.4% QoQ and 53% YoY all good pointers towards higher profitability. Though, a huge chunk of interest may well have been capitalized.

Why are these important? These factors to a larger extent determine how much profitability growth Nigerian Breweries may report later in the year. Currently the share price has averaged N178 this year with a trailing price earnings ratio of 30x. The P.E ratio suggest a high expectation on its profitability growth which for now seems inconceivable despite this result. The current P.E ratio is 3x its trailing earning growth (PEG ratio) which is a sign of an over priced stock. Will I buy now? Not at this price and growth levels. Will I sell? if I had the stock, no I won’t.

As usual, your thoughts are fully welcomed.

{kind=link}