With the NMRC coming to market to kick-start its refinancing scheme, most participating mortgage banks could be potential winners, but quite few of them will be even bigger winners than most.

In addition to the refinancing of original mortgages from the NMRC bond proceeds, there is a possibility that a securitization of mortgages to create Asset Backed Securities is in the offing. The reason stems from the interest of US-based Cantor Fitzgerald, a global financial services firm.

In March, the firm signed an MOU with the NMRC, and announced an investment of N200 billion in the mortgage industry, which was at the time, seen as a bellwether for heightened activity within the Nigerian mortgage banking space.

For scale, the size of its investment is about 70% of the entire market cap of Nigeria’s listed mortgage banks.

This interest from Cantor Fitzgerald is significant because it is a major player in the world of global finance. It is one of only 22 primary dealers authorized to trade US government securities with the Federal Reserve Bank of New York. It was the world’s 1st electronic platform for US government securities, and it became renowned for its computer-based bond brokerage (as far back as before the 1980s) and the quality of its Institutional distribution business model.

Cantor Fitzgerald specializes in the creation of new-issue securities, and offers services in derivatives, convertibles and structured products. It also provides services in mortgage-backed and asset-backed securities. It prides itself in pioneering new markets and fueling the growth of original ideas.

As an early stage investor in the housing scheme, an exit through a securitization route is not unfathomable.

Asides its monetary investment, the industry stands to gain from Cantor Fitzgerald’s expertise in the generation of Asset (mortgage) Backed Securities (ABS) and fixed income trading.

On the other hand, investor interest in the Series 1 bond appears robust, given the fact that it is backed with the full faith of the Federal government. Further more, according to the NMRC, the loans that are currently in line for refinancing are of the topmost quality, with little chance of default.

With the possibility of creating ABSs out of mortgages originated by the Primary Mortgage Banks (PMBs), PMBs can be further re-financed for the mortgages they originate (through the pass-through of 3rd party investors’ purchase of securitized products), and as such, maintain the cash flow needed to originate more mortgages.

This means that mortgage banks can potentially be refinanced via two routes. Through the NMRC bond proceeds route, and through Asset Backed Securities route.

This is essentially the Holy Grail of the mortgage business.

A surge in 3rd party financing could be looming, and that emphasis in the near future will be on how much of those mortgage assets 3rd party investors can lay their hands on. Demand for mortgage-backed securities could soar.

There will be demand on mortgage originators (the PMBs) to feed in mortgages into the mortgage pool of the NMRC for refinancing via the bond sale, and there will be demand to feed mortgages through to the ABS securitization vehicle for on-sale to 3rd party investors.

The implication of this is that the mortgage bank with the ability to create the most mortgages will obviously benefit the most.

So, who are the mortgage firms that create the most mortgages in the country?

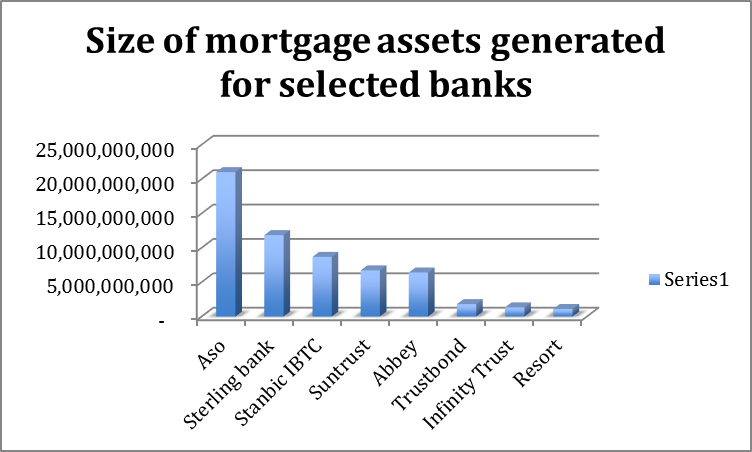

NMRC’s current mortgage portfolio paints a fairly clear picture. A few big financial institutions, in terms of size of total assets and mortgage lending activity, dominate the mortgage industry with its circa 20 players. Aso savings, Sterling bank, and Stanbic IBTC lead the pack (according to analysis of publicly available data).

To paint a better picture, in 2013 (for the sake of comparability), Aso’s mortgage assets stood at N21 billion. The second largest was Sterling bank, whose mortgage assets stood at N12 billion, 44 percent lower than Aso. Stanbic IBTC, who generated mortgage assets valued at N9 billion, was the third. Suntrust had N6.7 billion, and Abbey was next with mortgage assets worth N6 billion.

Comparing like for likes (mortgage bank versus mortgage bank), Aso’s total assets stood at N87 billion in 2013. The second mortgage bank, (according to publicly available data) Suntrust, had total assets of N24 billion. Abbey had its total assets at N14 billion.

Aso has not released its FY 2014, probably on account of its acquisition of Union Homes. Suntrust had not released too, as at the time of writing.

Based on these metrics, it should be fairly easy to pick out the winner(s) in the mortgage game (because we now know the biggest originators), even if the NMRC’s ambitious goal is half-fulfilled.

Wining Strategies

NMRC’s plan is ambitious. Over the course of 5 years, it hopes to have about 400,000 mortgages in its portfolio. To appreciate the grandness of this vision, it helps to know that there are only about 20,000 mortgages in the market today.

If this goal is going to be remotely achievable, then the banks that can tie into it will emerge as winners because 3rd party investor interest is already looking robust. (The NMRC bond is almost as safe as FGN bonds, being backed by the full faith of the Federal government).

The ability, and capacity to originate the most NMRC-compliant mortgages will be the winning strategy for mortgage banks going forward.

And going by the precedence set out by the first tranche in the portfolio, between 2 to 4 companies stand out.

Industry Leaders and opportunities

Aso savings, along with Stanbic IBTC accounted for more than 60 percent of eligible loans in NMRC’s Series 1 mortgage loan portfolio. Aso accounts for 27 percent of eligible loans in the country, while Stanbic IBTC accounts for 39%. For an unclear reason, Sterling is omitted from the Series 1 portfolio.

Aso prides itself in being able to have provided housing for over 15,000 people amidst the challenges in the industry. So its ability to provide even more with fresh funds should be a given.

But lower consumer spending remains the biggest challenge yet. The downside to the upside is the potential macro risk of slowing aggregate income growth, which might feed into an increased risk of loan default by homebuyers.

At an average rate of 18%, the repayment burden on homebuyers could prove a bit too much. At such a rate, a fear of loan default is not unfounded.

Cleaning up the mess

The present state of non-performing loans is still very significant, and is a testimony to the above fact. It is not unusual to see mortgage banks with non-performing loans to the tune of between 10% and 40% of mortgage loans made. (The subject of non-performing loans is topic for later).

But this is exactly what the NMRC has been working to clean up in the sector. It has introduced house-cleaning measures such as: ensuring that all mortgages originated by its participating banks are compliant with its new Uniform Underwriting Standards (UUS) – an upgrade from previous underwriting standards.

It also ensures that mortgage borrowers are made to accept that any property dispute is resolved through a different arbitration process that sidesteps the traditional courts. This allows disputes to be addressed in record time, and foreclosures to be done much quicker so that investors’ principal can be quickly recovered. Also, with a carrot and stick approach, it is getting state governors to “play ball”, and issue the requisite land titling. Additionally, there’s insurance against losses resulting from land titlings ‘gone bad’.

This means that mortgages in the NMRC mortgage pool are considered safer for 3rd party investors, by miles.

According to the NMRC, the loans that are currently in line for refinance are of the topmost quality, with little chance of default.

Stumbling block to housing revolution

Another potential hurdle in achieving the goal of a housing revolution is the supply of housing.

To achieve the housing goal, 100,000 units will need to be built each year, in the least. If this will be a herculean task remains to be seen. This also means that investors should watch out for mortgage banks that have very close ties and financing structures with homebuilders.

Nigerians need decent and affordable (low-priced) homes. The demand for this is huge. Innovative financing and home ownership products targeted at the middle and lower income bracket, is proving to be frontier for the mortgage industry.

According to the United Nations, around 58 million people will move to cities in sub-Saharan Africa this decade and Nigeria is at the heart of Africa’s urbanization.

{kind=link}