Julius Berger Plc was added to my portfolio September and November 2013 based on a valuation metric I used at the time. Since then the share price has hit a year high N76.45 declared dividend of N2.7 and given a 1 for 10 bonus issue. But my desire to own more shares of the company hasn’t yet diminished and this time I think the price is probably right. But before then, a quick buy or sell metricion should help determine;

1. P.E ratio – Julius Berger by my estimate has a one month P.E ratio of about 11x and going up. Forecasted P.E ratio based on my projected earnings per share of for 2015 of N7.86 should be about 9x. This is thus a forecasted earnings yield of 11% . Julius Berger also generates an EBITDA of about N19billion last year giving us an EBITDA multiple of about 5x which is in line with my current expectations.

P.E ratio is fair

2. Price to book ratio – Julius Berger currently has a PB ratio of 4.35X, one of the highest around. One metric I use when I see a company with a high PB ratio is to look at the composition of its shareholders funds. In most cases a high PB ratio is associated with a companies that have a smaller combination of share premium plus share capital relative to retained earnings. For JB retained earnings is N18.8billion compared to a Share capital plus premium of just over N1billion. So essentially, the company finances its operations organically and with debt and has resisted bringing in more expensive equity capital. You most likely will have to pay a premium for that sort of business. It’s no wonder ROAE is about 43% in 2013 and 66% in 2012.

PB Ratio is justified

3. Price to earnings growth ratio (PEG) – This ratio tells me if the earnings multiple placed on the shares is in line with its projected growth rate. By my estimate Julius Berger as averaged a CAGR of 25% in the last 5 years. This puts the PEG ratio at under 0.5. A PEG ratio of under 1 suggest an undervalued stock. But that growth rate is tricky even if that is what the data tells me. I adjusted to 5% and it gave me a PEG of 2.

A PEG of 2 at an adjusted EPS growth rate is ok for a blue chip

4. Dividend Yield – One of my favorite valuation metrics due to its ability to fairly value a stock based on how much it can actually pay you should you decide to hold for long. Last year (well this year if you consider when it was paid). I got a dividend yield of 4%. So if we assume dividend will remain N2.7the value will be about N67.5.

Current price is about right based on this. But the yield should be 5% in my opinion.

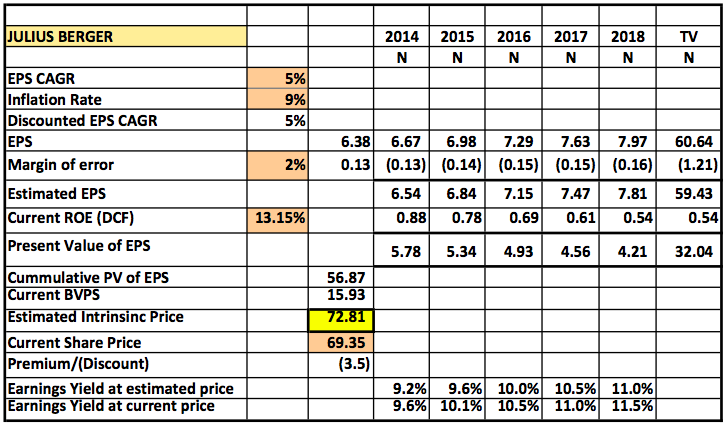

5. Discounted cash flow – Assuming a compounded annual growth rate (cagr) of 5% (which is probably conservative) on an earnings per share of N6.38 for the base year. And then discounting using a discount rate of 13% gives me a valuation of about N73. It’s important to note that JB currently has a 5 year CAGR of 21% and using that growth rate will give you a valuation of almost N200. However, I don’t see the company growing at that rate in the near term.

Suggest the stock is currently undervalued

6. Volume of Trade – Volume of trade is equally important when you decide to buy a stock. After all there has to be a willing seller and a buyer when you decide to do either. Bloomberg data suggest JB has an average 30day trading volume of 240,00 units suggesting it is not a very liquid stock. At the current price the value is just about N15.6m in value traded.

Probability of flipping the stock at a price you want is low. You might not easily get a willing buyer or seller.

7. Share price growth rate – Julius Berger has a year high of N76.45 achieved sometime in June 2014. Share price was N25 some 5 years back giving you a return of about 155% and CAGR of 21% annually if you had invested then. So if your question is whether the stock can increase in value over time, you have your answer.

Great for a value and long term investor

8. Debts – JB relies on loans to finance its huge operations as you can’t logically depend on an equity of N21billion to finance a turnover of N200billion. Currently, I believe the company generates enough EBITDA to service its total debts of about N26billion. Therefore there is no significant threat to shareholder returns.

No imminent threat here in my opinion

Other Issues

- Market – Will JB continue to be dominant in the construction sector? They have been there throughout the military and democratic era forging a good relationship with Federal and State Governments. But they also face competition from the likes of GCappa and other construction firms jostling for the hugely lucrative market. JB’s revenue has grown at a CAGR of 7%.

- Board & Management Team – They have a sound and experienced management team led by Woldgang Goetsch. Their Board is also very experienced and well connected

- Brand – JB brand is a popular one and their products are associated with quality.

- Opportunity – Infrastrucural deficit is high in Nigeria so there is noticeable potential to continue to increase revenue. They also have huge experience in Nigeria.

FInally,

JB is

Not for

- This may not be a stock for a short term investor looking for a quick capital appreciation

- Any investor looking for a high dividend yield

For

- Any investor looking for a sound business to invest in

- Any investor seeking assurance of a stable annual dividend payment

- Investor looking to optimise his portfolio with lower risk assets

Buy, Sell or Hold?

Buy – below N70,

{kind=link}

Great work on this UgoDre! Please can we see more of this on a regular basis? I have been eyeing JBerger and looking to add more to my portfolio and this helps greatly.

Thanks Dare. There are quite a number of them if you go to my “Valuation and Pricing” segment under “Investments” Category. Regards

How do I calculate my father’s shares of 300, in Julius Berger.