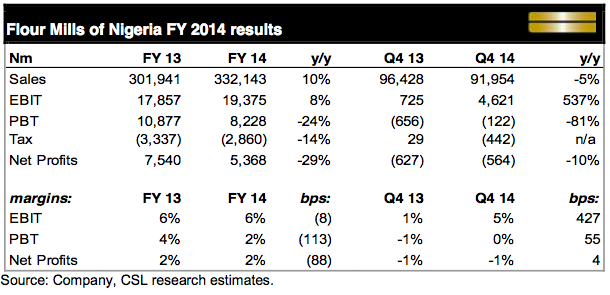

- Flour Mills of Nigeria (FMN) grew Sales by 10.0% year-on-year (y/y) to N332.1bn (US$2.0bn) in FY 2014 (March year-end, reported 1 August). On a quarterly basis, Sales declined by 4.6% y/y in Q4 2014 due to a significant decline in revenues from non-core divisions.

- The performance of the core Food Division is encouraging, in our view. Sales from FMN’s Food Division grew by 17.5% y/y, beating our expectation of 15.6% y/y growth. Sales from Packaging and Port Operations declined by 39.5% y/y and 82.4% y/y, respectively, as the company’s product mix changed significantly.

- EBIT increased by 8.5% y/y to N19.4bn (US$117.4m) but Net Profits declined by 28.8% y/y to N5.4bn (US$32.5m). Interest Expense increased by 41.2% y/y to N16.1bn (US$97.6m) on the back of the company’s significant increase in leverage.

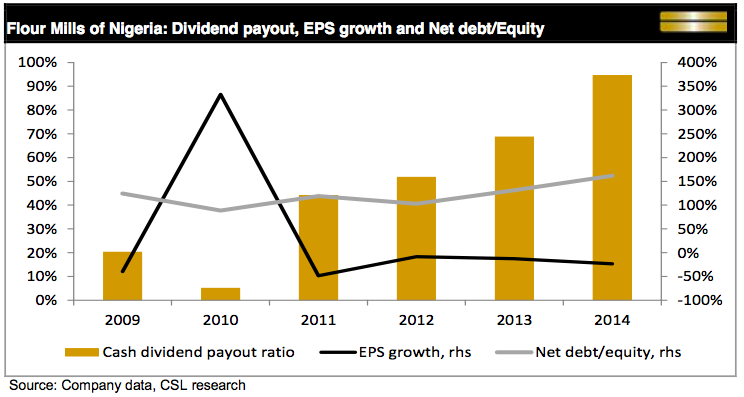

- Leverage rose during 2013 and 2014 and we believe the impact of additional debt on PBT is only becoming more significant as earnings have declined over the last three years and the cash pay-out ratio has increased. The pay- out ratio was 44% in 2011, 52% in 2012, 69% in 2013, and 95% in 2014 (based on the proposed dividend).

- FMN’s total borrowings (ex-the outstanding balance on the 2010 N37.5bn bond) increased by 33.4% y/y to N125.1bn (US$771.9m) as at FY 2014 with financial leverage (Total Assets/Total Equity) up to 3.6x (from 3.4x in 2013) and net debt/equity at 161.6%. We believe debt levels will remain elevated through 2015e-16e given the company’s recent push to pay out a higher proportion of its Net Profits as dividends.

- Our EPS computation for FY 2014 equates to N2.22 per share and the company has proposed a cash dividend of N2.10 per share and bonus issue of 1:10.

- The proposed dividend implies a pay-out ratio of 95% and gross yield of 3.1%.

- FMN currently trades on a one-year trailing PE and EV/EBITDA of 30.7x and 8.4x, respectively, which indicates that while FMN is trading almost on a par with the other flour miller under our coverage (notably Honeywell Flour Mills, Buy, current price N4.1/s, target price N5.2/s) on an EV/EBITDA basis, it is trading at a significant premium on a PE basis.

- We currently rate FMN a Buy with a price target of N106.3 (potential upside of +56.1%). We arrived at a target price for FMN through an equally weighted fair value from DCF and dividend discount valuation models.

Soure; CSL Research

{kind=link}